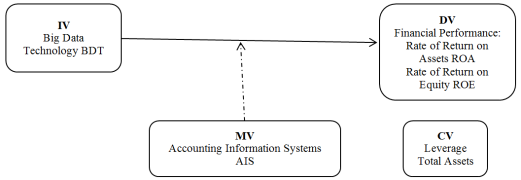

The purpose of this paper is to examine the mediating effect of the rate of quality of accounting information systems on the relationship between big data technology and firms’ financial performance in firms listed on the Palestine Stock Exchange. The researchers conducted an account of the previous studies in this field. The researcher used the deductive approach in studying and analyzing previous studies related to big data by relying on books, periodicals, theses, and accounting standards related to the subject of the research. The researcher applied an inductive approach when conducting the field study and testing the statistical hypotheses related to the study of the relationship between the use of big data technology and firms’ financial performance. The findings show a correlation coefficient of (0.54) and a coefficient of determination of (48%), indicating that big data analytics positively affects the rate of return on assets, and that there is a statistically significant relationship between the advancement of accounting information systems and the enhancement of financial performance in big data technology, as measured by the rate of return on equity and the rate of return on assets, which have correlation rates of (0.53) and (42%), respectively. This relationship is reflected in the data on the existence of a statistically significant relationship between the use of big data technology and the enhancement of financial performance with big data technology. The intention of big data, as well as the absence of fundamental differences between the sample individuals, states that the use of big data technology leads to improved performance through the development of various accounting practices and good inventory management by predicting customer behaviour, thus increasing the competitiveness of competition and improving the reputation of the establishment on social media. This is reflected in the company’s sales and its survival in the market, as well as the development of analytical models and advanced methods of analysis that limit fraud and help control it, which is one of the establishment’s goals at present. This paper contributes to the literature by showing that the use of big data leads to a change in methods of preparing the final accounts, especially the financial position, and displaying them at fair value, which increases investor confidence. The study offers insights into the necessity of holding training courses for accountants concerning technology related to digital transformation and big data analysis for use in developing accounting practices.

| Published in | Journal of Finance and Accounting (Volume 12, Issue 2) |

| DOI | 10.11648/j.jfa.20241202.12 |

| Page(s) | 34-57 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2024. Published by Science Publishing Group |

Big Data Technology, Financial Performance, Accounting Information Systems, Return on Assets, Return on Equity, Palestine Stock Exchange

Variables | Variable Symbol | Measurement Method |

|---|---|---|

Big Data Technology IV | (BDT) | This variable was measured by taking the value (0) if there was no use of big data technology and taking the value (1) if there was a use of big data technology |

Financial Performance DV | Rate of Return on Assets (ROA) | It is measured by dividing net profit after taxes by total assets |

Rate of Return on Equity (ROE) | It is measured by dividing net profit after taxes by total equity | |

Accounting Information Systems MV | AIS | It was measured by taking the value (0) if there is no use of high technology and taking the value (1) if there is a use of technology |

Leverage CV | Financial Leverage (LEV) | Total liabilities over total assets at the end of the year |

Firm Size CV | F-size (FS) | The natural logarithm of total assets at the end of the year |

Model | R | R-Square | Adjusted R-Square | Std. Error of the Estimation |

|---|---|---|---|---|

1 | 0.544 | 0.484 | 0.462 | 1.977012 |

Model | Sum of Squares | DF | Mean Square | F-statistic | Significance |

|---|---|---|---|---|---|

Regression | 49.900 | 3 | 16.633 | 4.256 | 0.003b |

Residual | 570.652 | 146 | 3.909 | - | - |

Total | 620.552 | 149 | - | - | - |

Model | Unstandardized Coefficients | Standardized Coefficients | T | Significance | |

|---|---|---|---|---|---|

B | Std. Error | Beta | |||

Constant | 4.052 | 1.360 | 2.980 | 0.003 | |

Leverage | 0.407 | 0.116 | 0.074 | 0.926 | 0.003 |

Total Assets | -0.174 | 0.063 | 0.222 | 2.773 | 0.001 |

Information Systems | 0.827 | 0.340 | 0.122 | 1.522 | 0.000 |

Model | R | R-Square | Adjusted R-Square | Std. Error of the Estimation |

|---|---|---|---|---|

1 | 0.339a | 0.355 | 0.327 | 7.803983 |

Model | Sum of Squares | DF | Mean Square | F-statistic | Significance |

|---|---|---|---|---|---|

Regression | 115.727 | 3 | 385.242 | 6.326 | 0.000b |

Residual | 8891.715 | 146 | 60.902 | - | - |

Total | 10047.442 | 149 | - | - | - |

Model | Unstandardized Coefficients | Standardized Coefficients | T | Significance | |

