The fuel oil is a basic input to production, so an increase in oil price leads to a rise in production costs that induces firms to lower output. In parallel, oil prices change also effects, indirectly, the consumption, through its positive relation with disposable income. However, despite the relevance of the variation in fuel prices in economy, there are no recent study conducted to analyse the impact of changes in fuel prices on GDP and CPI in Mozambique. This study aims to contribute to filling the information gap by providing the quantification of the impact of fuel prices on GDP and CPI. So, the study aim to determine the impact of changes in FUEL prices on Inflation (Consumer Price Index – CPI) and Economic Growth (Gross Domestic Product – GDP), using quarter data from 2007 to 2020. Descriptive statistics, Unit Root Test, Johansen Cointegration Test and Error Correction Model, Granger Causality Econometric Models, Impulse and Response Function and Variance Decomposition Analysis are used. The results indicate that in Mozambique there are a cointegrating long-run relationship between FUEL prices and CPI and GDP, which suggest that the impact of FUEL prices shocks to CPI and GDP in short-run and long-run path. Also, the results show that changes in GDP and FUEL prices lead to an increase in CPI by 3.0% and 1.3%, respectively, coeteris paribus. The previous quarter’s errors (or deviation from long-run equilibrium) are corrected for with the current quarter at a convergence speed of 3.5% to GDP, and 4.8% to CPI. Granger causality tests also indicate causality between CPI and GDP, and the changes in GDP causes changes in other variables.

| Published in | International Journal of Economics, Finance and Management Sciences (Volume 12, Issue 3) |

| DOI | 10.11648/j.ijefm.20241203.12 |

| Page(s) | 142-160 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2024. Published by Science Publishing Group |

FUEL, Consumer Price Index, Gross Domestic Product, Vector Autoregressive, Vector Error Correction Model

Division Code | Description | Base: Dez.98 | Base: Dez.2004 | Base: Dez.2010 | Base: 2016=100 |

|---|---|---|---|---|---|

01 | Food and non-alcoholic beverages | 62,4 | 55,46 | 44,48 | 33,92 |

02 | Alcoholic beverages, tobacco and narcotics | 1,06 | 2,21 | 1,32 | 1,21 |

03 | Clothing and footwear | 4,62 | 4,65 | 8,45 | 7,4 |

04 | Housing, water, electricity, gas and other fuels | 12,17 | 12,62 | 12,9 | 7,36 |

05 | Furnishings, household equipment and routine household maintenance | 4,79 | 5,3 | 6,37 | 7,59 |

06 | Health | 2,46 | 2,94 | 1,45 | 0,88 |

07 | Transport | 2,83 | 7,92 | 11,67 | 17,06 |

08 | Information and communication | 1,8 | 1,72 | 3,37 | 6,36 |

09 | Recreation, sport and culture | 2,12 | 2,63 | 3,52 | 1,57 |

10 | Education services | 0,63 | 1,26 | 1,71 | 2,38 |

11 | Restaurants and accommodation services | 0,34 | 1,97 | 1,34 | 10,7 |

12 | Other Goods and Services | 4,78 | 1,32 | 3,42 | 3,57 |

Total | 100 | 100 | 100 | 100 | |

(2)

(2)  is a pure white noise error term and where

is a pure white noise error term and where  ,

,  , etc. The number of lagged difference terms to include is often determined empirically, the idea being to include enough terms so that the error term is serially uncorrelated. In ADF we still test whether δ = 0 and the ADF test follows the same asymptotic distribution as the DF statistic, so the same critical values can be used.

