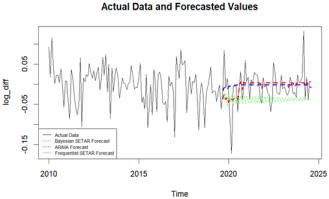

The analysis and interpretation of time series data is of great importance across different fields, including economics, finance, and engineering, among other fields. This kind of data, characterized by sequential observations over time, sometimes exhibits complex patterns and trends that some commonly used models, such as linear autoregressive (AR) and simple moving average (MA) models, cannot capture. This limitation calls for the development of more sophisticated and flexible models that can effectively capture the complexity of time series data. In this study, a more sophisticated model, the Self-Exciting Threshold Autoregressive (SETAR) model, is used to model the Nairobi Securities Exchange (NSE) 20 Share Index, incorporating a Bayesian parameter estimation approach. The objectives of this study are to analyze the properties of the NSE 20 Share Index data, to determine the estimates of SETAR model parameters using the Bayesian approach, to forecast the NSE 20 Share Index for the next 12 months using the fitted model, and to compare the forecasting performance of the Bayesian SETAR with the frequentist SETAR and ARIMA model. Markov Chain Monte Carlo (MCMC) techniques, that is, Gibbs sampling and the Metropolis-Hastings Algorithm, are used to estimate the model parameters. SETAR (2; 4, 4) model is fitted and used to forecast the NSE 20 Share Index. The study's findings generally reveal an upward trajectory in the NSE 20 Share Index starting September 2024. Even though a slight decline is predicted in November, an upward trend is predicted in the following months. On comparing the performance of the models, the Bayesian SETAR model performed better than the linear ARIMA model for both short and longer forecasting horizons. It also performed better than its counterpart model, which uses the frequentist approach for a longer forecasting horizon. These results show the applicability of SETAR modeling in capturing non-linear dynamics. The Bayesian approach incorporated for parameter estimation advanced the model even further by providing a flexible and robust way of parameter estimation and accommodating uncertainty.

| Published in | American Journal of Theoretical and Applied Statistics (Volume 13, Issue 6) |

| DOI | 10.11648/j.ajtas.20241306.13 |

| Page(s) | 203-212 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2024. Published by Science Publishing Group |

Nonlinear Time Series, Threshold Autoregressive Models, SETAR, Bayesian Inference, Markov Chain Monte Carlo (MCMC), NSE20 Index

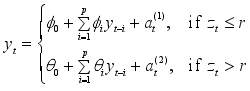

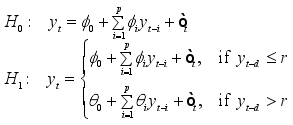

is observed at discrete time points t. TAR(p), a TAR model of order p and two regimes can be written as

is observed at discrete time points t. TAR(p), a TAR model of order p and two regimes can be written as  (1)

(1)  is the threshold variable, and

is the threshold variable, and  are independent Gaussian white noise processes with mean zero and variance

are independent Gaussian white noise processes with mean zero and variance  , with j = 1,2.

, with j = 1,2.  and

and  are real-valued parameters and r is the threshold.

are real-valued parameters and r is the threshold.  value is replaced with previous values of the time series

value is replaced with previous values of the time series  as below, the TAR model is then referred to as SETAR model.

as below, the TAR model is then referred to as SETAR model.  (2)

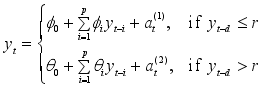

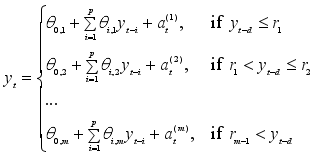

(2)  , that is,

, that is,  , where d represents the delay parameter.