|---|---|---|---|---|---|

B | Std. Error | Beta | |||

Constant | 1.527 | 5.368 | 0.284 | 0.004 | |

Leverage | 1.035 | 0.456 | 0.177 | 2.268 | 0.002 |

Total Assets | 0.299 | 0.247 | 0.031 | 0.399 | 0.001 |

Information Systems | 4.774 | 1.342 | 0.280 | 3.556 | 0.001 |

Model | R | R-Square | Adjusted Square | Std. Error of the Estimation |

|---|---|---|---|---|

1 | 0.423a | 0.534 | 0.486 | 4.65176 |

Model | Sum of Squares | DF | Mean Square | F-statistic | Significance |

|---|---|---|---|---|---|

Regression | 368.178 | 3 | 122.726 | 5.672 | 0.001b |

Residual | 3159.268 | 146 | 21.639 | - | - |

Total | 3527.447 | 149 | - | - | - |

Model | Unstandardized Coefficients | Standardized Coefficients | T | Significance | |

|---|---|---|---|---|---|

B | Std. Error | Beta | |||

Constant | 1.263 | 3.200 | - | 0.395 | 0.694 |

Leverage | 2.646 | 0.800 | 0.262 | 3.306 | 0.001 |

Total Assets | 0.571 | 0.272 | 0.165 | 2.099 | 0.038 |

Information Systems | -0.038 | 0.148 | -0.020 | -0.254 | 0.799 |

Series | Job | Number of Listings Sent | Number of Listings Received | Percentage |

|---|---|---|---|---|

1 | Accountants | 45 | 20 | 44% |

2 | Systems Analysts | 50 | 22 | 44% |

3 | System Designers | 25 | 19 | 42% |

4 | Academics | 20 | 14 | 70% |

5 | Big Data Specialist | 20 | 12 | 60% |

Total | 160 | 87 | 54% |

Cronbach’s Alpha | Number of Phrases | Interlocutor |

|---|---|---|

0.938 | 8 | MX1 |

0.655 | 8 | MX2 |

0.648 | 7 | MX3 |

0.747 | 23 | Total |

Erase Phrases | Mean | Significance | DF | T | Standard Deviation |

|---|---|---|---|---|---|

X1.1 Providing the latest technology in information systems | 4.0230 | 0.000 | 86 | 82.12 | 0.45691 |

X1.2 Providing information that facilitates measurement methods in the big data environment | 3.9310 | 0.000 | 86 | 49.29 | 0.74386 |

X1.3 Accounting standards related to the design of information systems in the big data environment | 3.5862 | 0.000 | 86 | 32.50 | 1.02924 |

X1.4 Include in the curricula methods of designing and analyzing information systems in the big data environment | 3.3218 | 0.000 | 86 | 33.18 | 0.93379 |

X1.5 Outsourcing of storage and data processing including cloud computing | 3.5402 | 0.000 | 86 | 41.06 | 0.80413 |

X1.6 Providing material and human resources to adopt modern systems that deal with financial and non-financial information | 4.1839 | 0.000 | 86 | 55.15 | 0.70758 |

X1.7 The need for information literacy for accountants and designers of accounting systems in the big data environment | 4.3333 | 0.000 | 86 | 66.96 | 0.60361 |

X1.8 The need to develop methods of producing information so that it has the appropriate characteristics for decision-making, as well as the need to develop methods of interpreting that information | 3.8966 | 0.000 | 86 | 40.85 | 0.88966 |

Total | 3.8520 | - | - | - | 0.44889 |

Job | Chi-Square | Mean Rank | N | Asymptotic Significance |

|---|---|---|---|---|

Accountants | - | 44.70 | 20 | - |

Systems Analysts | 4.242 | 43.68 | 22 | 0.374 |

System Designers | - | 45.50 | 19 | - |

Academics | - | 51.86 | 14 | - |

Big Data Specialist | - | 31.88 | 12 | - |

Total | - | - | 87 | - |

Erase Phrases | Mean | Significance | DF | T | Standard Deviation |

|---|---|---|---|---|---|

X2.1 Showing the intangible assets in a clearer way, which gives a more comprehensive picture of the performance of the assets | 4.1839 | 0.000 | 86 | 61.122 | 0.63847 |

