1. Introduction

The growing environmental challenges, social inequalities and governance concerns have intensified expectations on corporation to operate responsibly and transparently. Stakeholder such as shareholders, investors, government, financial analyst, customers, society and even employees now demand for not just financial performance but non- financial information (sustainability disclosure) for rational decisions. For companies such disclosures help strengthens legitimacy, build trust and align corporation strategies with the societal expectations and global sustainability goals. Corporate sustainability disclosure is the process by which a company publicly reports information about its environment, social and governance practices, impact performance alongside its financial results

| [17] | Sustainability directory (n.d) sustainability directory, sustainability-directory.com 2026. |

[17]

. In the recent times, the inclusion of sustainability report in management decision cannot be undermined. Accordingly, entities are required to provide disclosures on sustainability as part of its general purpose financial report to be published the same time

| [11] | IFRS-S1 and S1 international financial reporting standard –sustainability standard 1 and 2. |

[11]

. This report provides non- financial information that complement financial data enabling companies and stakeholders to make informed, forward looking and responsible decision as well as aid in reducing information gap between companies and stakeholders for better evaluation

| [4] | Amin M. R. 2025 sustainability reporting and its influence on investors decision making; critical perspective and empirical insight. International journal of science and research archive 6(1). |

[4]

. Many institutional factors are considered as responsible for influencing corporate sustainability disclosure including organisational culture, presence of sustainability committee, adoption of GRI, membership in advocacy group among others

| [13] | Kilic M., Uyar A. Kuzey C. Kanaman A. S. (2021): Drivers and consequences of sustainability committee existence? Evidence from the hospitality and tourism industry. International journal of hospitality management vol. 92. |

| [14] | Nwobu, O. A. (2017). Determinants of Corporate Sustainability Reporting in selected companies in Nigeria. Ota, Nigeria: An Unpublished Phd Thesis in Accounting, Covenant University. |

[13, 14]

. Studies on sustainability disclosure have cut across many industries both nationally and internationally including oil and gas, financial services, production and manufacturing, conglomerate, hospitality, telecommunication, with little attention in the health sector despite the role it plays in every economy particularly in Nigeria.

Despite the growing importance of sustainability disclosure or reporting, many firms and industries differ significantly in the quality and extent of their sustainability disclosures. Although sustainability reporting framework and governance mechanisms are increasingly promoted, prior studies have largely examined these factors in isolation. Empirical evidence on whether adoption of GRI framework, presence of sustainability committee as well as membership advocacy group jointly influence corporate sustainability reporting practice is still scarce including Nigeria.

This posed the question as to “does institutional factors combined have effect on corporate sustainability disclosure in healthcare sector of Nigeria”?

On this background, the study is aimed at assessing the effect of institutional factors on corporate sustainability disclosure of healthcare sector companies in Nigeria.

It further hypothesized that “institutional factors do not have significant effect on corporate sustainability disclosure of healthcare sector companies of Nigeria.

2. Literature Review

Conceptual issues

i. Corporate Sustainability Disclosure (CSD)

Corporate sustainability disclosure is synonymous with the terms citizen reporting, social reporting, corporate social responsibility, accountability report, and triple bottom line reporting

| [3] | Aman, Z., & Ismail, S. (2017). The Determinant of Corporate Sustainability Reporting: Malaysian evidence. Proceedings of the 4 international conference and management muamalah. Malaysia. |

[3]

.

A sustainability Report also refers to a report prepared by companies that disclose the economic, environmental, and social performance of business organizations. It also entails reporting the governance approach to sustainability performance

| [10] | GRI. (2013). Global Reporting Initiative. Amsterdam: G4 Sustainability Reporting Guidelines. |

[10]

.

