Abstract

Under the policy framework highlighted by the 20th National Congress of the Communist Party of China, which advocates for ‘actively and steadily promoting carbon peak and carbon neutrality’, this study investigates the pricing mechanism of China Emission Allowance (CEA) swing options in the carbon market, aligned with the practical needs of the ‘Interim Regulations on the Management of Carbon Emission Trading’. In line with the policy outlined by the 20th National Congress of the Communist Party of China, which emphasizes the "active and steady progress toward carbon peaking and carbon neutrality," this paper delves into the pricing mechanism of CEA swing options in the carbon market. This article mainly introduces the CEA swing option product, which is an innovative financial instrument that aims to provide flexible risk management means for high-carbon emission industries such as electricity, petrochemicals and manufacturing. This paper analyses the descriptive statistical results of the characteristics and data of the CEA market, based on the Market regional conversion model, and adjusts it in combination with the stochastic fluctuation model, so as to determine the CEA value model. At the same time, this article also emphasises the importance of implementing a flexible product management mechanism, including risk tips, regulatory measures, and rolling issuance and adjustment strategies for products to ensure that products can effectively serve the needs of the target market. The research results of this article play an important role in improving the liquidity of the carbon market and helping relevant enterprises avoid the risks caused by fluctuations in the price of carbon emissions. By introducing swing options, it can not only provide more flexible risk management tools for high-carbon emission enterprises, but also promote the healthy development of the carbon emission trading market and encourage more market entities to participate in energy conservation and emission reduction actions.

Keywords

China Emission Allowance, Swing Options, Risk Management, Markov System Conversion Model, Carbon Price Fluctuation

1. Product Overview and Design Concept

1.1. Background of Product Design

Global climate change has become a central focus of international concern, with governments and organizations worldwide taking measures to address this critical issue

| [8] | Pawłowski A, Rydzewski P. Pathways to Carbon Neutrality: Integrating Energy Strategies, Policy, and Public Perception in the Face of Climate Change—A Global Perspective [J]. Energies, 2024, 17(23): 5867. |

[8]

. The carbon emissions trading market serves as a pivotal mechanism for combating climate change, increasingly acknowledged for its effectiveness

| [9] | Liu Q, Yin Y. Strategies for Emission Reduction in Construction: The Role of China’s Carbon Trading Market [J]. Journal of the Knowledge Economy, 2024: 1-30. |

[9]

. This market enables governments to set a cap on total carbon emissions and allocate CEA to businesses, which may then trade these quotas, thus fostering economic incentives for emission reduction

| [7] | Zhao Z, Zhao Y, Shi X, et al. Green innovation and carbon emission performance: The role of digital economy [J]. Energy Policy, 2024, 195: 114344. |

[7]

.

China has committed actively to addressing climate change, particularly through carbon emissions management. As outlined by the Chinese government, carbon emissions are projected to peak before 2030 and achieve carbon neutrality by 2060. These objectives not only reflect China's resolve in global climate governance but also its dedication to sustainable development. In 2021, the Chinese government inaugurated the national carbon emissions trading market, designed to facilitate carbon emission reduction through market mechanisms

| [1] | Liu, Jun, Peng Zhang, and Xiaofei Wang. "Exploring the Mechanisms and Pathways Through Which the Digital Transformation of Manufacturing Enterprises Enhances Green and Low-Carbon Performance Under the “Dual Carbon” Goals." Sustainability 17.3 (2025): 1162. |

[1]

.

Aligning with international carbon markets, China is dedicated to establishing a linkage with global markets

| [2] | Chen X, Zhang M. Carbon emission trading market: international experience, Chinese characteristics and policy recommendations [J]. Shanghai Finance, 2022, 9: 22-33. |

[2]

. Through this mechanism, China aims to make a significant contribution to the achievement of global emission reduction targets while fostering the green transformation of its economy

| [12] | Zhao S, Zhang L, An H, et al. Has China's low-carbon strategy pushed forward the digital transformation of manufacturing enterprises? Evidence from the low-carbon city pilot policy [J]. Environmental impact assessment review, 2023, 102: 107184. |

| [14] | Zhang H, Gao S, Zhou P. Role of digitalization in energy storage technological innovation: Evidence from China [J]. Renewable and Sustainable Energy Reviews, 2023, 171: 113014. |

[12, 14]

. The establishment of the national carbon emissions trading market represents a critical step for China in the global carbon market. Initially, this market primarily focused on the power industry, a significant source of carbon emissions. By setting emission quotas for power companies and enabling them to trade these quotas, this mechanism seeks to encourage enterprises to enhance energy efficiency and reduce carbon emissions.