X2.2 Reduce information asymmetry among stakeholders through real-time reports instead of periodic reports | 4.3333 | 0.000 | 86 | 47.861 | 0.84450 |

X2.3 Identify potential problems within the facility and create solutions that increase the value of the facility | 4.0460 | 0.000 | 86 | 88.000 | 0.42885 |

X2.4 Developing new models to reduce costs, which creates a competitive advantage for the establishment | 4.0805 | 0.000 | 86 | 52.948 | 0.71882 |

X2.5 The use of analytical models and advanced methods of analysis, which limits fraud and helps control | 4.3563 | 0.000 | 86 | 50.375 | 0.80662 |

X2.6 Good inventory management by predicting customer behaviour | 4.4503 | 0.000 | 86 | 48.682 | 0.77672 |

X2.7 Improving the company's reputation on social media, which is reflected in the company's sales and its survival in the market | 4.4122 | 0.000 | 86 | 70.759 | 0.70022 |

X2.8 Changing the methods of preparing the final accounts, especially the financial position, and showing them at fair value, which increases investor confidence | 4.2137 | 0.000 | 86 | 79.909 | 0.52635 |

Mean and general deviation | 4.2514 | - | - | - | 0.39962 |

Job | Chi-Square | Mean Rank | N | Asymptotic Significance |

|---|---|---|---|---|

Accountants | - | 51.80 | 20 | - |

Systems Analysts | 5.312 | 46.43 | 22 | 0.257 |

System Designers | - | 38.18 | 19 | - |

Academics | - | 45.64 | 14 | - |

Big Data Specialist | - | 33.83 | 12 | - |

Total | - | - | 87 | - |

Erase Phrases | Mean | Significance | DF | T | Standard Deviation |

|---|---|---|---|---|---|

X3.1 Lack of accounting standards for how to deal with big data, especially reporting standards | 4.1379 | 0.000 | 86 | 45.331 | 0.85143 |

X3.2 Unavailability of information systems that can handle various forms of data | 3.9540 | 0.000 | 86 | 44.222 | 0.83399 |

X3.3 The high cost of big data analytics specialists | 4.1839 | 0.000 | 86 | 61.122 | 0.63847 |

X3.4 The size, magnitude and diversity of big data make it difficult to deal with it | 4.3333 | 0.000 | 86 | 47.861 | 0.84450 |

X3.5 The difficulty of storing big data in traditional means | 4.0460 | 0.000 | 86 | 88.000 | 0.42885 |

X3.6 The problem of insecure handling of data, which exposes it to theft | 4.0805 | 0.000 | 86 | 52.948 | 0.71882 |

X3.7 Slow companies deal with big data technology, although it has become a reality | 4.3563 | 0.000 | 86 | 50.375 | 0.80662 |

Mean and general deviation | 4.1560 | - | - | - | 0.42892 |

Job | Chi-Square | Mean Rank | N | Asymptotic Significance |

|---|---|---|---|---|

Accountants | - | 45.88 | 20 | - |

Systems Analysts | 2.715 | 45.86 | 22 | 0.607 |

System Designers | - | 48.68 | 19 | - |

Academics | - | 38.43 | 14 | - |

Big Data Specialist | - | 36.54 | 12 | - |

Total | - | - | 87 | - |

BDT | Big Data Technology |

BDA | Big Data Analytics |

AIS | Accounting Information Systems |

BMI | Body Mass Index |

DCT | Dynamic Capabilities Theory |

EMH | Efficient Markets Hypothesis |

FP | Financial Performance |

IT | Information Technology |

ROA | Return on Assets |

ROE | Return on Equity |

PEX | Palestine Stock Exchange |

| [1] | Akter, S., & Wamba, S. F. (2016). Big data analytics in E-commerce: a systematic review and agenda for future research. Electronic Markets, 26(2), 173-194. |

| [2] | Al-Htaybat, K., & von Alberti-Alhtaybat, L. (2017). Big Data and corporate reporting: impacts and paradoxes. Accounting, Auditing & Accountability Journal, 30(4), 850-873. |

| [3] | Al-Okaily, A., Abd Rahman, M. S., Al-Okaily, M., Ismail, W. N. S. W., & Ali, A. (2020). Measuring success of accounting information system: applying the DeLone and McLean model at the organizational level. J. Theor. Appl. Inf. Technol, 98(14), 2697-2706. |

| [4] | Al-Okaily, A., Teoh, A. P., & Al-Okaily, M. (2023). Evaluation of data analytics-oriented business intelligence technology effectiveness: an enterprise-level analysis. Business Process Management Journal, 29(3), 777-800. |

