1. Introduction

Over the last half-century, most nations have witnessed significant financial development, and Ghana is no exception. In several countries, the causal issue behind financial development is the problem of public debt. As inferred by Gaspar

| [1] | Gaspar, V., Amaglobeli, M. D., Garcia-Escribano, M. M., Prady, D., & Soto, M. (2019). Fiscal policy and development: Human, social, and physical investments for the SDGs. International Monetary Fund. |

[1]

, financial development necessitates investment in infrastructure, education, social welfare, health and other sectors of the economies. The enormous expenditures associated with such investments make it challenging for nations to fund them from tax revenues, frequently leading to budget deficits.

Budget deficits triggered by such investments must be financed; nevertheless, the key question confronting policymakers and most government economists is how the budget deficit must be funded. Public finance provides three (3) alternative sources of financing deficits: taxes, debts and user fees

| [2] | Florea, N. M., Bădîrcea, R. M., Meghisan-Toma, G. M., Puiu, S., Manta, A. G., & Berceanu, D. (2021). Linking public finances’ performance to renewable-energy consumption in emerging economies of the European Union. Sustainability, 13(11), 6344. https://doi.org/10.3390/su13116344 |

| [3] | Rosen, H. S., & Gayer, T. (2008). Public finance (internat. ed). Boston, Mass. |

[2, 3]

. Developing countries with weak tax regimes and low incomes opt for debt as the best option for financing the government budget. Given this, it is not shocking that public debt plays a predominantly vital role in developing nations

| [4] | Eichengreen, B. J., El-Ganainy, A., Esteves, R., & Mitchener, K. J. (2021). In defense of public debt. Oxford University Press. |

| [5] | Salsman, R. M. (2017). The political economy of public debt: three centuries of theory and evidence. Edward Elgar Publishing. |

| [6] | Schularick, M. (2016). Public debt and financial crises in the twentieth century. In Economic Crises and Global Politics in the 20th Century (pp. 33-49). Routledge. |

[4-6]

. Public debt allows financial authorities to play their part in stabilizing their economies and stimulating aggregate growth.

Incidentally, Ghana is no exception to borrowing. Its existing lower middle-income economic standing makes it germane for the nation to incessantly invest in the productive sectors of the economy to guarantee sustained growth

. Ghana has a fragile tax system, and consequently, the nation does not create sufficient tax revenues to fund its expenditures. Thus, taxes are not viewed as a good option for funding budget deficits

| [9] | Fiscal Alert (2018). The Growing Ghana’s Public Debt and its Implications for the Economy. Institute for Fiscal Studies. No. 11. Cantonments, Accra. www.ifsghana.org |

[9]

.

Furthermore, most of the informal sector of Ghana’s economy is excluded from the country’s tax base owing to the lack of an accurate database, making it difficult for Ghana’s tax system to track their economic activities and tax them accordingly

| [10] | Wiafe, P. A., Armah, M., Ahiakpor, F., & Tuffour, K. A. (2024). The underground economy and tax evasion in Ghana: Implications for economic growth. Cogent Economics & Finance, 12(1), 2292918. https://doi.org/10.1080/23322039.2023.2292918 |

| [11] | Appiah, T., Domeher, D., & Agana, J. A. (2024). Tax Knowledge, Trust in Government, and Voluntary Tax Compliance: Insights From an Emerging Economy. SAGE Open, 14(2), 21582440241234757. https://doi.org/10.1177/21582440241234757 |

| [12] | Mugano, G. (2024). Payment of Taxes: Challenges and Options. In SMEs and Economic Development in Africa (pp. 70-84). Routledge. |

| [13] | Amoh, J. K., & Adafula, B. (2019). An estimation of the underground economy and tax evasion: Empirical analysis from an emerging economy. Journal of Money Laundering Control, 22(4), 626-645. https://doi.org/10.1108/JMLC-01-2019-0002 |

| [14] | Joshi, A., Prichard, W., & Heady, C. (2013). Taxing the informal economy: Challenges, possibilities and remaining questions. IDS Working Papers, 2013(429), 1-37. |

[10-14].

The specified policy of Ghana is to follow prudent macroeconomic policies to recover the socioeconomic situations and welfare of its people through sound fiscal policies like government spending in the areas of education, health, defence, infrastructure and other social services

| [7] | Awadzie, D. M., Garr, D. K., & Tsoekeku, T. D. (2022). The Relationship Between Economic Growth and Public Debt: A Threshold Regression Approach in Ghana. Journal of Business Economics and Finance, 11(1), 15-23. https://doi.org/10.17261/Pressacademia.2022.1549 |

| [15] | Fumey, A., Bekoe, W., & Imoru, A. (2022). External Debt Servicing and Capital Formation in Ghana: An Autoregressive Distributed Lag Analysis. European Journal of Economic and Financial Research, 6(1). http://dx.doi.org/10.46827/ejefr.v6i1.1272 |

[7, 15]

. This necessitates that the government borrows from both local and international financial markets, the World Bank and the International Monetary Fund, to finance development projects

.