, etc. The number of lagged difference terms to include is often determined empirically, the idea being to include enough terms so that the error term is serially uncorrelated. In ADF we still test whether δ = 0 and the ADF test follows the same asymptotic distribution as the DF statistic, so the same critical values can be used.  (6)

(6) Variables | FUEL | CPI | GDP |

|---|---|---|---|

N | 59 | 59 | 59 |

Mean | 44,90271 | 234,66570 | 133906,20000 |

Median | 39,70849 | 241,39110 | 137675,90000 |

Skewness | 0,48004 | -0,35771 | -0,23343 |

Kurtosis | 1,90777 | 1,76801 | 1,58354 |

Min | 25,67753 | 48,20374 | 83998,67000 |

Max | 67,14500 | 401,80000 | 171608,60000 |

Std.dev | 12,76602 | 122,84220 | 29207,79000 |

Augmented Dickey-Fuller (ADF) - Unit Root Tests

Variables | Lags | Level: I(0) | First difference: I(1) | Order of integration result | |

|---|---|---|---|---|---|

t - Stat P-value | Conclusion at 5% | t - Stat P-value Conclusion at 5% | |||

LnCPI | 0 | -1,593 0.7953 | No Stationary | -7,5110 0,000 Stationary | I (1) |

LnGDP | 1 | 0,181 0,9957 | No Stationary | -8,8780 0,000 Stationary | I (1) |

LnFuel | 0 | -3,049 0.119 | No Stationary | -4,4340 0,0019 Stationary | I (1) |

Lag | Sample: 2008q1 thru 2021q3 | Number of obs = 55 | ||||||

|---|---|---|---|---|---|---|---|---|

LL | LR | df | P | FPE | AIC | HQIC | SBIC | |

GDP | ||||||||

0 | 159,681 | 0,000164 | -5,87709 | -5,86289 | -5,84026* | |||

1 | 159,682 | 0,00032 | 1 | 0,986 | 0,00017 | -5,84006 | -5,81165 | -5,76639 |

2 | 159,848 | 0,33304 | 1 | 0,564 | 0,000176 | -5,80919 | -5,76657 | -5,69869 |

3 | 164,099 | 8,5024* | 1 | 0,004 | ,000156* | -5,9296* | -5,87278* | -5,78227 |

4 | 164,755 | 1,3121 | 1 | 0,252 | 0,000158 | -5,91687 | -5,84584 | -5,7327 |

ICP | ||||||||

0 | 24,1694 | ,024823* | -,858126* | -,843921* | -,821293* | |||

1 | 24,1701 | 0,00145 | 1 | 0,97 | 0,025759 | -0,82112 | -0,79271 | -0,74745 |

2 | 24,1947 | 0,04915 | 1 | 0,825 | 0,026709 | -0,78499 | -0,74237 | -0,67449 |

3 | 24,1949 | 0,00046 | 1 | 0,983 | 0,027721 | -0,74796 | -0,69114 | -0,60063 |

4 | 24,2152 | 0,04056 | 1 | 0,84 | 0,028753 | -0,71167 | -0,64065 | -0,52751 |

FUEL | ||||||||

0 | 89,8605 | 0,002179 | -3,29113 | -3,27692 | -3,25429 | |||

1 | 96,4294 | 13,138* | 1 | 0 | ,001773* | -3,49739* | -3,46898* | -3,42372* |

2 | 97,3715 | 1,8842 | 1 | 0,17 | 0,001777 | -3,49524 | -3,45263 | -3,38474 |

3 | 97,6532 | 0,56339 | 1 | 0,453 | 0,001825 | -3,46864 | -3,41182 | -3,32131 |

4 | 98,547 | 1,7876 | 1 | 0,181 | 0,001833 | -3,4647 | -3,39368 | -3,28054 |

Johansen tests for cointegration | |||||

|---|---|---|---|---|---|

Trend: Constant | Number of observations = 57 | ||||

Sample: 2007q3 thru 2021q3 | Number of lags =2 | ||||

H0: No Cointegration | |||||

Maximum | Trace | ||||

Rank | Params | LL | Eigenvalue | Trace test - Critical value (5%) | Critical Value (5%) |