| [5] | Al-Okaily, A., Teoh, A. P., Al-Okaily, M., Iranmanesh, M., & Al-Betar, M. A. (2023). The efficiency measurement of business intelligence systems in the big data-driven economy: a multidimensional model. Information Discovery and Delivery, 51(4), 404-416. |

| [6] | Al-Okaily, M. (2022). Toward an integrated model for the antecedents and consequences of AIS usage at the organizational level. EuroMed Journal of Business, (ahead-of-print). |

| [7] | Al-Okaily, M., Al-Fraihat, D., Al-Debei, M. M., & Al-Okaily, A. (2022). Factors influencing the decision to utilize eTax systems during the COVID-19 pandemic: the moderating role of anxiety of COVID-19 infection. International Journal of Electronic Government Research (IJEGR), 18(1), 1-24. |

| [8] | Alawaqleh, Q. A. (2021). The effect of internal control on employee performance of small and medium-sized enterprises in Jordan: The role of accounting information system. The Journal of Asian Finance, Economics and Business, 8(3), 855-863. |

| [9] | Alberto Ferraris, Alberto Mazzoleni, Alain Devalle, Jerome Couturier, (2018) "Big data analytics capabilities and knowledge management: impact on firm performance", Management Decision. |

| [10] | Alkhatib, Akram and Harasheh, Murad. Market Efficiency: The Case of Palestine Exchange (PEX) (March 10, 2014). World Journal of Social Sciences, Vol. 4. No. 1. March 2014 Issue. Pp. 196-206. |

| [11] | Alqtish, A., Qatawneh, A., & Alhaj, D. (2021). Development of accounting information systems according to the accounting variances and the requirements of international accounting standard (IAS) NO. 1. International Journal of Entrepreneurship, 25, 1-17. |

| [12] | Alrabei, A. M. (2023). Green electronic auditing and accounting information reliability in the Jordanian social security corporation: the mediating role of cloud computing. International Journal of Financial Studies, 11(3), 114. |

| [13] | Amani, F. A., & Fadlalla, A. M. (2017). Data mining applications in accounting: A review of the literature and organizing framework. International Journal of Accounting Information Systems, 24, 32-58. |

| [14] | Anderson, N. (2016). Blockchain Technology: A game-change in accounting? Deloitte. |

| [15] | Appelbaum, D., Kogan, A., & Vasarhelyi, M. A. (2017). Big Data and analytics in the modern audit engagement: Research needs. Auditing: A Journal of Practice & Theory, 36(4), 1-27. |

| [16] | Arif, D., Yucha, N., Setiawan, S., Oktarina, D., & Martah, V. (2020). Applications of goods mutation control form in accounting information system: A case study in sumber indah perkasa manufacturing, Indonesia. Journal of Asian Finance, Economics and Business, 7(8), 419-424. |

| [17] | Arnaboldi, M., Busco, C., & Cuganesan, S. (2017). Accounting, accountability, social media and big data: revolution or hype? Accounting, Auditing & Accountability Journal, 30(4), 762-776. |

| [18] | Aws, A. L., Ping, T. A., & Al-Okaily, M. (2021). Towards business intelligence success measurement in an organization: a conceptual study. Journal of System and Management Sciences, 11(2), 155-170. |

| [19] | Badrinarayanan, V., Madhavaram, S., & Manis, K. T. (2022). Technology-enabled sales capability: A capabilities-based contingency framework. Journal of Personal selling & sales ManageMent, 42(4), 358-376. |

| [20] | Bag, S., Gupta, S., Kumar, A., & Sivarajah, U. (2021). An integrated artificial intelligence framework for knowledge creation and B2B marketing rational decision making for improving firm performance. Industrial marketing management, 92, 178-189. |

| [21] | Balios, D. (2020). The impact of Big Data on accounting and auditing. International Journal of Corporate Finance and Accounting, 7(2). |

| [22] | Balios, D.and Tantos, S. (2019). The characteristics of a fair and efficient tax auditing system as a tool against tax evasion: A theoretical framework. International Journal of Economics and Management Engineering, 13(6), 777-780. |

| [23] | Barker, R., & Schulte, S. (2017). Representing the market perspective: Fair value measurement for non-financial assets. Accounting, Organizations and Society, 56, 55-67. |

| [24] | Bharadwaj, N., & Shipley, G. M. (2020). Salesperson communication effectiveness in a digital sales interaction. Industrial Marketing Management, 90, 106-112. |