Ghana’s total debt as of 2013 was $15.83 billion, which is about 33% of total GDP

| [17] | IMF Economic Outlook (2013), World Economic Outlook: Transitions and Tensions, IMF, Washington, DC. |

[17]

. Studies have underscored the implication of public debt on economic growth

| [18] | Yusuf, A., & Mohd, S. (2021). The impact of government debt on economic growth in Nigeria. Cogent Economics & Finance, 9(1), 1946249. https://doi.org/10.1080/23322039.2021.1946249 |

| [19] | Ahlborn, M., & Schweickert, R. (2018). Public debt and economic growth–economic systems matter. International Economics and Economic Policy, 15, 373-403. https://doi.org/10.1007/s10368-017-0396-0 |

| [20] | Panizza, U., & Presbitero, A. F. (2014). Public debt and economic growth: is there a causal effect?. Journal of Macroeconomics, 41, 21-41. https://doi.org/10.1016/j.jmacro.2014.03.009 |

| [21] | Calderón, C., & Fuentes, J. R. (2013). Government debt and economic growth (No. IDB-WP-424). IDB working paper series. |

| [22] | Kumhof, M. M., & Tanner, M. E. (2005). Government Debt: A Key Role in Financial Intermediation (EPub) (No. 5-57). International Monetary Fund. |

[18-22]

. Nevertheless, few empirical studies have explored the impact of public debt on developing economies. This study attempts to fill this gap in the literature as rising public expenditures in the context of persistently weak revenue performance have undermined Ghana’s fiscal and debt sustainability in current times.

Again, as the nation’s fiscal risks remain high, sound fiscal consolidation is essential to reverse the negative debt dynamics and decrease domestic refinancing risks. The government’s fiscal management strategy aims to reestablish fiscal discipline, reverse its inherited fiscal decline, and put the public debt on a downward and sustainable path

. Regrettably, it does not seem the government is winning the debt stability war, as overall public debt continues to increase with grave economic consequences

| [9] | Fiscal Alert (2018). The Growing Ghana’s Public Debt and its Implications for the Economy. Institute for Fiscal Studies. No. 11. Cantonments, Accra. www.ifsghana.org |

[9]

.

This study, thus, seeks to comprehend how rising government debt influences financial institutions, market structures, investment climates, and overall economic growth in the country and identify and assess policy measures that could mitigate adverse effects and promote sustainable financial development amidst high public debt levels.

The significance of the current study therefore, stems from the fact that, first, public debt has become a significant concern for policymakers and economists worldwide, particularly in developing countries such as Ghana. The study will, thus, provide vital insights into public debt and economic development, which can inform policymaking and help balance the need for investment in infrastructure and social programs while ensuring long-term sustainability and financial stability.

Secondly, the study’s qualitative analysis of public debt and economic development nexus has vital implications in Ghana’s context as the nation has experienced a significant increase in public debt levels in recent years, and policymakers need to prudently manage public finances to guarantee long-term sustainability while promoting financial development and economic growth

. The study’s findings can help identify appropriate policies that promote economic development while maintaining sustainable public debt levels.

Also, the study’s discoveries have broader implications for developing countries worldwide, where public debt levels are a significant concern. By shedding light on public debt and economic development, the study can inform policymaking and assist in promoting sustainable economic growth and development. Furthermore, the literature indicates limited studies undertaken in this area qualitatively and primarily focused on only public external debt (see, for instance,

| [7] | Awadzie, D. M., Garr, D. K., & Tsoekeku, T. D. (2022). The Relationship Between Economic Growth and Public Debt: A Threshold Regression Approach in Ghana. Journal of Business Economics and Finance, 11(1), 15-23. https://doi.org/10.17261/Pressacademia.2022.1549 |

| [70] | Prah, G. J., & Ofori, C. (2022). External Debt and Foreign Investment: An Empirical Analysis on the Economy of Ghana. Eurasian Journal of Economics and Finance, 10(2), 54-67. https://doi.org/10.15604/ejef.2022.10.02.002 |

[7, 70]

.

Literature Review

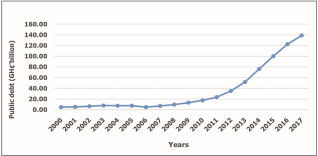

As indicated earlier, Ghana’s debt stock has increased astronomically over the last decade, with grave economic consequences. Total public debt stood at GH¢4.92 billion in 2000 and rose to GH¢8.0 billion by 2003, representing an increase of 62.6%. By the end of 2006, Ghana’s debt had dropped to GH¢4.90 billion after its relief from the Highly Indebted Poor Country (HIPC) and the Multilateral Debt Relief Initiative (MDRI). Subsequently, the country’s debt started to rise, reaching GH¢9.7 billion in 2008, mirroring the hefty fiscal deficit noted in the year and the effect of the cedi depreciation on the external debt. Total public debt continued increasing, reaching GH¢35.1 billion by the end of 2012 and by end-2016, the debt stock had soared to GH¢122.6 billion. The debt stock continued to increase, reaching GH¢138.9 billion in September 2017 (

Figure 1) and GH¢575.7 billion in 2022

| [24] | Ministry of Finance (MoF) (2022). Mid-Year Fiscal Policy Review of the 2022 Budget Statement and Economic Policy of the Government of Ghana. Presented to Parliament on Monday, 25th July, 2022 by Ken Ofori-Atta Minister for Finance. available at: www.mofep.gov.gh |

[24]

.