0 | 12 | 315,53716 | 46,1952 | 29,68 | |

1 | 17 | 332,2763 | 0,4442 | 12,7169 | 15,41 * |

2 | 20 | 336,26006 | 0,13045 | 4,7494 | 3,76 |

3 | 21 | 338,63477 | 0,07995 | ||

Maximum | Params | LL | Eigenvalue | Maximum- Eigenvalue | Critical Value (5%) |

|---|---|---|---|---|---|

Rank | |||||

0 | 12 | 315,53716 | 33,4783 | 20,97 | |

1 | 17 | 332,2763 | 0,4442 | 7,9675 | 14,07* |

2 | 20 | 336,26006 | 0,13045 | 4,7494 | 3,76 |

3 | 21 | 338,63477 | 0,07995 |

Long Run Equation

D (LNCPI) | D (LNFUEL) | D (LNGDP) | ||||

|---|---|---|---|---|---|---|

Coef | P-value | Coef | P-value | Coef | P-value | |

Constant | 35,52577 | -26,42498 | -11,66672 | |||

CPI | 1 | -0,74383 | 0,00000 | -0,32840 | 0,00000 | |

FUEL | -1,34440 | 0,00000 | 1 | 0,44150 | 0,00000 | |

GDP | -3,04505 | 0,00000 | 2,26499 | 0,00000 | 1 | |

ECT | -0.04769 | 0.052 | -0.02166 | 0.0216 | -0.03538 | 0.010 |

Vector Correction Model | ||||||

|---|---|---|---|---|---|---|

ERROR CORRECTION | D (LNCPI) | D (LNFUEL) | D (LNGDP) | |||

Coef | P-value | Coef | P-value | Coef | P-value | |

CoinEq,1 (ECT) | -0,04769 | 0,0518*** | -0,02166 | 0,0206** | -0,03538 | 0,01* |

D(LNCPI-1) | -0,04871 | 0,754 | 0,03396 | 0,470 | -0,05513 | 0,00* |

D(LnFUEL-1) | -0,12061 | 0,775 | 0,41819 | 0,775 | 0,03257 | 0,185 |

D(LNGDP-1) | 1,91465 | 0,336 | -0,46852 | 0,436 | 0,16252 | 0,161 |

CONSTANT | 0,00853 | 0,804 | 0,01539 | 0,138 | 0,01369 | 0,00* |

Pairwise Granger Causality Results | |||

|---|---|---|---|

Null hypothesis | Chi-Square | p-value | Conclusion |

GDP dos not Granger cause CPI | 25,054 | 0,0000 | Reject H0 |

GDP dos not Granger cause FUEL | 0,70896 | 0,4000 | Don’t Reject H0 |

GDP dos not Granger cause All | 32,159 | 0,0000 | Reject H0 |

CPI dos not Granger cause GDP | 0,53597 | 0,4640 | Don’t Reject H0 |

CPI dos not Granger cause FUEL | 0,03792 | 0,8460 | Don’t Reject H0 |

CPI dos not Granger cause All | 0,55498 | 0,7580 | Don’t Reject H0 |

FUEL dos not Granger cause GDP | 0,24453 | 0,6210 | Don’t Reject H0 |

FUEL dos not Granger cause CPI | 0,66309 | 0,4150 | Don’t Reject H0 |

FUEL dos not Granger cause All | 0,55498 | 0,7110 | Don’t Reject H0 |

Impulse | lnGDP | lnGDP | lnGDP | lnCPI | lnCPI | lnCPI | lnFUEL | lnFUEL | lnFUEL |

|---|---|---|---|---|---|---|---|---|---|

Response | lnGDP | lnCPI | lnFUEL | lnGDP | lnCPI | lnFUEL | lnGDP | lnCPI | lnFUEL |

1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | |

Step | fevd | fevd | fevd | fevd | fevd | fevd | Fevd | fevd | fevd |

0 | 0,0000 | 0,0000 | 0,0000 | 0,0000 | 0,0000 | 0,0000 | 0,0000 | 0,0000 | 0,0000 |

1 | 1,0000 | 0,2995 | 0,0006 | 0,0000 | 0,6866 | 0,0000 | 0,0000 | 0,0139 | 0,9994 |

2 | 0,6655 | 0,2876 | 0,0009 | 0,3248 | 0,6606 | 0,0047 | 0,0097 | 0,0517 | 0,9944 |