Global Reporting Initiative

The Global Reporting Initiative (GRI) is a leading organization in the field of corporate reporting poised with a mission to promote the use of sustainability reporting by government, business, and not-for-profit organizations; thereby contributing to sustainable development. The latest reporting principles and standard disclosures of the GRI (G4) were issued in July 2013. Previous guidelines are the G3.1 (issued in 2011), G3 (issued in 2006), G2 (issued in 2002), and the 2000 guidelines. The G3.1 guidelines issued in 2011 classify the standard sustainability disclosures along three lines namely strategy and profile, management approach, and performance indicators. Based on Global Reporting Initiative (2011), organizations are supposed to declare the level to which they adhere to the guidelines when they report

| [14] | Nwobu, O. A. (2017). Determinants of Corporate Sustainability Reporting in selected companies in Nigeria. Ota, Nigeria: An Unpublished Phd Thesis in Accounting, Covenant University. |

[14]

.

ii. Presence of Sustainability Committee

Corporate Sustainability committees have an oversight role to play in the financial reporting process as well as in reporting on sustainability issues in terms of economic, environmental, social, and governance impacts on one hand and performance metrics on the other hand

| [14] | Nwobu, O. A. (2017). Determinants of Corporate Sustainability Reporting in selected companies in Nigeria. Ota, Nigeria: An Unpublished Phd Thesis in Accounting, Covenant University. |

| [18] | Tran, T. T. M. (2017). Institutional Environment, Corporate Governance and Corporate Social Responsibility Disclosure: A Comparative Study of Southeast Asian Countries. Huddersfield, United Kingdom: An Unpublished PhD theses submitted to the University of Huddersfield. |

[14, 18]

. The members of the board of directors of a business organization that oversees sustainability issues could be made to be members of sustainability Committee. A study conducted on the impact of corporate characteristics on social responsibility disclosure has revealed that the presence of a sustainability committee is related to the disclosure of human-related issues i.e. social reporting

| [7] | Cowen, S. S., Ferreri, L. B., & Parker, L. D. (1987). The impact of corporate characteristics on social responsibility disclosure: a typology and frequency-baed analysis. Accounting, Organizations and Society, 12(2). |

[7]

. While the presence of corporate sustainability committee is not cited explicitly in the literature as a moderating factor for more corporate disclosure. This could be due to the reason that the existence of such a committee is associated with a greater corporate propensity to make disclosures concerning social involvements.

Therefore, this study used PSC as one of the moderating variables to argue the paucity of research and it is measured by the presence of Sustainability committees. This variable was obtained from corporate annual reports of companies. It was measured using ‘1’ where a company has a committee on sustainability and ‘0’ for otherwise

| [14] | Nwobu, O. A. (2017). Determinants of Corporate Sustainability Reporting in selected companies in Nigeria. Ota, Nigeria: An Unpublished Phd Thesis in Accounting, Covenant University. |

| [18] | Tran, T. T. M. (2017). Institutional Environment, Corporate Governance and Corporate Social Responsibility Disclosure: A Comparative Study of Southeast Asian Countries. Huddersfield, United Kingdom: An Unpublished PhD theses submitted to the University of Huddersfield. |

[14, 18]

.

iii. Membership in Advocacy Group

Membership association to a group is allowing people or groups of people to subscribe and become a member advocating for a specific shared purpose. The membership in the advocacy group contains steps taken towards risk reduction and aimed to address steps taken to know companies involved in certain harmful kinds of business, ascertain the kind of risk involved, how to avoid negative impacts of such companies involved in the harmful operation as well as strategies to be adopted to address such issue

| [14] | Nwobu, O. A. (2017). Determinants of Corporate Sustainability Reporting in selected companies in Nigeria. Ota, Nigeria: An Unpublished Phd Thesis in Accounting, Covenant University. |

[14]

.

Conceptual Framework

The diagram below demonstrates the conceptual framework for the connection between institutional factors and corporate sustainability disclosure. It is used to predict the relationship empirically between institutional factors and CSD underpinned by resource based theory.

Figure 1. Relationship between Institutional Factors and Corporate Sustainability Disclosure.

The independent variable represents the factor that is observed in the study. In this context, it is institutional factors. While the dependent variables represent the outcome or response that is measured. In this case, it is CSD.

Source: Adapted from work of

| [5] | Baba Y. A., Joel M, Tahir F. A & Gulani M. G. (2023). Effect of firm characteristics on corporate sustainability disclosure in the health care sector of Nigeria. international journal of intellectual discourse, Bauchi State University, Gadau, Nigeria. |

[5]

.