External debt has constituted much of Ghana’s total public debt for most of the post-HIPC/MDRI period. The sharp surge in Ghana’s public debt over the last decade has grave consequences for economic growth because of the related high debt servicing cost and the exposure of the economy to the fluctuations of external shocks

| [15] | Fumey, A., Bekoe, W., & Imoru, A. (2022). External Debt Servicing and Capital Formation in Ghana: An Autoregressive Distributed Lag Analysis. European Journal of Economic and Financial Research, 6(1). http://dx.doi.org/10.46827/ejefr.v6i1.1272 |

[15]

. Ghana did not experience any severe decline in debt sustainability and high-risk of debt distress through the six-year period between 2006 and 2012. The amalgamation of a more ambitious fiscal consolidation, in conjunction with more robust real GDP growth as well as higher export levels, contributed to a more promising sustainability of the country’s debt between 2009 and 2012. Notwithstanding the debt build-up during this period, the economy did not display any severe sign of debt distress, as the debt-to-GDP ratio touched only 48.4% by the end of 2012.

Ghana started to face a high risk of debt distress in 2014 as the total debt liabilities grew and the nation’s debt service-to-revenue ratio approached high-risk levels. As a result of weak fiscal policy, worsening financing terms and external pressures, much of the nation’s public domestic and external debt indicators deteriorated

| [25] | Amankwah, G., Ofori-Abebrese, G., & Kamasa, K. (2018). An empirical analysis of the sustainability of public debt in Ghana. Theoretical Economics Letters, 8(11), 2038. https://doi.org/10.4236/tel.2018.811133 |

[25]

. The total public debt service-to-revenue ratio was not only on a fast-increasing path but also breached its indicative long-term threshold. Debt service riveted a large part of domestic revenue. According to the Fitch Rating Agency, Ghana’s downgrade mirrors the deterioration of Ghana’s public finances, which has contributed to a protracted lack of access to Eurobond markets, sequentially leading to a significant decline in external liquidity.

Also, the country’s medium-term debt trajectories are on an upward trend, with grave consequences for interest payment commitments. Contingent liabilities, particularly from state-owned enterprises and domestic payment arrears, also present additional risks to the country’s debt sustainability

| [9] | Fiscal Alert (2018). The Growing Ghana’s Public Debt and its Implications for the Economy. Institute for Fiscal Studies. No. 11. Cantonments, Accra. www.ifsghana.org |

[9]

. Thus, as of June 2022, Ghana’s total public debt was GHS393 billion, representing 78.3% of GDP), consistent with Bank of Ghana (BoG) and finance ministry data.

Debt sustainability analysis categorizes countries into four (4) basic bands: low risk, moderate risk, high risk, and debt distress

. This is based on specific thresholds for core public debt indicators. Ghana’s preceding analysis, conducted in mid-2021, categorized the nation as high risk of external debt distress and overall debt distress

. The evaluation was conducted jointly by the IMF and the World Bank.

Aizenman and Jinjarak

| [26] | Aizenman, J., & Jinjarak, Y. (2012). The fiscal stimulus of 2009-2010: Trade openness, fiscal space and exchange rate adjustment. Journal of International Money and Finance, 31(4), 887-903. |

[26]

assert that the nexus between public debt and financial growth is non-linear. At lower levels of public debt, the effect on economic growth is positive, while at higher levels, it becomes negative. They noted that economic development could moderate the adverse effect of public debt on financial growth, implying that a well-developed financial system can help mitigate the adverse effects of high public debt levels on financial growth. Similarly, Cecchetti and Mohanty

| [27] | Cecchetti, S. G., & Mohanty, M. S. (2012). Emerging market economies and the world monetary system. Economic Policy, 27(69), 285-329. |

[27]

believe that high public debt levels can lead to lower economic growth rates, but the effect is more severe in countries with underdeveloped financial systems. They argue that a well-developed financial system can help absorb the impact of high public debt and facilitate economic growth.

Contrary to the above beliefs, Reinhart and Rogoff

suggested that the relationship between public debt and financial growth is negative, regardless of the level of financial development. They argue that high public debt levels led to increased interest rates, which crowd out private investments and reduce financial growth. However, more recently, Panizza et al.

challenged the conclusions of Reinhart and Rogoff

, arguing that the negative relationship between public debt and financial growth is conditional on several factors, such as the level of financial development, the type of debt (internal or external), and the composition of debt (domestic or foreign currency). They also found that financial development can mitigate the adverse effects of public debt on financial growth.

Afonso and Sousa

suggest that the positive effect of public debt on financial development is contingent on the level of financial development. Financial development has also been shown to play a crucial role in the relationship between public debt and financial growth. Financial development can increase public debt's effectiveness by improving resource allocation, lowering transaction costs, and improving the overall efficiency of the financial system

| [36] | Pradhan, R. P., Arvin, M. B., & Bahmani, S. (2018). Are innovation and financial development causative factors in economic growth? Evidence from a panel granger causality test. Technological Forecasting and Social Change, 132, 130-142. https://doi.org/10.1016/j.techfore.2018.01.024 |

| [37] | Cheng, Y. S., & Tan, L. (2017). The impact of public debt on financial development in emerging markets. Economic Systems, 41(3), 434-447. |

| [38] | Ductor, L., & Grechyna, D. (2015). Financial development, real sector, and economic growth. International Review of Economics & Finance, 37, 393-405. https://doi.org/10.1016/j.iref.2015.01.001 |

| [39] | Hauner, D. (2009). Public debt and financial development. Journal of development economics, 88(1), 171-183. https://doi.org/10.1016/j.jdeveco.2008.02.004 |

[36-39]

.