3 | 0,6175 | 0,2519 | 0,0078 | 0,3010 | 0,5762 | 0,0104 | 0,0815 | 0,1719 | 0,9818 |

4 | 0,6001 | 0,2466 | 0,0091 | 0,2984 | 0,5641 | 0,0105 | 0,1015 | 0,1893 | 0,9804 |

5 | 0,5931 | 0,2467 | 0,0092 | 0,2969 | 0,5634 | 0,0105 | 0,1100 | 0,1899 | 0,9803 |

6 | 0,5929 | 0,2469 | 0,0092 | 0,2971 | 0,5633 | 0,0105 | 0,1099 | 0,1899 | 0,9802 |

7 | 0,5922 | 0,2468 | 0,0093 | 0,2968 | 0,5630 | 0,0106 | 0,1109 | 0,1902 | 0,9802 |

8 | 0,5922 | 0,2468 | 0,0093 | 0,2968 | 0,5629 | 0,0106 | 0,1110 | 0,1903 | 0,9801 |

Test Null Hypothesis Chi-square Probability Decision | ||||

|---|---|---|---|---|

LM Test | No serial correlation | 31.30 | 0.000 | With p-value less than 5%, reject H0. Therefore, the results show that there is serial correlation in the model |

White Test | No heteroscedasticity | 21.56 | 0.000 | With p-value less than 5%, reject H0. Therefore, the results show that there is a heteroscedasticity in the model |

Jarque-Bera | Residual are normal distributed | 78.7453 | 0.000 | With p-value less than 5%, reject H0. Therefore, the results show that the data is not normally distributed |

CPI | Consumer Price Index |

ECT | Error Correction Term |

EU | European Union |

ECM | Error Correction Mechanism |

GDP | Gross Domestic Product |

IMF | International Monetary Fund |

IWGPS | Inter-secretariat Working Group on Price Statistics |

ISWGNA | Inter-Secretariat Working Group on National Accounts |

OECD | Organization for Economic Co-operation and Development |

SNA | System of National Accounts |

UN | United Nations |

UNSD | The United Nations Statistics Division |

VAR | Vector Autoregressive |

VDC | Decomposition of Variance |

VECM | Vector Error Correction Mechanism |

WB | World Bank |

| [1] | Akinleye, S. O., & Ekpo, S. (2013). Oil price shocks and macroeconomic performance in Nigeria. Economía Mexicana Nueva Época, volumen Cierre de época, número II de 2013, pp 565-624. |

| [2] | Adeleye, N., Ogundipe, A. A., Ogundipe, O., Ogunrinola, I., & Adediran, O. (2019). Internal and external drivers of inflation in Nigeria. Banks Bank Syst, 14(4), 206-218. Pdf (semanticscholar.org). |

| [3] |

Arndt, C., Benfica, R., Maximiano, N., Nucifora, A. M., & Thurlow, J. T. (2008). Higher fuel and food prices: impacts and responses for Mozambique. Agricultural Economics, 39, 497-511.

https://onlinelibrary.wiley.com/doi/full/10.1111/j.1574-0862.2008.00355.x |

| [4] | Arndt C, Matsinhe L, Mulder P, Paulo E, e Van Dunem J. (2005) “O impacto do aumento do preço do petróleo na Economia Moçambicana”. Ministerio da Planificacao e Desenolvimento, DNEAP Discussion paper, p. 19. 28. |

| [5] | Arinze, P. E. (2011). The impact of oil price on the Nigerian economy. Journal of Research in National Development, 9(1), 211-215. |

| [6] |

Banco de Mocambique (2016). Relatorio Anual 2016. Maputo. Mocambique. Disponivel em:

https://www.bancomoc.mz/fm_pgtab1.aspx?id=106 (Acessed in 28 July 2022). |

| [7] | Bellemare, M. F. (2015). Rising food prices, food price volatility, and social unrest. American Journal of agricultural economics, 97(1), 1-21. |

| [8] | Bhattacharya, K., & Bhattacharya, I. (2001). Impact of increase in oil prices on inflation and output in India. Economic and Political Weekly, 36(51), 4735–4741. |

| [9] | Bobai, F. D. (2012). An analysis of the relationship between petroleum prices and inflation in Nigeria. International Journal of Business and Commerce, 1(12), 01–07. |

| [10] |

Brito, L. D. (2017). Agora eles têm medo de nós! Uma colectânea de textos sobre as revoltas populares em Moçambique (2008–2012). Maputo: IESE.