Empirical review

A doctoral dissertation studied on determinants of Corporate Sustainability Reporting in selected companies in Nigeria from 2010 to 2014

| [14] | Nwobu, O. A. (2017). Determinants of Corporate Sustainability Reporting in selected companies in Nigeria. Ota, Nigeria: An Unpublished Phd Thesis in Accounting, Covenant University. |

[14]

. Company attributes, external institutional factors, and internal organizational process factors were found to be significant determinants of corporate sustainability reporting in the selected companies. The study also revealed that there was a statistically significant variation in sustainability reporting from the year 2010 to 2014 in the sample companies. The study further revealed that the companies were influenced by the disclosure guidelines of the Nigerian Stock Exchange regulator (SEC), the banking sector regulator introduced in 2011 and 2012 respectively. Results of the Fixed Effects model showed that the Securities and Exchange Commission (SEC) code of corporate governance, Central Bank of Nigeria Sustainability Banking Principles, accounting firm affiliation, and sustainability reporting. Also, stakeholder engagement had a significant positive relationship with sustainability reporting. From these findings, it can be concluded that stakeholder engagement is crucial for sustainability reporting.

An examination of the impact of corporate governance (CG) on economic, social, and environmental sustainability disclosures of the top 100 companies listed on the Pakistan Stock Exchange (PSE) for the period ranging from 2012 to 2015

| [15] | Mahmood Z. Kouser R., Ali W., Ahmad Z& Salma T. (2018), Does corporate governance affect sustainability disclosure? A mixed method study. Sustainability 10(1). |

[15]

. Data were collected from both primary and secondary sources. Overall results indicate that corporate governance elements enhance sustainability disclosures. Precisely, a large board size consisting of a female director and a CSR committee (CSRC) is better able to check and control management decisions regarding sustainability issues and result in better sustainability disclosure

In a related development, a doctoral dissertation carried out at the University of Hudders field on Institutional Environment, Corporate Governance, and Corporate Social Responsibility Disclosure (comparatively) in Thailand, Singapore, Malaysia, Indonesia, Philippines, and Vietnam

| [15] | Mahmood Z. Kouser R., Ali W., Ahmad Z& Salma T. (2018), Does corporate governance affect sustainability disclosure? A mixed method study. Sustainability 10(1). |

[15]

. The Analysis of Variance and Regression technique was utilized in the study. Firstly, empirical findings of CSRD levels across the countries showed that Thailand has the highest level of disclosure, followed by Indonesia, Malaysia, Singapore, Philippines, and finally Vietnam. There were significant differences between the extent of CSRD of the two countries with the highest disclosure (Thailand and Indonesia) and the lowest disclosure group (Philippines and Vietnam). The findings are interesting in the sense that the levels of CSRD do not reflect the stages of economic development, and therefore, the differences in CSRD levels could be attributable to the impact of other institutional factors. Secondly, in relation to internal determinants and based on the existing literature and the context of Southeast Asia, six corporate governance practices were identified to examine the impact of corporate governance on CSRD. The results of OLS regression supported the negative impact of block ownership and the positive impact of board size as well as the presence of the CSR committee on CSRD. Contrary to the theoretical and empirical expectations, board gender diversity was found to have a significantly negative relationship with CSRD, and board independence had no impact on CSRD. These differences could be explained by the context of the study where the presentation of women onboard is very low and independent directors might not be wholly independent. The effect of six institutional factors representing the three pillars, regulative (legal origin and mandatory disclosure), cultural-cognitive (uncertainty avoidance and masculinity cultural dimensions), and normative (the adoption of GRI standard and membership of CSR-related associations), were evaluated in this study. The empirical results indicate that mandatory disclosure, uncertainty avoidance dimension, and the adoption of GRI standards have a positive impact on CSRD, while the masculinity dimension has a negative relationship with CSRD. The findings imply that the institutional environment influences CSRD through all three pillars with some institutional factors having a greater impact than others.

A study on assessment of the Determinants and Consequences of Corporate Social Responsibility Disclosure in Jordan from 2010-2015

| [2] | Alkayed, H. A.-M. (2018). The Determinants and Consequences of Corporate Social Responsibility Disclosure: The Case Of Jordan. Manchester, United kingdom: Published PhD theses by the University of Salford. |

[2]

. Agency, Stakeholder, and Legitimacy theories were used to underpin the doctoral dissertation. A qualitative approach and Content Regression Analysis were used in the study; the result shows that the extent of CSD is high quality in Jordan. The result also revealed that board size, non-executive directors, firm’s age, foreign members on the board, number of boards meetings, the presence of audit committees, big four

| [4] | Amin M. R. 2025 sustainability reporting and its influence on investors decision making; critical perspective and empirical insight. International journal of science and research archive 6(1). |

[4]

, government ownership, firm’s size, industry type were found to have a significant relationship with both extent and quality of CSD while the non-executive member was found not have a significant relationship with the extent of CSD: Concerning CSD consequences, the result shows that CSD has a positive and significant impact on company performance (ROA) and market value. This result provides evidence for policymakers (Jordan security commission and other regulators around the world) of the importance of CSD and its impact on a company’s performance, and that companies should consider this type of disclosure more in their annual reports.