Thus, financial development is a vital characteristic of economic development and is widely recognized as a key factor in reducing poverty and promoting economic development. Hence, it has been well-established in both theoretical and empirical literature that financial development is required for economic growth

| [31] | Sarwar, A., Khan, M. A., Sarwar, Z., & Khan, W. (2021). Financial development, human capital and its impact on economic growth of emerging countries. Asian Journal of Economics and Banking, 5(1), 86-100. https://www.emerald.com/insight/2615-9821.htm |

| [32] | Bist, J. P. (2018). Financial development and economic growth: Evidence from a panel of 16 African and non-African low-income countries. Cogent Economics & Finance, 6(1), 1449780. https://doi.org/10.1080/23322039.2018.1449780 |

| [33] | Anwar, S., & Nguyen, L. P. (2011). Financial development and economic growth in Vietnam. Journal of Economics and Finance, 35, 348-360. https://doi.org/10.1007/s12197-009-9106-2 |

| [34] | Rousseau, P. (2003). Historical perspectives on financial development and economic growth. Federal Reserve Bank of St. Louis Review, 85(Jul), 81-106. https://doi.org/10.3386/w9333 |

| [35] | Levine, R. (1997). Financial development and economic growth: Views and agenda. Journal of Economic Literature, 35(2), 688-726. https://www.jstor.org/stable/2729790 |

[31-35]

. It involves the broader use of prevailing financial instruments and the formation and adoption of innovative ones for intermediating funds and handling risk

| [40] | Broner, F. A., & Ventura, J. (2010). Rethinking the effects of financial liberalization (No. w16640). National Bureau of Economic Research. https://doi.org/10.3386/w16640 |

[40]

. For Africa, particularly sub-Saharan Africa, with external demand and financing situations suggestively deteriorating and a much less promising growth outlook for the area, recognizing unexploited and underutilized sources of growth and decreasing the unpredictability of that growth has become crucial.

Mlachila et al.

| [41] | Mlachila, M. M., Jidoud, A., Newiak, M. M., Radzewicz-Bak, B., & Takebe, M. M. (2016). Financial development in Sub-Saharan Africa: promoting inclusive and sustainable growth. International Monetary Fund. |

[41]

asserted that whereas discussions have revolved around whether financial development is an engine for development or merely a lubricant, any feature that can meaningfully ameliorate development prospects for Africa is worth exploring in detail. Theoretically, financial development affects growth through several important channels for sub-Saharan Africa as it aids in catalyzing savings into more practical forms and supports the effectual distribution of capital and improvement of total factor productivity

| [41] | Mlachila, M. M., Jidoud, A., Newiak, M. M., Radzewicz-Bak, B., & Takebe, M. M. (2016). Financial development in Sub-Saharan Africa: promoting inclusive and sustainable growth. International Monetary Fund. |

[41]

.

Also, financial development supports diversification and management of risk and decreases information asymmetries, as well as transaction and monitoring costs. Ndung’u and Oguso

| [42] | Ndung’u, N., & Oguso, A. (2021). Financial sector development and financial inclusion in Africa: gaps, challenges and policy options. In Inclusive Financial Development (pp. 28-51). Edward Elgar Publishing. https://doi.org/10.4337/9781800376380.00008 |

[42]

specified that economic development could decrease the economy’s volatility by providing a wide range of instruments and statistics to assist households and businesses in tackling adverse shocks through consumption and investment smoothing.

Levine

| [43] | Levine, R. (2005). Finance and Growth: Theory and Evidence. In Aghion, P. and Durlauf, S. (Eds.), Handbook of Economic Growth (pp. 865-934). Elsevier |

[43]

discovered a strong relationship between financial development and growth. Thus, empirical studies infer that financial development has reinforced growth and reduced its precariousness in sub-Saharan Africa. Ductor and Grechyna

, for instance, noted that financial development had enabled other economic strategies to refine growth and stabilize the economy. Additionally, financial development can yield further gains by raising the median financial development index to its standard value

| [41] | Mlachila, M. M., Jidoud, A., Newiak, M. M., Radzewicz-Bak, B., & Takebe, M. M. (2016). Financial development in Sub-Saharan Africa: promoting inclusive and sustainable growth. International Monetary Fund. |

[41]

, which is related to a surge in growth by approximately 1.5% points and lower its volatility further. However, Shahbaz et al.

| [44] | Shahbaz, M., Mallick, H., Mahalik, M. K., & Hammoudeh, S. (2018). Is globalization detrimental to financial development? Further evidence from a very large emerging economy with significant orientation towards policies. Applied Economics, 50(6), 574-595. https://doi.org/10.1080/00036846.2017.1324615 |

[44]

infer that countries must be cautious about the evolving macro-financial risks to successfully manage the risks in financial development.