https://www.iese.ac.mz/wpcontent/uploads/2018/02/IESE-Food-Riot.pdf |

| [11] | Brinkman, C. S. Hendrix, Food insecurity and conflict: Applying the WDR framework, World Development Report 2011 (August 2, 2010). |

| [12] |

Brown, S. P., & Yücel, M. K. (2002). Energy prices and aggregate economic activity: an interpretative survey. The Quarterly Review of Economics and Finance, 42(2), 193-208.

https://www.sciencedirect.com/science/article/abs/pii/S1062976902001382 |

| [13] |

Chang, Y., & Wong, J. F. (2003). Oil price fluctuations and Singapore economy. Energy policy, 31(11), 1151-1165.

https://www.sciencedirect.com/science/article/abs/pii/S0301421502002124 |

| [14] |

Chamalwa, H. A., & Bakari, H. R. (2016). A Vector Autoregressive (VAR) Cointegration and Vector Error Correction Model (VECM) approach for financial deepening indicators and economic growth in Nigeria. American Journal of Mathematical Analysis, 4(1), 1-6.

https://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.1088.6462&rep=rep1&type=pdf |

| [15] | Commission of the European Communities, International Monetary Fund, Organisation for Economic Cooperation and Development, United Nations and World Bank, System of National Accounts 2008. Brussels/Luxembourg, Washington, D. C., Paris, New York, 2008. United Nations Publication, Sales No. E. 94.XVII. 4. |

| [16] | Cunado, J., & De Gracia, F. P. (2005). Oil prices, economic activity and inflation: evidence for some Asian countries. The Quarterly Review of Economics and Finance, 45(1), 65-83. |

| [17] |

Du, L., Yanan, H., Chu, W & Wei, C. (2010). The relationship between oil price shocks and China’s macro-economy: An empirical analysis. Energy policy, 38(8), 4142-4151.

https://www.sciencedirect.com/science/article/abs/pii/S0301421510002053 |

| [18] | Gbenga, O., & Omo-Ojugo, S. O. (2022). The Effect of Petroleum Product Prices Adjustment on Inflation Rate in Nigeria (1980-2021). Academic Journal of Digital Economics and Stability, 15, 164175. |

| [19] | Gujarati DN (2003). Basic Econometrics. 4th Edition, McGraw-Hill, New York. |

| [20] | Hamilton, J. D. (1983). Oil and the Macroeconomy since World War II, Journal of Political Economy, 91(3), 228-248. |

| [21] | Inter-Secretariat Working Group on National Accounts (United Nations, European Commission, International Monetary Fund, Organisation for Economic Cooperation and Development and World Bank) – ISWGNA (2009), System of National Accounts 2008, Series F, No. 2, Rev. 5, United Nations, New York. |

| [22] | Inter-secretariat Working Group on Price Statistics (International Labour Organization, International Monetary Fund, Organisation for Economic Co-operation and Development, European Union, United Nations and The World Bank) – IWGPS, (2020). Consumer price index manual: concepts and methods. International Monetary Fund, Publication, Washington, U.S.A. |

| [23] | INE - Instituto Nacional de Estatística (2022). Contas Nacionais. Maputo- Moçambique. |

| [24] |

Jiménez-Rodríguez, R., & Sánchez, M. (2005). Oil price shocks and real GDP growth: empirical evidence for some OECD countries. Applied economics, 37(2), 201-228.

https://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.357.5343&rep=rep1&type=pdf |

| [25] |

Johansen, S., & Juselius, K. (1990). Maximum likelihood estimation and inference on cointegration— with appucations to the demand for money. Oxford Bulletin of Economics and statistics, 52(2), 169210.