A study on effect of corporation boards, audit committees on voluntary disclosure, evidence from Italian-listed companies

| [1] | Allegrini, M., & Greco, G. (2013). Corporate Boards, Audit Committees and Voluntary Disclosure: Evidence from Italian Listed Companies. Journal of Management and Governance, 17(1). |

[1]

. The paper investigated the interplay between governance proxied by the independence of the board, size of the Board, CEO duality, Director's independence, the diligence of the Board and audit committee, and voluntary disclosure. This secondary-based research and regression were used to test the hypothesis. The outcome of the examination revealed the presence of a connection between governance and disclosure. In addition, audit and board committee diligence are positively associated with voluntary disclosure. The finding also revealed that board has a significant correlation with voluntary disclosure while CEO duality is negatively correlated with disclosure. Firm size shows a significant positive relationship while no significant relationship was observed between profitability and listing status and voluntary disclosure.

According to a study conducted by Fan et al (2024)

| [8] | Fan J., Muhamad H., Said R. M. and Daud R. M 2024 Do institutional pressure impact voluntar enviromental information disclosure? bangledesh journal of multidisolinar scientific research vol 9(5). |

[8],

if institutional pressure impact voluntary environmental information disclosure. A sample of listed manufacturing companies based in china was taken. Data was obtained between march to May 2024 and PLS-SEM was used to analyse the data. Finding revealed that normative and coercive pressures influences voluntary disclosure while mimetic pressure no significant effect. The outcome also revealed that companies prioritize compliance with regulator standard rather than imitating the behaviours of others.

In their study Jahid et al 2023

| [12] | Jahid M. D., Yaya R., Pratolo S. and Pribadi F. (2023) institutional factors and CSR reporting in developing countr- evidence from the neo-institutional perspective. Cogent Business and Mangement journal vol 10(1). |

[12]

examined institutional factors and CSR reporting in developing country- evidence from the neo-institutional perspective. Purposive sampling technique was used to select sample size. Total of 272 DSE listed companies was taken from 2017-2021. Content analysis approach was adopted to compute the data while OLS regression model was used to test the hypothesis. Findings revealed that CSR reporting is positively and significantly associated with country institutional environment. Specifically, findings also showed that presence of CSR guideline, reform on corporate governance, audit firm and firm GRI registration has positive impact on CSR reporting. it was therefore recommended that rigorous attention should be paid to the policy level and managerial implication.

Coliccia et al 2023

| [6] | Collucia D., Fantana S., and Solimene S. 2018 Does institutional context affect CRS disclosure? A study on Eurostoxx 50. Sustainability journal vol. 10(8). |

[6]

who examined if institutional context affects CSR disclosure, a study on Euostoxx 50. A multivariate regression was used to test the hypothesis. Findings revealed that legal system do affect the disclosure on CSR.

From the empirical reviews put together on the effect of institutional factors on corporate sustainability disclosure, it had been revealed that a good number of the studies carried out have considered GRI adoption and or legal as mainly institutional factor but this study used CSR committee and membership as additional factors. To add to that, the available research has focused on areas such as manufacturing, banks, oil and gas, food production, and so on, only a small number (insignificant) have studied the health care sector which may be considered among the least compliant sector. Furthermore, the previous studies have always based their works on the common theories of agency, stakeholders as well as legitimacy. This current study used institutional theory instead of the already existing theories commonly used in CSD. Finally, it was also observed from the literature that only a few out of the reviews originated from Africa and even in Nigeria, the number is still scarce. Therefore, this study fills the gap in the literature by conducting research in Africa and particularly Nigeria.