| [25] | Cetindamar, D., Phaal, R., & Probert, D. (2009). Understanding technology management as a dynamic capability: A framework for technology management activities. Technovation, 29(4), 237-246. |

| [26] | Chen, D. Q., Preston, D. S., & Swink, M. (2015). How the use of big data analytics affects value creation in supply chain management. Journal of management information systems, 32(4), 4-39. |

| [27] | Chen, J., Tao, Y., Wang, H., & Chen, T. (2015). Big data-based fraud risk management at Alibaba. The Journal of Finance and Data Science, 1(1),1-10. |

| [28] | Coyne, J. G., & McMickle, P. L. (2017). Can Blockchain serve an accounting purpose? Journal of Emerging Technologies in Accounting, 14(2), 101-111. |

| [29] | Coyne, M., Coyne, G., and Walker, B. (2016). Big Data information governance by accountants. International Journal of Accounting & Information Management, Vol. (26), Issue (1). |

| [30] | Davenport, T. H., & Bean, R. (2022). Companies Are Making Serious Money With AI. MIT Sloan Management Review. |

| [31] | Dwivedi, K., Hughes, L., Ismagilova, E., Aarts, G., Coombs, C., Crick, T., & Williams, D. (2021). Artificial Intelligence (AI): Multidisciplinary perspectives on emerging challenges, opportunities, and agenda for research, practice and policy. International Journal of Information Management, 57, 101994. |

| [32] | Erevelles, S., Fukawa, N., & Swayne, L. (2016). Big Data consumer analytics and the transformation of marketing. Journal of business research, 69(2), 897-904. |

| [33] | Fama, E (1972b). Components of investment performance, Journal of Finance, Vol. 27, pp. 551-567. |

| [34] | Fama, E 1970a, ‘Efficient capital markets: a review of theory and empirical work’, Journal of Finance, Vol. 25, pp. 383-417. |

| [35] | Fama, E 1991c, ‘Efficient capital markets: II’, Journal of Finance, Vol. 46, pp. 15751617. |

| [36] | Fama, E and French, K 1992d, ‘The cross-section of expected stock returns’, Journal of Finance, Vol. 47, pp. 427-465. |

| [37] | Fan, S., Lau, R. Y., & Zhao, J. L. (2015). Demystifying big data analytics for business intelligence through the lens of marketing mix. Big Data Research, 2(1), 28-32. |

| [38] | Furneaux, B. (2012). Task-technology fit theory: A survey and synopsis of the literature. Information Systems Theory: Explaining and Predicting Our Digital Society, Vol. 1, 87-106. |

| [39] | Gamage, P. (2016). Big Data: are accounting educators ready? Accounting & Management Information Systems, 15(3), 588-604. |

| [40] | Goodhue, D. L., & Thompson, R. L. (1995). Task-technology fit and individual performance. MIS quarterly, 213-236. |

| [41] | Grewal, D., Guha, A., Satornino, C. B., & Schweiger, E. B. (2021). Artificial intelligence: The light and the darkness. Journal of Business Research, 136, 229-236. |

| [42] | Gupta, S., Justy, T., Kamboj, S., Kumar, A., & Kristoffersen, E. (2021). Big data and firm marketing performance: Findings from knowledge-based view. Technological Forecasting and Social Change, 171, 120986. |

| [43] | Hackius, N., & Petersen, M. (2017). Blockchain in logistics and supply chain: trick or treat? In Proceedings of the Hamburg International Conference of Logistics, (pp. 3-18). Epubli. |

| [44] | Hallikainen, H., Savimäki, E., & Laukkanen, T. (2020). Fostering B2B sales with customer big data analytics. Industrial Marketing Management, 86, 90-98. |

| [45] | Hashim, H. T. (2022). The Reliability and Relevancy of Accounting Information Systems Impact Auditing Profession. American Journal of Economics and Business Management, 5(10), 215-224. |

| [46] | IMF (2017). West Bank and Gaza - Report to the Ad Hoc Liaison Committee. International Monetary Fund. |

| [47] | Jiali Tang, Khondkar E. Karim, (2018) Financial fraud detection and big data analytics – implications on auditors’ use of fraud brainstorming session. Managerial Auditing Journal, |

| [48] | Kantmar, (2018). Analyzing big data: the path to competitive advantage. Electronic Copy Available at http://hosteddocs. ittoolbox.com, (accessed 6 December 2023). |