A very significant aspect of financial development - financial inclusion - decreases inequality of opportunity and alleviates the harmful effects of inequality on the level and durability of growth

| [45] | Van, L. T. H., Vo, A. T., Nguyen, N. T., & Vo, D. H. (2021). Financial inclusion and economic growth: International evidence. Emerging Markets Finance and Trade, 57(1), 239-263. https://doi.org/10.1080/1540496X.2019.1697672 |

| [46] | Ratnawati, K. (2020). The impact of financial inclusion on economic growth, poverty, income inequality, and financial stability in Asia. The Journal of Asian Finance, Economics and Business, 7(10), 73-85. https://doi.org/10.13106/jafeb.2020.vol7.no10.073 |

[45, 46]

. Thus, financial inclusion is a key factor in promoting financial development as it enables a wide range of individuals and businesses to access financial services. Financial inclusion is crucial for low-income households, as it can provide access to essential financial services such as savings accounts, credit, and insurance.

According to Joia et al.

| [47] | Joia, L. A., & Cordeiro, J. P. V. (2021). Unlocking the potential of fintechs for financial inclusion: A Delphi-based approach. Sustainability, 13(21), 11675. https://doi.org/10.3390/su132111675 |

[47]

, about 1.7 billion adults globally do not have access to formal financial services, and lack of financial inclusion is considered a major barrier to economic development in many developing countries. According to Claessens and Van Horen

| [48] | Claessens, S., & Van Horen, N. (2015). The Impact of the Global Financial Crisis on Banking Globalization. IMF Economic Review, 63(4), 868-918. https://doi.org/10.1057/imfer.2015.38 |

[48]

, financial inclusion is essential for promoting financial development because it provides access to financial services to a wide range of individuals and businesses. Financial inclusion can be achieved through various means, including mobile banking, microfinance, and other forms of financial technology.

Microeconomic and sociological studies remarkably suggest that financial inclusion aids produce better welfare results in society. Affirming the above arguments, empirical evidence advocates that financial development supports growth, particularly at lower levels of financial development, even though the effect on volatility is more varied. Studies demonstrate a positive impact but advocate the existence of a threshold beyond which financial development is detrimental to growth

| [49] | Machado, C. M., Saraiva, A. F., & Vieira, P. D. (2021). Finance-growth nexus in sub-Saharan Africa. South African Journal of Economic and Management Sciences, 24(1), 1-11. http://dx.doi.org/10.4102/sajems.v24i1.3435 |

| [50] | Arcand, J. L., Berkes, E., & Panizza, U. (2015). Too much finance?. Journal of Economic Growth, 20(2), 105-148. https://doi.org/10.1007/s10887-015-9115-2 |

[49, 50]

.

A recently fashioned financial development index by Svirydzenka

| [51] | Svirydzenka, K. (2016). Introducing a New Broad-based Index of Financial Development1. IMF Working Papers, 2016(005). |

[51]

and Sahay et al.

| [52] | Sahay, R., Čihák, M., N'Diaye, P., & Barajas, A. (2015). Rethinking financial deepening: Stability and growth in emerging markets. Revista de Economía Institucional, 17(33), 73-107. |

[52]

aids in demonstrating a more comprehensive measure of financial development globally. To measure sub-Saharan Africa’s performance in financial development over time, the index combines an assessment of countries’ financial institutions such as banks, insurance firms, mutual funds, pension funds, etc., and financial markets such as stock and bond markets.

It then captures the fact that many financial institutions provide financial services and that markets have advanced in a way that permits individuals and companies to diversify their investments and permits firms to raise capital beyond bank loans

| [51] | Svirydzenka, K. (2016). Introducing a New Broad-based Index of Financial Development1. IMF Working Papers, 2016(005). |

| [52] | Sahay, R., Čihák, M., N'Diaye, P., & Barajas, A. (2015). Rethinking financial deepening: Stability and growth in emerging markets. Revista de Economía Institucional, 17(33), 73-107. |

[51, 52]

. Since financial markets are comparatively underdeveloped and institutions are dominated by banks in numerous African nations, the index indicates the gap in financial services better than a one-dimensional measure like private credit to GDP. Both financial organizations and markets are measured based on depth, access, and efficiency. By including profitability indicators, the efficiency dimension of the index indicates that, notwithstanding sturdy growth in assets, the financial system in sub-Saharan Africa still lags behind other regions in terms of competition.

Regulatory frameworks also perform a critical role in promoting financial development. According to Demirguc-Kunt and Levine

| [53] | Demirguc-Kunt, A., & Levine, R. (2008). Finance and economic opportunity. Washington, DC: World Bank. |

[53]

, effective regulation can enhance financial stability and promote the development of financial institutions. Additionally, effective regulation can inspire innovation and competition, leading to new financial products and services. Regulatory frameworks are, consequently, critical for promoting financial development as they help to establish a stable and secure financial system that can support economic growth. Effective regulation can enhance financial stability and promote the development of financial institutions

| [54] | Anarfo, E. B., & Abor, J. Y. (2020). Financial regulation and financial inclusion in Sub-Saharan Africa: Does financial stability play a moderating role?. Research in International Business and Finance, 51, 101070. https://doi.org/10.1016/j.ribaf.2019.101070 |

| [57] | Mishkin, F. S., & Herbertsson, T. T. (2011). Financial stability in Iceland. In Preludes to the Icelandic financial crisis (pp. 107-159). London: Palgrave Macmillan UK. |

[54, 57]

. It can also inspire innovation and competition, leading to the development of new financial products and services.