Theoretical Review

Institutional theory was first founded by

| [16] | Selznick, P. (1957). Leadership in administration: a sociological interpretation. New york: harper and row. |

[16]

in 1957. It is based on the assumption that organisation do not act only based on efficiency or profit motive but they also behave in way that conform to social rule, norms expectation and pressure in their work environment in order to gain legitimacy. It strengthens the dependent association between an organisation and environment. On the other hand, companies and their practices are molded by business related i.e. institutional factors in the corporate environment and one of these practices is sustainability. Sustainability practice has recently gained relevance especially in stakeholders’ decision making as it covers social, environmental and governance concern in addition to economic. Institutional theory lingers on answering question on institutional factors because it mainly concentrated on customs and obligations, such as bylaws, rules, cultural demands, social comparison processes, or belief systems. Healthcare companies are highly regulated organisation, therefore professionalism is essential in las much as performance. Since institutional pressure environmental factor) do exist in the system, these companies would want to comply with rules, regulations, norms and culture as a means to gain legitimacy. Hence the need to disclose more information including sustainability disclosures. Therefore, to safeguard both present and future, legitimate compliance with institutional factors, for proper accountability, sustainability, and disclosure, the institutional theory will be accepted to pilot this research.

3. Methodology

Research design adopted is the combination of both qualitative and quantitative designs. Qualitative design i.e. descriptive statistic was used because numerical data are to described in order to answer the research question, including mean, standard, minimum and maximum while quantitative i.e. inferential statistic was used because it allows for test of hypothesis. Regression analysis was used to test the hypothesis. The study sampled 7 healthcare companies listed on the Nigerian exchange group for period of 10 years from 2011-2020, selected based on criteria adapted in work of

| [9] | Garko, J. S. (2014). Corporate Governance And Voluntary Disclosure In The Nigerian Listed Industrial Goods Companies. Kano: An Unpublished PhD Theses in Accounting and Finance submitted to Bayero University Kano. |

[9]

. Panel data was extracted from the annual report of the selected companies. The objective of the study was just to demonstrate a simple relationship i.e. average effect across health care firms rather than within temporal variation and in this context, OLS provide efficient and consistent estimator when unobserved firm effect is not statistically significant. Therefore, it was used.

Furthermore, some diagnostic tests were conducted in order to ensure the validity of all statistical inferences for the study, and assessing the impact of distribution problems in addition to the problems of outliers before deciding on the appropriate statistical method to use. The tests include Multicollinearity, heteroscedasticity, normality of residuals, and skewness and kurtosis tests. These are discussed below:

Multi-Collinearity Test

A VIF above 10 should be taken as an indication of harmful Multi-collinearity (Gujarati, 2003).

Table 3 indicates that the Multi-collinearity test was carried out using VIF and the results show an average VIF of 1.02 and which is less than 10 which indicates the absence of Multi-collinearity.

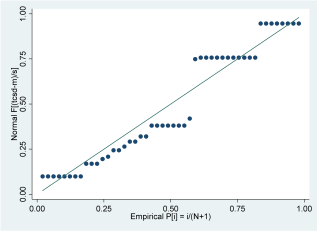

Normality Test of the Residuals

Figure 2. Probability P-Plot for Normality test of the dependent Variable.

Normality implies that errors (residuals) should be normally distributed. Fitness and normality are ensured when the p-plot does not deviate significantly from the line of best fit (Gujarati, 2003). The study used a normal probability plot test for this purpose on the dependent variable. The normal p-plot of the regression standardized residual (

Figure 2) indicates a good fit and does not suggest the presence of outliers among the regression standardized residuals. In other words, the points on the plot do not appear to deviate significantly from the line of best fit indicating that the normality assumption is valid.

Heteroscedasticity Test

The presence of heteroscedasticity signifies that the variation of the residuals or term errors is not constant. Ideally, the model should be homoscedastic for OLS (ordinary least square) regression to be accepted as the BLUE (best linear unbiased estimators). However, the heteroscedastic situation exerts an effect on the inferences drawn with regard to the beta coefficient, coefficient of determination (R2), and t-statistics of the model. Test of heteroscedasticity ensures that the regression model fits all the values of the independent variables and this is possible only if the residuals do not vary with the independent variable and therefore are random. The result of the Breusch-pagan/Cook-Weisberg test for heteroscedasticity reveals that the data is homoscedastic and not heteroscedastic. This is evidenced by the insignificant p-value of 0.9315 for model. This signifies the absence of heteroscedasticity and the presence of homoscedasticity in the model. In this study, OLS regression was used due to the presence of homoscedasticity.