https://digilander.libero.it/rocco.mosconi/JohansenJuselius1990.pdf |

| [26] | Kinyanjui, A. K. (2018). Effects of crude oil prices on gross domestic product growth and selected macroeconomic variables in kenya (doctoral dissertation, kenyatta university). |

| [27] |

Korhonen, I., & Ledyaeva, S. (2010). Trade linkages and macroeconomic effects of the price of oil. Energy Economics, 32(4), 848-856.

https://www.econstor.eu/bitstream/10419/212629/1/bofit-dp2008-016.pdf |

| [28] | Lepenies, P. (2016). The power of a single number: a political history of GDP. Columbia University Press. |

| [29] | Le Blanc, M. & Chinn, M. (2004). Do high oil price presage inflation? The evidence from G-5 countries. Santa Cruz Center for International Economics (Working Paper, WP1021). |

| [30] | Lagi, M., Bertrand, K. Z., & Bar-Yam, Y. (2011). The food crises and political instability in North Africa and the Middle East. arXiv preprint arXiv: 1108.2455. |

| [31] | Lescaroux, F., & Mignon, V. (2008). On the influence of oil prices on economic activity and other macroeconomic and financial variables. OPEC Energy Review, 32(4), 343-380. |

| [32] | Malik, A. (2016). The impact of oil price changes on inflation in Pakistan. International journal of energy economics and policy, 6(4), 727-737. |

| [33] | Masiya, M. (2010). The Lisman and Sandee Method of Interpolation in Stata. Available at SSRN 2504523. |

| [34] | Meyer, D. F. (2018). The impact of changes in fuel prices on inflation and economic growth in South Africa. In Proceedings of the 11th International RAIS Conference on Social Sciences (pp. 65-73). Scientia Moralitas Research Institute. http://rais.education/wp-content/uploads/2018/11/010DM.pdf |

| [35] |

Nhamire, B., Mapisse, I., & Fael, B. (2019). Corrupção e más práticas no sectores dos combustíveis e de energia eléctrica: seus efeitos para o orçamento das famílias moçambicanos. CIP, Centro de Integridade Pública.

https://cipmoz.org/wp-content/uploads/2019/02/CORRUPC%CC%A7A%CC%83O-E-MA%CC%81SPRA%CC%81TICAS-1.pdf |

| [36] | Ocheni, S. I. (2015). Impact of fuel price increaseon the Nigerian economy. Mediterranean Journal of Social Sciences, 6(1 S1), 560-560. Impact of Fuel Price Increaseon the Nigerian Economy | Mediterranean Journal of Social Sciences (richtmann.org). |

| [37] | Peker, O., & Mercan, M. (2011). The inflationary effect of price increases in oil products in Turkey. Ega Academic Review, 11(4), 553–562. |

| [38] | Przekota, G.; Szczepa ´nska-Przekota, A. Pro-Inflationary Impact of the Oil Market—A Study for Poland. Energies 2022, 15, 3045. |

| [39] |

Peersman, G., & Van Robays, I. (2012). Cross-country differences in the effects of oil shocks. Energy Economics, 34(5), 1532-1547.

https://www.econstor.eu/bitstream/10419/46278/1/644794933.pdf |

| [40] |

Sarmah, A., & Bal, D. P. (2021). Does Crude Oil Price Affect the Inflation Rate and Economic Growth in India? A New Insight Based on Structural VAR Framework. The Indian Economic Journal, 69(1), 123-139.

https://journals.sagepub.com/doi/pdf/10.1177/0019466221998838 |

| [41] | Sek, S. K., Teo, X. Q., & Wong, Y. N. (2015). A comparative study on the effects of oil price changes on inflation. “4th World Conference on Business, Economics and Management, WCBEM”. |

| [42] | Tang, W., Wu, L., & Zhang, Z. (2010). Oil price shocks and their short-and long-term effects on the Chinese economy. Energy Economics, 32, S3-S14. |