, where d represents the delay parameter.  be a positive finite integer and

be a positive finite integer and  a real number sequence with

a real number sequence with  where

where  and

and  are regarded as real numbers. Then a time series

are regarded as real numbers. Then a time series  is a m-regime SETAR (p) model if it satisfies

is a m-regime SETAR (p) model if it satisfies  (3)

(3)  is the threshold variable and

is the threshold variable and  is the delay parameter.

is the delay parameter.  are collected of a time series

are collected of a time series  . Suppose that each data point,

. Suppose that each data point,  , is associated with a probability distribution which can be expressed as a function of a parameter or many parameters

, is associated with a probability distribution which can be expressed as a function of a parameter or many parameters  so that the relationship between

so that the relationship between  and

and  is described by a pdf

is described by a pdf  . When

. When  is considered as a function of

is considered as a function of  instead of

instead of  , it is referred to as the likelihood function. By applying Bayes' theorem, the posterior pdf

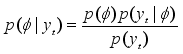

, it is referred to as the likelihood function. By applying Bayes' theorem, the posterior pdf  can be derived, that is, the posterior pdf of

can be derived, that is, the posterior pdf of  given

given  , by multiplying the likelihood with the prior density,

, by multiplying the likelihood with the prior density,  . That is,

. That is,  (4)

(4)

defines what is known as predictive density function. The prior distribution provides a means to include researcher's initial beliefs or assumptions regarding

defines what is known as predictive density function. The prior distribution provides a means to include researcher's initial beliefs or assumptions regarding  , and Bayes' theorem enables the revision and updating of these assumptions once the data is observed.

, and Bayes' theorem enables the revision and updating of these assumptions once the data is observed.  and

and  are taken as independent and normally distributed as

are taken as independent and normally distributed as  , while

, while  and

and  are taken as independent with inverse gamma distribution inverse gamma

are taken as independent with inverse gamma distribution inverse gamma  . The hyper-parameters d and r are assumed to be known. r is presumed to have a uniform distribution on

. The hyper-parameters d and r are assumed to be known. r is presumed to have a uniform distribution on  while d is presumed to take a discrete uniform distribution on 1,2,..., D.

while d is presumed to take a discrete uniform distribution on 1,2,..., D.  's,

's,  s, r, and d. Determining the posterior distribution is frequently achallenging task due to the need for complex numerical integration in high-dimensional spaces. Therefore, Gibbs Sampler and the Metropolis-Hastings algorithm will be used in this study to find the conditional posterior distributions of the unknown parameters.

s, r, and d. Determining the posterior distribution is frequently achallenging task due to the need for complex numerical integration in high-dimensional spaces. Therefore, Gibbs Sampler and the Metropolis-Hastings algorithm will be used in this study to find the conditional posterior distributions of the unknown parameters.  can be broken down into components

can be broken down into components  and the conditional densities

and the conditional densities  can be simulated for

can be simulated for  . Then, to sample from the joint density of

. Then, to sample from the joint density of  using Gibbs sampler, the following algorithm is followed:

using Gibbs sampler, the following algorithm is followed:  , generate

, generate  ,

,  ,

,  .

.  (5)

(5)  and

and  being functions of r.

being functions of r.  is made. Hence, a transition kernel

is made. Hence, a transition kernel  with

with  can be utilized to map

can be utilized to map  into

into  . The Metropolis algorithm will then work in the following manner;

. The Metropolis algorithm will then work in the following manner;  drawn from the prior

drawn from the prior  and set the indicator

and set the indicator  to 0.

to 0.  , generate a new point

, generate a new point  .

.  , update

, update  to

to  and remain at

and remain at  with a probability of

with a probability of  .

.  (6)

(6)  (hasunitroots)

(hasunitroots)  (nounitroots)

(nounitroots)  (serieshasaunitrootwithdrift)

(serieshasaunitrootwithdrift)  (seriesisstationarywithbreak(s))

(seriesisstationarywithbreak(s)) Working Orders | Test statistic | P-value |

|---|---|---|

1 | 1.246 | 0.2652 |

2 | 1.871 | 0.1345 |

3 | 1.671 | 0.1276 |

4 | 1.59 | 0.1085 |

5 | 1.634 | 0.06407 |

6 | 2.272 | 0.001457 |

7 | 2.453 | 0.000116 |

8 | 2.273 | 0.0001182 |

9 | 2.18 | 8.27e-05 |

10 | 2.273 | 1.068e-05 |

P-values | ||||

|---|---|---|---|---|

Embedding Dimension | ε (standard deviation) | |||

0.5 | 1.0 | 1.5 | 2.0 | |

2 | 2.2 e-16 | 2.2 e-16 | 2.2 e-16 | 2.2 e-16 |

3 | 2.2 e-16 | 2.2 e-16 | 2.2 e-16 | 2.2 e-16 |

.