Skewness and kurtosis Test

Skewness and Kurtosis test carried out on all the variables indicates that none of the variables are highly skewed. There is no need to normalize the variable data found not to be highly skewed using Winsorization or data clipping.

Table 1. Variables and Measurements.

Independent variables (Institutional Factors) |

SGL | It was scored as “1” if companies comply with guideline and “0” otherwise, then averaged between observed and expected to obtain the outcome ratio utilized in the study | [14] | Nwobu, O. A. (2017). Determinants of Corporate Sustainability Reporting in selected companies in Nigeria. Ota, Nigeria: An Unpublished Phd Thesis in Accounting, Covenant University. |

[14, |

MEM | It was scored as “1” if companies belong to any of the mentioned groups and “0” if otherwise, then averaged between observed and expected to obtain the outcome ratio utilized in the study | [14] | Nwobu, O. A. (2017). Determinants of Corporate Sustainability Reporting in selected companies in Nigeria. Ota, Nigeria: An Unpublished Phd Thesis in Accounting, Covenant University. |

[14, |

PSC | It was scored “1” where a company has a committee on sustainability and “0” where it does not have a sustainability committee. The observed are then averaged against the expected to obtain the outcome ratio utilized in the study | [15] | Mahmood Z. Kouser R., Ali W., Ahmad Z& Salma T. (2018), Does corporate governance affect sustainability disclosure? A mixed method study. Sustainability 10(1). |

[15, |

Dependent variable (TCSD) | ] |

Source: Authors Design 2025.

The model can be specified below

Where

TCSD - Average Corporate Sustainability Disclosure

INSTFCT= Institutional factors (SGL, PSC. MEM)

Measurement approach of Total Corporate Sustainability Disclosure (TCSD)

Sustainability disclosure is found in corporate annual reports and or stand-alone sustainability reports depending on the choice of the company. A disclosure index will be used to ascertain the disclosure level of such information in annual reports or sustainability reports. The disclosure index consists of list of three to four reporting components known as the TBL or CSR. This procedure to measuring the dependent variable is not new to the sustainability reporting literature as it has been used in past studies such as Ong (2016), Brey and Haavaldsen (2014) and Selvanathan (2012). In this study, there are four (4) indicators of corporate sustainability disclosure namely economic, social, governance and environmental. The content analysis approach will be used in this study. Healthcare sector companies will be scored on the disclosure index made up of corporate sustainability disclosure indicators guideline as adapted from GRI and Nigerian sustainability guideline (2015).

Previous literature has shown that the CSD can be measured either through weighted or non-weighted techniques (see Gao, Heravi, & Xiao, 2005). Weighted presence of information on checklist items (Noah, 2017; Binti-Mokhtar, 2015; Garko, 2014) have been applied to measure the degree of CSD in some past researches. This was applied to measure the extent of CSD in the financial statements of firms in Nigeria’s healthcare sector. This is because, the use of weighted index presence of information on checklist items is considered more suitable as the use of unweighted index (word count, sentence count or page count) could create subjectivity and bias during the analysis.

Mathematically, the sustainability reporting index can be computed as follows:

ESDI= EECI + EENI + ESCI + EGVI

Where

ESDI: Expected Sustainability Disclosure Indicators

EECSSDI: Expected Economic Indicators

EENVSDI: Expected Environmental Indicators

ESSDI: Expected Social Indicators

EGSSDI: Expected Governance Indicators

CSDI: Corporate Sustainability Disclosure Index

OECSSDI: Observed Economic Indicators

OENVSDI: Observed Environmental Indicators

OSSDI: Observed Social Indicators

OGSSDI: Observed Governance Indicators

4. Result and Findings

Table 2. Descriptive Statistics.

VARIABLES | OBS. | MEAN | STD. DEV. | MINIMUM | MAXIMUM |

TCSD | 70 | 0.44958 | 0.2119 | 0.1800 | 0.9339 |

INSTFCT | 70 | 0.2810 | 0.2817 | 0 | 0.6667 |

Source: Research Output, 2025

Table 2 depict the descriptive statistics for the data obtained with observation of 70. The average sample value is 0.445 which is below midpoint of 0-1 scale. Standard deviation is 0.212 while mean is 0.445 relative spread 48% is moderately high. That means values are fairly spread out around the mean. The range is wide at 0.754 and maximum 0.9339 is much farther from the mean of 0.18 is, this suggest a right positive skew. The 95% confidence interval for the mean indicates the mean is estimated reasonably precisely given 70, we can be 5% confident to the population mean lies in that interval under standard assumption.