APA Style

Macia, S., Macuacua, J., Vilanculos, A., Mahaluça, F. (2024). Impact of Changes in Fuel Prices on Inflation and Economic Growth in Mozambique. International Journal of Economics, Finance and Management Sciences, 12(3), 142-160. https://doi.org/10.11648/j.ijefm.20241203.12

ACS Style

Macia, S.; Macuacua, J.; Vilanculos, A.; Mahaluça, F. Impact of Changes in Fuel Prices on Inflation and Economic Growth in Mozambique. Int. J. Econ. Finance Manag. Sci. 2024, 12(3), 142-160. doi: 10.11648/j.ijefm.20241203.12

AMA Style

Macia S, Macuacua J, Vilanculos A, Mahaluça F. Impact of Changes in Fuel Prices on Inflation and Economic Growth in Mozambique. Int J Econ Finance Manag Sci. 2024;12(3):142-160. doi: 10.11648/j.ijefm.20241203.12

@article{10.11648/j.ijefm.20241203.12,

author = {Sandre Macia and Júlio Macuacua and Alfeu Vilanculos and Filipe Mahaluça},

title = {Impact of Changes in Fuel Prices on Inflation and Economic Growth in Mozambique

},

journal = {International Journal of Economics, Finance and Management Sciences},

volume = {12},

number = {3},

pages = {142-160},

doi = {10.11648/j.ijefm.20241203.12},

url = {https://doi.org/10.11648/j.ijefm.20241203.12},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ijefm.20241203.12},

abstract = {The fuel oil is a basic input to production, so an increase in oil price leads to a rise in production costs that induces firms to lower output. In parallel, oil prices change also effects, indirectly, the consumption, through its positive relation with disposable income. However, despite the relevance of the variation in fuel prices in economy, there are no recent study conducted to analyse the impact of changes in fuel prices on GDP and CPI in Mozambique. This study aims to contribute to filling the information gap by providing the quantification of the impact of fuel prices on GDP and CPI. So, the study aim to determine the impact of changes in FUEL prices on Inflation (Consumer Price Index – CPI) and Economic Growth (Gross Domestic Product – GDP), using quarter data from 2007 to 2020. Descriptive statistics, Unit Root Test, Johansen Cointegration Test and Error Correction Model, Granger Causality Econometric Models, Impulse and Response Function and Variance Decomposition Analysis are used. The results indicate that in Mozambique there are a cointegrating long-run relationship between FUEL prices and CPI and GDP, which suggest that the impact of FUEL prices shocks to CPI and GDP in short-run and long-run path. Also, the results show that changes in GDP and FUEL prices lead to an increase in CPI by 3.0% and 1.3%, respectively, coeteris paribus. The previous quarter’s errors (or deviation from long-run equilibrium) are corrected for with the current quarter at a convergence speed of 3.5% to GDP, and 4.8% to CPI. Granger causality tests also indicate causality between CPI and GDP, and the changes in GDP causes changes in other variables.

},

year = {2024}

}

TY - JOUR T1 - Impact of Changes in Fuel Prices on Inflation and Economic Growth in Mozambique AU - Sandre Macia AU - Júlio Macuacua AU - Alfeu Vilanculos AU - Filipe Mahaluça Y1 - 2024/05/30 PY - 2024 N1 - https://doi.org/10.11648/j.ijefm.20241203.12 DO - 10.11648/j.ijefm.20241203.12 T2 - International Journal of Economics, Finance and Management Sciences JF - International Journal of Economics, Finance and Management Sciences JO - International Journal of Economics, Finance and Management Sciences SP - 142 EP - 160 PB - Science Publishing Group SN - 2326-9561 UR - https://doi.org/10.11648/j.ijefm.20241203.12 AB - The fuel oil is a basic input to production, so an increase in oil price leads to a rise in production costs that induces firms to lower output. In parallel, oil prices change also effects, indirectly, the consumption, through its positive relation with disposable income. However, despite the relevance of the variation in fuel prices in economy, there are no recent study conducted to analyse the impact of changes in fuel prices on GDP and CPI in Mozambique. This study aims to contribute to filling the information gap by providing the quantification of the impact of fuel prices on GDP and CPI. So, the study aim to determine the impact of changes in FUEL prices on Inflation (Consumer Price Index – CPI) and Economic Growth (Gross Domestic Product – GDP), using quarter data from 2007 to 2020. Descriptive statistics, Unit Root Test, Johansen Cointegration Test and Error Correction Model, Granger Causality Econometric Models, Impulse and Response Function and Variance Decomposition Analysis are used. The results indicate that in Mozambique there are a cointegrating long-run relationship between FUEL prices and CPI and GDP, which suggest that the impact of FUEL prices shocks to CPI and GDP in short-run and long-run path. Also, the results show that changes in GDP and FUEL prices lead to an increase in CPI by 3.0% and 1.3%, respectively, coeteris paribus. The previous quarter’s errors (or deviation from long-run equilibrium) are corrected for with the current quarter at a convergence speed of 3.5% to GDP, and 4.8% to CPI. Granger causality tests also indicate causality between CPI and GDP, and the changes in GDP causes changes in other variables. VL - 12 IS - 3 ER -