One of the key aims of financial regulation is to guarantee the safety and reliability of financial institutions

| [58] | Jungo, J., Madaleno, M., & Botelho, A. (2022). The Effect of Financial Inclusion and Competitiveness on Financial Stability: Why Financial Regulation Matters in Developing Countries? Journal of Risk and Financial Management, 15(3), 122. https://doi.org/10.3390/jrfm15030122 |

[58]

. Regulatory bodies oversee the operation of financial institutions, set minimum capital requirements, and ensure that banks maintain sufficient reserves to meet their obligations. In addition, they monitor the credit quality of loans made by financial institutions and ensure that banks adhere to anti-money laundering and counter-terrorism financing regulations. Regulatory bodies can promote competition by ensuring a level playing field for new entrants and supporting smaller institutions. Furthermore, regulatory bodies can boost innovation by providing guidance on new products and services and fostering an environment that encourages experimentation and risk-taking

| [59] | Tarullo, D. K. (2019). Financial regulation: Still unsettled a decade after the crisis. Journal of Economic Perspectives, 33(1), 61-80. https://doi.org/10.1257/jep.33.1.61 |

| [60] | Botha, E., & Makina, D. (2011). Financial regulation and supervision: Theory and practice in South Africa. International Business & Economics Research Journal, 10(11), 27-36. https://doi.org/10.19030/iber.v10i11.6402 |

| [74] | Laeven, L., Levine, R., & Michalopoulos, S. (2015). Financial innovation and endogenous growth. Journal of Financial Intermediation, 24(1), 1-24. https://doi.org/10.1016/j.jfi.2014.04.001 |

[59, 60, 74]

.

In many countries, the regulation of financial institutions is the responsibility of a central bank or other government agency. However, it is imperative to guarantee that regulatory bodies are independent and have the resources and expertise required to carry out their responsibilities effectively. Regulatory bodies must be transparent and accountable and engage with stakeholders to ensure appropriate and effective regulations

| [56] | Ackah, C., & Asiamah, J. P. (2016). Financial regulation in Ghana: Balancing inclusive growth with financial stability. In Achieving financial stability and growth in Africa (pp. 107-121). Routledge. |

| [60] | Botha, E., & Makina, D. (2011). Financial regulation and supervision: Theory and practice in South Africa. International Business & Economics Research Journal, 10(11), 27-36. https://doi.org/10.19030/iber.v10i11.6402 |

[56, 60]

. Consequently, regulatory frameworks are essential for promoting financial development. Effective regulation can enhance financial stability, encourage competition and innovation, and promote financial inclusion. Policymakers must focus on creating a regulatory environment that supports the development of a safe, sound, and innovative financial sector while ensuring that regulatory bodies are transparent, accountable, and have the resources and expertise needed to carry out their responsibilities effectively.

Capital markets are also an essential aspect of financial development. A well-functioning capital markets can promote economic growth by mobilizing savings and allocating resources efficiently. Capital markets can also promote financial institutions’ development and increase credit access for individuals and businesses. Technology has also played an essential role in promoting financial development. Beck et al.

assert that financial technology (fintech) can potentially improve financial inclusion and access to financial services, particularly in low-income and rural areas. Fintech can also help to reduce transaction costs and increase the efficiency of financial transactions. Education and financial literacy are also important factors that contribute to financial development.

According to Lusardi and Mitchell

| [62] | Lusardi, A., & Mitchell, O. S. (2014). The Economic Importance of Financial Literacy: Theory and Evidence. Journal of Economic Literature, 52(1), 5-44. https://doi.org/10.1257/jel.52.1.5 |

[62]

, financial literacy can improve financial decision-making and increase access to financial services. In addition, education can also help individuals understand the importance of financial planning and savings, leading to greater financial stability and security. Political stability and institutional quality are also critical factors contributing to financial development. Keefer and Knack

pointed out that countries with stable political environments and strong institutions are more likely to develop effective financial systems. Stable political environments and strong institutions can promote investor confidence, increasing investment and economic growth.

Maintaining sustainable levels of public debt is, thus, crucial for the long-term economic stability of a country. As indicated previously, public debt, which is the amount of money a government owes to its creditors, can finance government spending, infrastructure projects, and other public investments. However, when public debt levels become too high, it can lead to several economic problems, including higher interest rates, inflation, and reduced economic growth.

Thus, there are several reasons why countries need to maintain sustainable levels of public debt. Firstly, high levels of public debt can lead to higher interest rates, which can sequentially lead to reduced private-sector investment and lower economic growth. According to Reinhart and Rogoff

, when a country’s debt-to-GDP ratio exceeds 90%, economic growth slows by an average of 1% per year. Furthermore, high public debt levels can lead to inflation, which can be particularly problematic for developing countries. Inflation can erode the purchasing power of consumers, leading to higher costs of living and reduced economic growth

| [55] | Ratiyah, R., Suharno, S., & Arintoko, A. (2023). Economic Dynamics: The Interconnection of Trade Balance, Exchange Rate, Inflation, And Imports In The Context Of Empirical Data. In Proceeding of Midyear International Conference (Vol. 2). https://core.ac.uk/download/587919235.pdf |

[55]

. Ahmed et al.

| [64] | Ahmed, S., Ahmed, W., & Zaman, N. (2021). Public debt and inflation in developing countries. Journal of Economics and Finance, 45(1), 103-115. |

[64]

asserted that high public debt levels are associated with higher inflation rates in developing countries. They discovered that every 10-percentage point increase in the public debt-to-GDP ratio is associated with a 0.4 percentage point increase in inflation in developing countries.