| [49] | Khaldoon Al-Htaybat, Larissa von Alberti-Alhtaybat. (2017). Big Data and corporate reporting: impacts and paradoxes. Accounting, Auditing & Accountability Journal, Vol. 30 Issue: 4, pp. 850-873. |

| [50] | Kuurila, J. (2016). The role of big data in Finnish companies and the implications of big data on management accounting. Master’s thesis, University of Jyväskylä. |

| [51] | Lee, I. (2017). Big data: Dimensions, evolution, impacts, and challenges. Business Horizons, 60(3), 293-303. |

| [52] | Li, L. (2022). Digital transformation and sustainable performance: The moderating role of market turbulence. Industrial Marketing Management, 104, 28-37. |

| [53] | Liedtke, C. A. (2016). Quality, Analytics, and Big Data. Doctoral dissertation, Strategic Improvement Systems (SIS), (952) 380-0778. |

| [54] | Liu, C., Chen, J., Yang, L., Zhang, X., Yang, C., Ranjan, R., & Rao, K. (2014). Authorized public auditing of dynamic big data storage on the cloud with efficient verifiable fine-grained updates. Parallel and Distributed Systems, IEEE Transaction on, 25(9), 2234-2244. |

| [55] | Major national accounts variables in Palestine for the year 2020, 2021 at constant prices: 2015 is the base year,” Palestinian Central Bureau of Statistics, accessed May 5, 2023. |

| [56] | Mazzei, M. J., & Noble, D. (2017). Big data dreams: A framework for corporate strategy. Business Horizons, 60(3), 405-414. |

| [57] | Mendoza, R. R. (2017). Relationship between intangible assets and cash flows: an empirical analysis of publicly listed corporations in the Philippines. Review of Integrative Business and Economics Research 6(1), 188-202. |

| [58] | Mikalef, P., Krogstie, J., Pappas, I. O., & Pavlou, P. (2020). Exploring the relationship between big data analytics capability and competitive performance: The mediating roles of dynamic and operational capabilities. Information & Management, 57(2), 103169. |

| [59] | Muchenje, G., & Seppänen, M. (2023). Unpacking task-technology fit to explore the business value of big data analytics. International Journal of Information Management, 69, 102619. |

| [60] | N. Nuruzzaman, A.S. Gaur, R. Sambharya, A. (2018). Micro-foundations approach to studying innovation in multinational subsidiaries. Global Strategy Journal (2018), |

| [61] | Palestine Stock Exchange (PEX). |

| [62] | Palestinian Central Bureau of Statistics, Press Release, November 8, 2022, “Results of the Labour Force Survey ird Quarter (July-September, 2022) Round”. |

| [63] | Paschen, J., Wilson, M., & Ferreira, J. J. (2020). Collaborative intelligence: How human and artificial intelligence create value along the B2B sales funnel. Business Horizons, 63(3), 403-414. |

| [64] | Pham, T. L. H., Le, T. T. H., Nguyen, T. T. L., Nguyen, T. T., & Doan, T. D. U. (2022). Impact of management accounting information system on financial performance: evidence from Vietnam wood product export enterprises. Ann. For. Res, 65(1), 5291-5308. |

| [65] | PMA (2017). Financial Stability Report 2016. Ramallah: Palestine Monetary Authority. |

| [66] | Popovič, A., Hackney, R., Tassabehji, R., & Castelli, M. (2018). The impact of big data analytics on firms’ high value business performance. Information Systems Frontiers, 20, 209-222. |

| [67] |

Preliminary results of registered Palestinian exports, and imports of goods by month, quarter, and country for 2021 and 2022,” Palestinian Central Bureau of Statistics, accessed May 5, 2023,

https://www.pcbs.gov.ps/statisticsIndicatorsTables.aspx?lang=en&table_id=1604 |

| [68] | Qatawneh, A. M. (2023). The role of organizational culture in supporting better accounting information systems outcomes. Cogent Economics & Finance, 11(1), 2164669. |

| [69] | Ram, J., Zhang, C., & Koronios, A. (2016). The implications of big data analytics on business intelligence: A qualitative study in China. Procedia Computer Science, 87, 221-226. |

| [70] | Ranjan, J., & Foropon, C. (2021). Big data analytics in building the competitive intelligence of organizations. International Journal of Information Management, 56, 102231. |

| [71] | Rehman, M. H., Chang, V., Batool, A., & Wah, T. Y. (2016). Big data reduction framework for value creation in sustainable enterprises. International Journal of Information Management, 36(6), 917-928. |

| [72] | Rezaee, Z., & Wang, J. (2019). Relevance of Big Data to forensic accounting practice and education. Managerial Auditing Journal, 34(3), 268-288. |