The mean total for institutional factor on corporate sustainability disclosure of healthcare companies in Nigeria shows an average of about 0.28, this means that there is an average of 28% institutional factor pressure in the industry. The standard deviation of 0.28 indicates that there is no significant variation in institutional factor elements between the sampled healthcare companies during the period of the study with a minimum level of 0% and a maximum of 67% institutional factor elements.

Table 3. Correlation of the Dependent and Explanatory.

VARIABLES | TCSD | INSTFCT. | VIF |

TCSD | 1.0000 | | |

INSTF | 0.9070 | 1.0000 | 1.02 |

Source: Research Output, 2025

Table 3 contains the correlation matrix of the dependent and independent variables of the study. The outcome reveals a strong positive relationship between institutional factors and corporate sustainability disclosure. This implies that s institutional pressure increases, corporate sustainability disclosure increases. R coefficient of +0.91 is close to perfect which implies that the variables move together very consistently and in the same direction. A VIF value below 5 mean no multicollinearity issue. i.e. institutional factor does not highly correlate with other predictors in the model.

Table 4. OLS Regression Results for Hypothesis.

Variables | Coefficient | t | p>/t/ |

Constant | 0.1121774 | 0.73 | 0.469 |

INSTFCT | 0.5294842*** | 18.23 | 0.0000 |

R2 | | | 0.9291 |

Prob > F | | | 0.0000 |

Source: Research Output, 2025

Table 4 present the test for main effects, coefficients, and p-values of the OLS multiple regression model result on TCSD institutional factors proxied by sustainability guideline, presence of sustainability committee and membership in advocacy group. The constant of 0.1121 indicates that even in the absence of institutional factors pressure firms disclose sustainability information at baseline level 11.2%. This suggest that some level of sustainability disclosure occurs voluntarily or due to internal motivations. The beta coefficient of 0.5295 shows a positive and substantial relationship between institutional factors pressure and corporate sustainability disclosure. Specifically, one-unit increase in institutional pressure leads to an average increase of 52.95% in the level of sustainability disclosure holding other factors constant. This implies that stronger institutional factors pressure such as regulatory requirement professional norms and stakeholder expectations encourage firms to disclose more sustainability information.

Table 3 revealed an R

2 (0.93) which is the multiple coefficients of determination that gives the proportion or percentage of the total variation in the dependent variable (Total corporate Sustainability Disclosure) explained by institutional factors. Hence, it indicates that 92% of the total variation in the extent of TCSD in listed healthcare companies is caused by institutional factors while the remaining 8% of the total variation in the extent of TCSD is caused by factors not explained by the model, captured by stochastic disturbance term. This explain an excellent model with a high explanatory power.

This is further substantiated by the fact that a f-Prob of 0.000 is less than a 0.05 level of significance. Since the f-Prob is less than α, the null hypothesis is rejected. Hence, it can be concluded that there is a significant relationship Institutional Factors and Corporate Sustainability Disclosure of listed Healthcare Sector Companies in Nigeria. This implies that the observed relationship is not due to chance. This outcome is inline with the works

| [13] | Kilic M., Uyar A. Kuzey C. Kanaman A. S. (2021): Drivers and consequences of sustainability committee existence? Evidence from the hospitality and tourism industry. International journal of hospitality management vol. 92. |

| [14] | Nwobu, O. A. (2017). Determinants of Corporate Sustainability Reporting in selected companies in Nigeria. Ota, Nigeria: An Unpublished Phd Thesis in Accounting, Covenant University. |

[13, 14]

.

Author Contributions

Yagana Alhaji Baba: Conceptualization, Data curation, Formal Analysis, Investigation, Methodology, Supervision, Writing – original draft, Writing – review & editing

Bukar Zannah Waziri: Conceptualization, Formal Analysis, Funding acquisition, Investigation, Methodology, Project administration, Writing – original draft, Writing – review & editing

Amina Ahmed Idriss: Funding acquisition, Investigation, Methodology, Validation, Writing – review & editing