Furthermore, high levels of public debt can also lead to increased fiscal risks, particularly in the event of a sudden economic shock. IMF

noted that the COVID-19 pandemic has increased fiscal risks for several countries, principally those with high public debt levels. The study underscored the importance of debt sustainability analyses and the need for countries to implement sound fiscal policies to mitigate these risks. Also, high levels of public debt can limit the ability of governments to respond to economic crises. The World Bank

| [66] | World Bank. (2021). Fiscal Policy and Debt: Building Resilience in the Time of COVID-19. Washington, DC: World Bank. |

[66]

specified that countries with high levels of public debt might face more severe economic consequences in the event of a future crisis, including a natural disaster or recession and emphasized the need for countries to maintain fiscal buffers and reduce debt levels to enhance their resilience to future shocks.

Hence, when a country experiences an economic downturn, the government may need to implement expansionary policies such as fiscal stimulus to boost economic activity. However, if public debt levels are already high, the government may be unable to borrow more money to fund these policies

| [67] | Jha, R. (2023). Macroeconomic policies in the current global context. In Macroeconomics for Development (pp. 142-155). Edward Elgar Publishing https://doi.org/10.4337/9781788977869.00013 |

| [68] | Cecchetti, S. G., Mohanty, M. S., & Zampolli, F. (2011). The real effects of debt. BIS Working Paper No. 352. |

| [69] | Bernanke, B. S. (1993). Credit in the Macroeconomy. Quarterly Review-Federal Reserve Bank of New York, 18, 50-50. http://fraser.stlouisfed.org/ |

[67-69].

This can make it more difficult for governments to support households and businesses during economic distress. One instance of this can be seen in the impact of the COVID-19 pandemic on public debt levels. The pandemic led to a global economic downturn, with numerous countries experiencing significant declines in economic activity.

Despite the need for increased government spending to support households and businesses during the pandemic, some experts have raised concerns about the long-term implications of high public debt levels. IMF

| [66] | World Bank. (2021). Fiscal Policy and Debt: Building Resilience in the Time of COVID-19. Washington, DC: World Bank. |

[66]

emphasized the risks associated with high public debt levels, including increased vulnerability to future economic shocks and reduced fiscal space for future policy responses. The study argued that countries should focus on implementing fiscal policies that prioritize investment in areas supporting long-term growth and development, such as education, healthcare, and infrastructure, while also managing debt sustainably.

Overall, while increased government spending can be necessary to support households and businesses during economic distress, high levels of public debt can limit the ability of governments to respond to future crises and create long-term economic risks. As such, countries need to adopt responsible fiscal policies that balance the need for government support with long-term sustainability considerations. The above underscores the importance of maintaining sustainable levels of public debt. High public debt levels can lead to various economic problems, including inflation, increased fiscal risks, and reduced government flexibility in responding to future economic crises. By adopting responsible fiscal policies and managing debt effectively, countries can ensure that public debt levels remain sustainable and conducive to long-term economic growth.

Thus, as indicated earlier, since 2000, there has been a recorded increase in the stock of public debt and the current ‘C’ rating by Fitch in December 2022 and ‘Ca’ by Moody’s in November 2022 compelled the government to approach the International Monetary Fund (IMF) for an economic support package which has severe implications for the economy. In this regard, a thorough empirical assessment of the economic development in the face of rising public debt in Ghana will afford a firm footing for policy development geared toward an effective debt management strategy that contributes to the sustainable economic progress of Ghana.

3. Results

This study examined the intricate relationship between financial development and public debt within the context of Ghana. Understanding these relationships is critical for policy formulation and economic stabilization, given the dynamic economic environment and the government’s fiscal engagements.

The study began with a qualitative assessment where participants were requested to rate, on a scale of 1 to 10, the current state of financial development and the level of public debt in Ghana. This provided a subjective gauge of the perceived efficacy of existing financial systems and the public debt burden as perceived by stakeholders. Such assessments help identify underlying sentiments and concerns regarding the country’s financial health and debt management strategies.

A consensus emerged from the bank officials’ responses regarding Ghana’s current financial development and public debt. When reacting to financial development, many of the respondents expressed concern, with one noting,

“Our financial development is at a moderate level; I would rate it a 5. The main challenges are the high interest rates and low access to credit facilities, especially in the rural areas.”

Another respondent echoed this sentiment:

“On a scale of 1 to 10, I would rate our financial development at a 4. We have made some strides, especially in the digital finance sector, but there is still a long way to go.”

Public debt was also a prevalent issue in the responses. One bank official lamented,

“I am gravely concerned about our level of public debt, and I would give it a rating of 3. It’s quite high and could potentially impact our financial stability and future development.”