| [73] | Richins, G., Stapleton, A., Stratopoulos, C., & Wong, C. (2017). Big Data analytics: Opportunity or threat for the accounting profession? Journal of Information Systems, 31(3), 63-79. |

| [74] | Saunders, A., & Brynjolfsson, E. (2016). Valuing Information Technology Related Intangible Assets. Mis Quarterly, 40(1). |

| [75] | Schilke, O., Hu, S., & Helfat, C. E. (2018). Quo vadis, dynamic capabilities? A content-analytic review of the current state of knowledge and recommendations for future research. Academy of management annals, 12(1), 390-439. |

| [76] | Shahbaz, M., Gao, C., Zhai, L., Shahzad, F., & Hu, Y. (2019). Investigating the adoption of big data analytics in healthcare: the moderating role of resistance to change. Journal of Big Data, 6(1), 1-20. |

| [77] | Sheng, H., Feng, T., Chen, L., & Chu, D. (2021). Responding to market turbulence by big data analytics and mass customization capability. Industrial Management & Data Systems, 121(12), 2614-2636. |

| [78] | Sledgianowski, D., Gomaa, M., & Tan, C. (2017). Toward an integration of Big Data, technology and information systems competencies into the accounting curriculum. Journal of Accounting Education, 38, 81-93. |

| [79] | Suoniemi, S., Meyer-Waarden, L., Munzel, A., Zablah, A. R., & Straub, D. (2020). Big data and firm performance: The roles of market-directed capabilities and business strategy. Information & Management, 57(7), 103365. |

| [80] | Syam, N., & Sharma, A. (2018). Waiting for a sales renaissance in the fourth industrial revolution: Machine learning and artificial intelligence in sales research and practice. Industrial marketing management, 69, 135-146. |

| [81] | Turner, L., Weickgenannt, A. B., & Copeland, M. K. (2022). Accounting information systems: controls and processes. John Wiley & Sons. |

| [82] | Vasarhelyi, M. A., Kogan, A., & Tuttle, B. M. (2015). Big Data in accounting: An overview. Accounting Horizons, 29(2), 381-396. |

| [83] | Wang, S. L., & Lin, H. I. (2019). Integrating TTF and IDT to evaluate user intention of big data analytics in mobile cloud healthcare system. Behaviour & Information Technology, 38(9), 974-985. |

| [84] | World Bank. (2016). Economic Monitoring Report to the Ad Hoc Liaison Committee. Washington DC: World Bank Group. |

| [85] | Xu, Z., Frankwick, G. L., & Ramirez, E. (2016). Effects of big data analytics and traditional marketing analytics on new product success: A knowledge fusion perspective. Journal of business research, 69(5), 1562-1566. |

| [86] |

Zhang, Juan; Yang, Xiongsheng; and Appelbaum, Deniz. Toward Effective Big Data Analysis in Continuous Auditing. (2015). Department of Accounting and Finance Faculty Scholarship and Creative Works. 132.

https://digitalcommons.montclair.edu/acctg-finance-facpubs/132 |

| [87] | Zhao, Z., & Yang, Y. (2017). Influence of Big Data on Manufacturing Industry and Strategies of Enterprises: A Literature Review. In MATEC Web of Conferences (Vol. 100, p. 02019). EDP Sciences, 9(2), 469-476. |

| [88] | Zhang, X., Gu, N., Chang, J., & Ye, H. (2021). Predicting stock price movement using a DBN-RNN. Applied Artificial Intelligence, 35(12), 876-892. |

APA Style

Faza, M., Badwan, N. (2024). Big Data Technology and Financial Performance of Listed Firms in Palestine: Mediating Role of Accounting Information Systems. Journal of Finance and Accounting, 12(2), 34-57. https://doi.org/10.11648/j.jfa.20241202.12

ACS Style

Faza, M.; Badwan, N. Big Data Technology and Financial Performance of Listed Firms in Palestine: Mediating Role of Accounting Information Systems. J. Finance Account. 2024, 12(2), 34-57. doi: 10.11648/j.jfa.20241202.12

@article{10.11648/j.jfa.20241202.12,

author = {Mustafa Faza and Nemer Badwan},

title = {Big Data Technology and Financial Performance of Listed Firms in Palestine: Mediating Role of Accounting Information Systems