.  are estimated using the Bayesian approach. The Gibbs sampler was executed for 1,000 iterations, and the initial 500 iterations were disregarded as the burn-in sample. The estimates of the parameters alongside their standard errors are as shown in the table below;

are estimated using the Bayesian approach. The Gibbs sampler was executed for 1,000 iterations, and the initial 500 iterations were disregarded as the burn-in sample. The estimates of the parameters alongside their standard errors are as shown in the table below; Parameter | Mean | Median | Standard Deviation |

|---|---|---|---|

| -0.0332 | -0.0327 | 0.0109 |

| -0.2871 | -0.2894 | 0.1590 |

| 0.0739 | 0.0677 | 0.1353 |

| -0.0866 | -0.0818 | 0.1369 |

| 0.3277 | 0.3282 | 0.1194 |

| 0.0023 | 0.0020 | 0.0042 |

| 0.1288 | 0.1301 | 0.0963 |

| 0.0532 | 0.0566 | 0.0584 |

| 0.1191 | 0.1162 | 0.0593 |

| 0.0616 | 0.0607 | 0.0668 |

| 0.0033 | 0.0032 | 0.0005 |

| 0.0024 | 0.0024 | 0.0002 |

r | -0.0218 | -0.0215 | 0.0037 |

d | 1 | 1 | 0.0000 |

and

and  . The estimated value of d is 1.

. The estimated value of d is 1. Predictions | |||

|---|---|---|---|

Month/Year | Mean | Lower | Upper |

Sep 2024 | 1683.5889 | 1661.17926 | 1703.74326 |

Oct 2024 | 1689.9987 | 1667.50375 | 1711.25625 |

Nov 2024 | 1665.6705 | 1613.37418 | 1688.30953 |

Dec 2024 | 1671.6777 | 1645.47278 | 1692.53558 |

Jan 2025 | 1677.5389 | 1654.05153 | 1697.62081 |

Feb 2025 | 1684.2624 | 1661.51153 | 1707.66638 |

Mar 2025 | 1693.7208 | 1664.00567 | 1738.85656 |

Apr 2025 | 1698.9795 | 1676.19736 | 1719.14616 |

May 2025 | 1704.7658 | 1680.7292 | 1723.79413 |

June 2025 | 1713.6537 | 1685.10479 | 1753.52448 |

Jul 2025 | 1718.9743 | 1697.45106 | 1739.20437 |

Aug 2025 | 1723.9665 | 1700.33918 | 1743.90657 |

Bayesian SETAR | Frequentist SETAR | ARIMA | |

|---|---|---|---|

RMSE | 0.05074525 | 0.04949407 | 0.05102666 |

Bayesian SETAR | Frequentist SETAR | ARIMA | |

|---|---|---|---|

RMSE | 0.03947424 | 0.05351723 | 0.04191522 |

SETAR | Self-Exciting Threshold Autoregressive |

NSE | Nairobi Securities Exchange |

NSE20 | NSE 20 Share Index |

Probability Density Function | |

AR | Autoregressive |

MA | Moving Average |

ARIMA | Autoregressive Integrated Moving Average |

i.i.d | Independently and Identically Distributed |

| [1] | Tong H., Lim K. S., Threshold Autoregression, Limit Cycles and Cyclical Data. Journal of the Royal Statistical Society: Series B (Methodological). 1980, 42(3), 245-268. |

| [2] | Aydin D., Güneri Ö. İ. Time Series Prediction Using Hybridization of AR, SETAR and ARM Models. International Journal of Applied. 2015, 5(6), 87-96. |