Another added,

“Effective public debt management is critical to prevent a crisis, and I would rate our public debt level at 5.”

The responses shed light on two main issues: the moderately progressing state of financial development in Ghana, marked by high interest rates and low accessibility to credit, and the rising level of public debt, which is seen as a significant risk to the country’s financial stability and future development prospects. These insights underline the need for policy interventions to enhance financial development and prudent public debt management.

Participants were then queried about the factors they believe are most critical in promoting financial development while managing sustainable levels of public debt. These factors include fiscal and monetary policies, the regulatory environment, the investment climate, infrastructure development, and consumer education. Ranking these factors in order of importance will illuminate the perceived hierarchies of influence and the interdependencies among these elements. This aspect of the study aimed to uncover the multi-dimensional factors that stakeholders believe should be prioritized to foster a robust financial sector amidst manageable debt levels. Bank officials offered a variety of perspectives. One respondent shared,

“To me, fiscal and monetary policies are paramount. These policies directly influence the level of public debt and also the environment within which our financial institutions operate. They would be my number one.”

Another bank official, however, saw the regulatory environment as more critical. They mentioned,

“An enabling regulatory environment can foster more innovation and competition in the financial sector. This is my top pick.”

Some bank officials also considered the investment climate to be significant.

“For a thriving financial sector, we need a conducive investment climate. This should be our primary focus if we want to attract domestic and foreign investment,”

one respondent noted.

Infrastructure development was another factor that received attention. A bank official opined,

“Infrastructure is the backbone of any economy; financial development is challenging without it. Hence, I rank it as a significant factor.”

Consumer education also received notable mentions. One bank official highlighted its importance, stating,

“Consumer education, though often overlooked, is vital. A well-informed consumer base can help develop a more robust financial sector, which deserves more attention.”

It could be observed that there is a consensus among the respondents that fiscal and monetary policies, the regulatory environment, the investment climate, infrastructure development, and consumer education all play a crucial role in promoting financial development and maintaining sustainable levels of public debt. However, the order of importance seems to vary according to individual perspectives.

Exploring how public debt influences the behaviour of banks and financial intermediaries through firsthand experiences of the participants provides deep insights into the practical implications of high debt levels. This section sought to capture the operational adjustments, risk management strategies, and financial decisions influenced by the nation’s debt dynamics. Several key points emerged when analyzing the hypothetical responses of the bank officials regarding the impact of public debt on the behaviour of banks and financial intermediaries. One respondent noted,

“As public debt increases, banks are more cautious and seem to tighten their credit standards in fear of increased default risk.”

Another bank official echoed this sentiment:

“High public debt levels create a sense of economic instability, and I’ve noticed that banks respond to this by reducing their risk exposure. This often means less lending to the private sector, particularly small and medium enterprises.”

However, another perspective highlighted that banks and financial intermediaries might see increased public debt as an investment opportunity. One bank official stated,

“Higher public debt can sometimes lead banks to invest in government securities, which are deemed safe. This ‘crowding out’ effect may reduce credit availability for the private sector.”

One respondent also underscored the importance of managing public debt, saying:

“It is not just about the level of public debt but how it’s managed. Banks and financial intermediaries watch closely for signs of fiscal discipline. A rising public debt combined with poor fiscal management can scare off banks from extending credit.”

The bank officials’ position highlights that high public debt levels can lead to a more conservative approach by banks and financial intermediaries, affecting their lending behaviour. However, this behaviour is also heavily influenced by the perceived management and sustainability of the public debt.

The study culminates with a solicitation of policy recommendations from participants. These recommendations aim to promote financial development while ensuring that public debt remains sustainable. Discussions include strategies for balancing financial growth with debt, the adoption of international best practices, the role of the central bank in maintaining financial stability, and policies that could enhance financial inclusion. This part of the qualitative analysis is particularly valuable as it harnesses expert opinions and practical suggestions that could inform effective policymaking. Several key points were noted when the respondents were asked about policy recommendations. One respondent suggested,

“The government could focus on reducing public expenditure and prioritizing spending on key sectors that would lead to financial development. This includes investing in education, infrastructure, and healthcare.”

Another added,

“A regulatory environment encouraging competition and innovation in the financial sector would also contribute significantly to financial development.”

More so, striking a balance was considered vital. A respondent noted,

“Striking a balance requires a multifaceted approach that includes prudent fiscal management, fostering a conducive business environment for private sector growth, and promoting a robust and inclusive financial sector.”

Also, the necessity of fiscal discipline was a common theme. One bank official said,

“Maintaining fiscal discipline is key, and the government should ensure that public expenditure is efficient, effective and aligns with the country’s long-term development goals.”

Another proposed that:

“The government could also look at strategies to increase revenue, such as improving tax collection, to reduce reliance on debt.”

Lastly, the central bank’s role in financial stability was highlighted. A respondent suggested,

“The central bank should proactively manage public debt by setting prudent monetary policies and promoting macroeconomic stability.”

Another bank official noted that:

“The central bank should also work in tandem with the government to align monetary and fiscal policies to ensure financial stability and sustainable debt management.”

In summary, the respondents strongly recommended fiscal discipline, improved government expenditure management, the creation of a conducive business environment, and the proactive role of the central bank in managing public debt while promoting financial stability.