The Centre of Excellence in Agri-Food Systems and Nutrition (CE-AFSN), Eduardo Mondlane University, Maputo, Mozambique; National Statistics Institute, Directorate of National Accounts and Global Indicators, Maputo, Mozambique; Higher Institute of Accounting and Auditing of Mozambique, Maputo, Mozambique

Higher Institute of Accounting and Auditing of Mozambique, Maputo, Mozambique

Higher Institute of Accounting and Auditing of Mozambique, Maputo, Mozambique; Faculty of Economics, Eduardo Mondlane University, Maputo, Mozambique

Higher Institute of Accounting and Auditing of Mozambique, Maputo, Mozambique; Department of Economics, University Saint Thomas Mozambique, Maputo, Mozambique

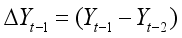

Figure 1. Structure of Gross Value Added by activity groups at current prices, 2010-2021.

Figure 2. Average quarter prices of GDP, CPI and FUEL prices (Jan2016 -July2022).

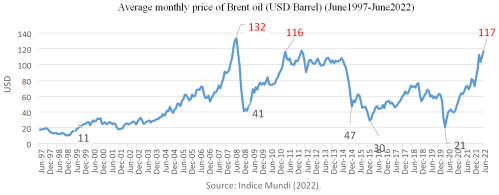

Figure 3. Average monthly price of Brent oil (USD/Barrel (June1997 -June2022).

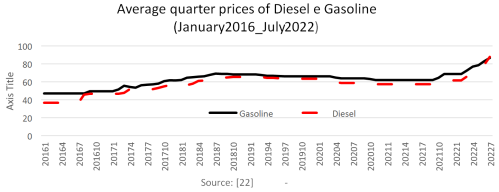

Figure 4. Average quarter prices of diesel e gasoline (MZN/Litre (Jan2016 -July2022).

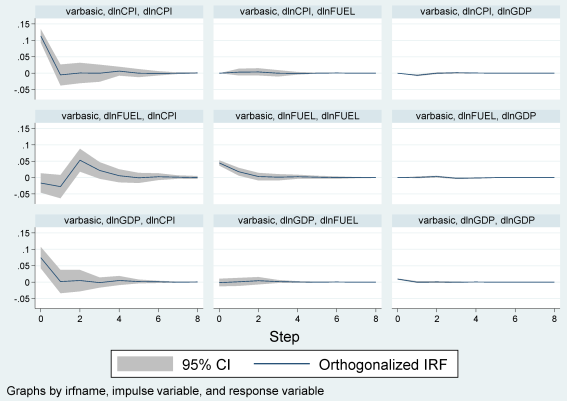

Figure 5. Impulse and Response.

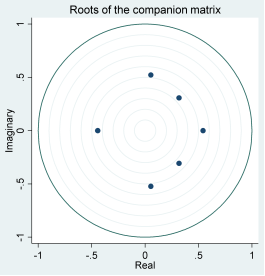

Figure 6. Root test estimates.

Information