| [3] | Boero G., Lampis F. The Forecasting Performance of SETAR Models: An Empirical Application. Bulletin of Economic Research. 2017, 69(3), 216-228. |

| [4] | Firat E. H. SETAR (Self-Exciting Threshold Autoregressive) Non-Linear Currency Modelling in EUR/USD, EUR/TRY and USD/TRY Parities. Mathematics and Statistics. 2017, 5(1), 33-55. |

| [5] | Gibson D., Nur D. Threshold Autoregressive Models in Finance: A Comparative Approach. In Proceedings of the Fourth Annual ASEARC Conference, University of Western Sydney, Paramatta, Australia, 2011; 18-23. |

| [6] | Oyewale A. M., Adelekan O. G., Innocient O. O. Forecast Comparison of Seasonal Autoregressive Integrated Moving Average (SARIMA) and Self Exciting Threshold Autoregressive (SETAR) Models. American Journal of Theoretical and Applied Statistics. 2017, 6(6), 278-283. |

| [7] | Tobechukwu N. M., Emmanuel B. O., Ibienebaka B. T. Self-Exciting Threshold Autoregressive Modelling of COVID-19 Confirmed Daily Cases in Nigeria. International Journal of Data Science and Analysis. 2022, 8(6), 182-186. |

| [8] | Agiwal V., Kumar, J. Bayesian Estimation for Threshold Autoregressive Model with Multiple Structural Breaks. Metron. 2020, 78(3), 361-382. |

| [9] | Ojo O. O. Bayesian Modelling of Inflation in Nigeria with Threshold Autoregressive Model. Rattanakosin Journal of Science and Technology. 2021, 3(1), 10-18. |

| [10] | Pan J., Xia Q., Liu J. Bayesian Analysis of Multiple Thresholds Autoregressive Model. Computational Statistics. 2017, 32, 219-237. |

| [11] | Onyeka-Ubaka J. N., Ebiringa O. A. Self-exciting Threshold Autoregressive Model with Application to Crude Oil Production in Nigeria. Asian Journal of Probability and Statistics. 2023, 22(1), 1-18. |

| [12] | Andric V., Bodroza D., Djukic M. A Commentary on US Sovereign Debt Persistence and Nonlinear Fiscal Adjustment. Mathematics. 2024, 12(20), 3250. |

| [13] | Bolstad W. M., Curran J. M. Introduction to Bayesian statistics. John Wiley & Sons. 2016, 237-253. |

| [14] | Bisaglia L., Canale A. Bayesian Nonparametric Forecasting for INAR Models. Computational Statistics & Data Analysis. 2016, 100, 70-78. |

| [15] | Drovandi C. C., Pettitt A. N., McCutchan R. A. Exact and Approximate Bayesian Inference for Low Integer-Valued Time Series Models with Intractable Likelihoods. 2016, 11(2) 325 - 352. |

| [16] | Li Y., Yu J., Zeng T. Deviance Information Criterion for Latent Variable Models and Misspecified Models. Journal of econometrics. 2020, 216(2), 450-493. |

| [17] | Yang K., Li H., Wang D. Estimation of Parameters in the Self-Exciting Threshold Autoregressive Processes for Nonlinear Time Series of Counts. Applied Mathematical Modelling. 2018, 57, 226-247. |

APA Style

Muindi, J., Muhua, G., Wanyonyi, R. (2024). Self-Exciting Threshold Autoregressive (SETAR) Modelling of the NSE 20 Share Index Using the Bayesian Approach. American Journal of Theoretical and Applied Statistics, 13(6), 203-212. https://doi.org/10.11648/j.ajtas.20241306.13

ACS Style

Muindi, J.; Muhua, G.; Wanyonyi, R. Self-Exciting Threshold Autoregressive (SETAR) Modelling of the NSE 20 Share Index Using the Bayesian Approach. Am. J. Theor. Appl. Stat. 2024, 13(6), 203-212. doi: 10.11648/j.ajtas.20241306.13