},

journal = {Journal of Finance and Accounting},

volume = {12},

number = {2},

pages = {34-57},

doi = {10.11648/j.jfa.20241202.12},

url = {https://doi.org/10.11648/j.jfa.20241202.12},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.jfa.20241202.12},

abstract = {The purpose of this paper is to examine the mediating effect of the rate of quality of accounting information systems on the relationship between big data technology and firms’ financial performance in firms listed on the Palestine Stock Exchange. The researchers conducted an account of the previous studies in this field. The researcher used the deductive approach in studying and analyzing previous studies related to big data by relying on books, periodicals, theses, and accounting standards related to the subject of the research. The researcher applied an inductive approach when conducting the field study and testing the statistical hypotheses related to the study of the relationship between the use of big data technology and firms’ financial performance. The findings show a correlation coefficient of (0.54) and a coefficient of determination of (48%), indicating that big data analytics positively affects the rate of return on assets, and that there is a statistically significant relationship between the advancement of accounting information systems and the enhancement of financial performance in big data technology, as measured by the rate of return on equity and the rate of return on assets, which have correlation rates of (0.53) and (42%), respectively. This relationship is reflected in the data on the existence of a statistically significant relationship between the use of big data technology and the enhancement of financial performance with big data technology. The intention of big data, as well as the absence of fundamental differences between the sample individuals, states that the use of big data technology leads to improved performance through the development of various accounting practices and good inventory management by predicting customer behaviour, thus increasing the competitiveness of competition and improving the reputation of the establishment on social media. This is reflected in the company’s sales and its survival in the market, as well as the development of analytical models and advanced methods of analysis that limit fraud and help control it, which is one of the establishment’s goals at present. This paper contributes to the literature by showing that the use of big data leads to a change in methods of preparing the final accounts, especially the financial position, and displaying them at fair value, which increases investor confidence. The study offers insights into the necessity of holding training courses for accountants concerning technology related to digital transformation and big data analysis for use in developing accounting practices.

},

year = {2024}

}

TY - JOUR T1 - Big Data Technology and Financial Performance of Listed Firms in Palestine: Mediating Role of Accounting Information Systems AU - Mustafa Faza AU - Nemer Badwan Y1 - 2024/06/19 PY - 2024 N1 - https://doi.org/10.11648/j.jfa.20241202.12 DO - 10.11648/j.jfa.20241202.12 T2 - Journal of Finance and Accounting JF - Journal of Finance and Accounting JO - Journal of Finance and Accounting SP - 34 EP - 57 PB - Science Publishing Group SN - 2330-7323 UR - https://doi.org/10.11648/j.jfa.20241202.12 AB - The purpose of this paper is to examine the mediating effect of the rate of quality of accounting information systems on the relationship between big data technology and firms’ financial performance in firms listed on the Palestine Stock Exchange. The researchers conducted an account of the previous studies in this field. The researcher used the deductive approach in studying and analyzing previous studies related to big data by relying on books, periodicals, theses, and accounting standards related to the subject of the research. The researcher applied an inductive approach when conducting the field study and testing the statistical hypotheses related to the study of the relationship between the use of big data technology and firms’ financial performance. The findings show a correlation coefficient of (0.54) and a coefficient of determination of (48%), indicating that big data analytics positively affects the rate of return on assets, and that there is a statistically significant relationship between the advancement of accounting information systems and the enhancement of financial performance in big data technology, as measured by the rate of return on equity and the rate of return on assets, which have correlation rates of (0.53) and (42%), respectively. This relationship is reflected in the data on the existence of a statistically significant relationship between the use of big data technology and the enhancement of financial performance with big data technology. The intention of big data, as well as the absence of fundamental differences between the sample individuals, states that the use of big data technology leads to improved performance through the development of various accounting practices and good inventory management by predicting customer behaviour, thus increasing the competitiveness of competition and improving the reputation of the establishment on social media. This is reflected in the company’s sales and its survival in the market, as well as the development of analytical models and advanced methods of analysis that limit fraud and help control it, which is one of the establishment’s goals at present. This paper contributes to the literature by showing that the use of big data leads to a change in methods of preparing the final accounts, especially the financial position, and displaying them at fair value, which increases investor confidence. The study offers insights into the necessity of holding training courses for accountants concerning technology related to digital transformation and big data analysis for use in developing accounting practices. VL - 12 IS - 2 ER -

Department of Accounting, Higher Institute of Accountancy and Enterprise Management, Manouba University, Manouba, Tunisia

Computerized Finance and Banking Sciences Department, Faculty of Business and Economics, Palestine Technical University-Kadoorie (PTUK), Tulkarm, State of Palestine

Information