AMA Style

Muindi J, Muhua G, Wanyonyi R. Self-Exciting Threshold Autoregressive (SETAR) Modelling of the NSE 20 Share Index Using the Bayesian Approach. Am J Theor Appl Stat. 2024;13(6):203-212. doi: 10.11648/j.ajtas.20241306.13

@article{10.11648/j.ajtas.20241306.13,

author = {Jacinta Muindi and George Muhua and Ronald Wanyonyi},

title = {Self-Exciting Threshold Autoregressive (SETAR) Modelling of the NSE 20 Share Index Using the Bayesian Approach

},

journal = {American Journal of Theoretical and Applied Statistics},

volume = {13},

number = {6},

pages = {203-212},

doi = {10.11648/j.ajtas.20241306.13},

url = {https://doi.org/10.11648/j.ajtas.20241306.13},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ajtas.20241306.13},

abstract = {The analysis and interpretation of time series data is of great importance across different fields, including economics, finance, and engineering, among other fields. This kind of data, characterized by sequential observations over time, sometimes exhibits complex patterns and trends that some commonly used models, such as linear autoregressive (AR) and simple moving average (MA) models, cannot capture. This limitation calls for the development of more sophisticated and flexible models that can effectively capture the complexity of time series data. In this study, a more sophisticated model, the Self-Exciting Threshold Autoregressive (SETAR) model, is used to model the Nairobi Securities Exchange (NSE) 20 Share Index, incorporating a Bayesian parameter estimation approach. The objectives of this study are to analyze the properties of the NSE 20 Share Index data, to determine the estimates of SETAR model parameters using the Bayesian approach, to forecast the NSE 20 Share Index for the next 12 months using the fitted model, and to compare the forecasting performance of the Bayesian SETAR with the frequentist SETAR and ARIMA model. Markov Chain Monte Carlo (MCMC) techniques, that is, Gibbs sampling and the Metropolis-Hastings Algorithm, are used to estimate the model parameters. SETAR (2; 4, 4) model is fitted and used to forecast the NSE 20 Share Index. The study's findings generally reveal an upward trajectory in the NSE 20 Share Index starting September 2024. Even though a slight decline is predicted in November, an upward trend is predicted in the following months. On comparing the performance of the models, the Bayesian SETAR model performed better than the linear ARIMA model for both short and longer forecasting horizons. It also performed better than its counterpart model, which uses the frequentist approach for a longer forecasting horizon. These results show the applicability of SETAR modeling in capturing non-linear dynamics. The Bayesian approach incorporated for parameter estimation advanced the model even further by providing a flexible and robust way of parameter estimation and accommodating uncertainty.

},

year = {2024}

}

TY - JOUR T1 - Self-Exciting Threshold Autoregressive (SETAR) Modelling of the NSE 20 Share Index Using the Bayesian Approach AU - Jacinta Muindi AU - George Muhua AU - Ronald Wanyonyi Y1 - 2024/11/26 PY - 2024 N1 - https://doi.org/10.11648/j.ajtas.20241306.13 DO - 10.11648/j.ajtas.20241306.13 T2 - American Journal of Theoretical and Applied Statistics JF - American Journal of Theoretical and Applied Statistics JO - American Journal of Theoretical and Applied Statistics SP - 203 EP - 212 PB - Science Publishing Group SN - 2326-9006 UR - https://doi.org/10.11648/j.ajtas.20241306.13 AB - The analysis and interpretation of time series data is of great importance across different fields, including economics, finance, and engineering, among other fields. This kind of data, characterized by sequential observations over time, sometimes exhibits complex patterns and trends that some commonly used models, such as linear autoregressive (AR) and simple moving average (MA) models, cannot capture. This limitation calls for the development of more sophisticated and flexible models that can effectively capture the complexity of time series data. In this study, a more sophisticated model, the Self-Exciting Threshold Autoregressive (SETAR) model, is used to model the Nairobi Securities Exchange (NSE) 20 Share Index, incorporating a Bayesian parameter estimation approach. The objectives of this study are to analyze the properties of the NSE 20 Share Index data, to determine the estimates of SETAR model parameters using the Bayesian approach, to forecast the NSE 20 Share Index for the next 12 months using the fitted model, and to compare the forecasting performance of the Bayesian SETAR with the frequentist SETAR and ARIMA model. Markov Chain Monte Carlo (MCMC) techniques, that is, Gibbs sampling and the Metropolis-Hastings Algorithm, are used to estimate the model parameters. SETAR (2; 4, 4) model is fitted and used to forecast the NSE 20 Share Index. The study's findings generally reveal an upward trajectory in the NSE 20 Share Index starting September 2024. Even though a slight decline is predicted in November, an upward trend is predicted in the following months. On comparing the performance of the models, the Bayesian SETAR model performed better than the linear ARIMA model for both short and longer forecasting horizons. It also performed better than its counterpart model, which uses the frequentist approach for a longer forecasting horizon. These results show the applicability of SETAR modeling in capturing non-linear dynamics. The Bayesian approach incorporated for parameter estimation advanced the model even further by providing a flexible and robust way of parameter estimation and accommodating uncertainty. VL - 13 IS - 6 ER -

Department of Mathematics, University of Nairobi, Nairobi, Kenya

Research Fields: Time Series Analysis and Forecasting, Bayesian Inference, Probability Modeling, Stochastic Processes, Survival Analysis and Epidemiology, Machine Learning

Department of Mathematics, University of Nairobi, Nairobi, Kenya

Research Fields: Time Series, Stochastic Processes, Sample Surveys, Statistical Modeling, Group Testing, Distribution Theory

Department of Mathematics, Egerton University, Nakuru, Kenya

Research Fields: Group Screening Designs & their Applications, Probability Modeling in Biological Processes, Multivariate and Inferential Statistics & Applications, Downscaling of Climate Outlook Forecasts, Times Series Analysis & Applications, Linear & Survival Models

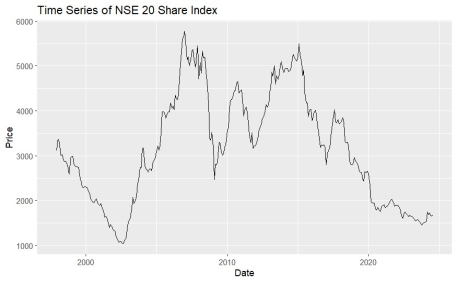

Figure 1. Time Series of NSE 20 share index monthly: Dec 1997 - Aug 2024.

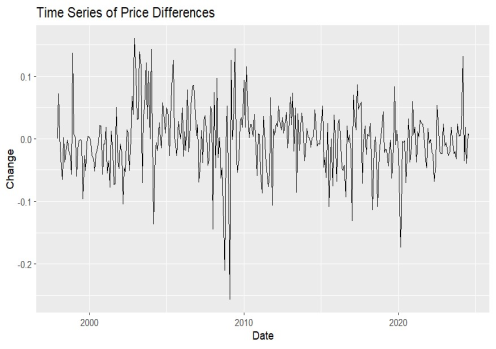

Figure 2. Time Series of Change in NSE 20 Share Index.

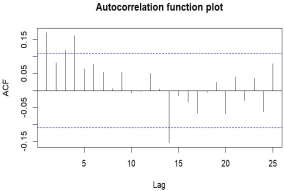

Figure 3. ACF Plot.

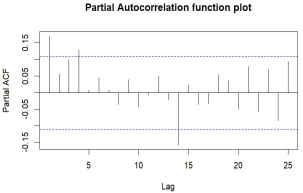

Figure 4. PACF Plot.

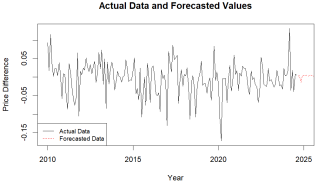

Figure 5. Predicted Future Changes of the NSE20 Index Are Indicated by the Red line.

Figure 6. Original Data and Forecasted Values using Bayesian SETAR and using ARIMA.

Information