Overall, China's carbon emissions trading market serves as a vital tool for achieving carbon emission targets, enabling enterprises to lower emissions through market-driven mechanisms and contributing to global climate objectives. The future enhancement and expansion of this market are expected to profoundly influence global climate governance.

1.2. Product Design Concept

Although the carbon market has played a significant role in promoting emission reductions, its price volatility has become a key issue constraining the stable operation of the market. Carbon emission allowances prices are influenced by multiple factors such as policy adjustments, energy price fluctuations, and macroeconomic conditions, exhibiting significant volatility characteristics. For instance, in 2022, the EU carbon market price once exceeded 100 euros per ton, but then plummeted due to factors such as the energy crisis. This volatility brings substantial cost uncertainty to emission control companies, increasing their compliance risks; at the same time, it affects the willingness of financial institutions and investors to participate, limiting the liquidity and depth of the carbon market.

In the carbon emission trading market, traditional carbon market derivatives such as futures and vanilla options are commonly employed for risk management

| [4] | Shi B, Li N, Gao Q, et al. Market incentives, carbon quota allocation and carbon emission reduction: evidence from China's carbon trading pilot policy [J]. Journal of Environmental Management, 2022, 319: 115650. |

| [6] | Tjon Akon M. The role of market operators in scaling up voluntary carbon markets [J]. Capital Markets Law Journal, 2023, 18(2): 259-275. |

[4, 6]

. However, these often deliver a single, fixed trading strategy that may not fully accommodate the complexity and uncertainty of price and quota fluctuations in the carbon market

| [5] | Zhou K, Yang S. Demand side management in China: The context of China’s power industry reform [J]. Renewable and Sustainable Energy Reviews, 2015, 47: 954-965. |

[5]

. The limitation of such products is that participants in the carbon emission market frequently need to modify the quantity of carbon emission allowances they purchase or sell in response to market dynamics. Essentially, participants must meticulously manage the dual risks of quantity and price that they encounter in the carbon market.

Against this backdrop, the development of a more flexible financial derivative has become an urgent need. A swing option, as an option product that allows the holder to exercise multiple times within a specific period, can provide market participants with more refined risk management tools, effectively addressing the volatility of carbon emission allowances prices. Therefore, designing a swing option product based on carbon emission allowances not only has theoretical innovation but also offers new solutions for the stable operation and sustainable development of the carbon market.

The fundamental concept of this product design is to offer a carbon financial instrument—a carbon quota swing option—that facilitates flexible risk management of CEQ through financial innovation, designed to meet the varied needs of carbon market participants in navigating price fluctuations and quota adjustments. The swing option, a novel type of derivative, is crafted to provide holders the ability to adjust the quantity of CEQ bought and sold multiple times within a designated period, thereby bolstering their risk management capabilities amid market volatility.

The introduction of swing options addresses the need for managing these dual risks, offering participants more adaptable and effective risk management tools. These tools allow for the flexible adjustment of allowance quantities in various market conditions, responding to substantial market price swings and achieving more accurate risk hedging. This adaptability is especially critical in the carbon market, influenced by factors such as policy shifts, market supply and demand changes, and macroeconomic conditions. Swing options enable participants to promptly adjust their allowance strategies when these factors affect market prices, effectively managing their risk exposure. For example, if the market anticipates a significant rise in future carbon prices, holders can hedge against this risk by increasing their allowance purchases; alternatively, if a decline is expected, they can sell more allowances to secure the current price level.

In addition, this study also considers product design from the perspective of aiding market participants in optimizing their balance sheets

| [3] | Schroeder R G, Clark M W, Cathey J M. Financial accounting theory and analysis: text and cases [M]. John Wiley & Sons, 2022. |

| [10] | Mink R. Implementation of the 2008 SNA and BPM6 in the area of financial accounts [J]. The IFC’s contribution to the 57th ISI Session, Durban, 2010, 33: 18-37. |

[3, 10]

. Through this flexible option tool, participants can maintain control over their carbon emission costs in a complex market environment, alleviating financial strain caused by price volatility. The introduction of CEA swing options also contributes to the further development and maturation of the carbon market, enhancing market liquidity and improving market efficiency.

As an innovative financial tool, CEA swing options offer carbon market participants a more flexible and efficient risk management solution. This tool enables participants to better handle market price fluctuations and quantity risks, as well as optimize their corporate balance sheets in an ever-changing market environment, achieving precise management of carbon emission market risks under reduced financial pressure.

1.3. Research Significance

Against the backdrop of global climate change response, the carbon market, as an important tool for promoting the achievement of emission reduction targets, has increasingly attracted attention. However, the drastic fluctuations in CEA prices have brought significant risks to emission control enterprises, financial institutions, and other market participants, urgently requiring effective risk management tools. Swing options, as a flexible financial derivative, can provide protection against price volatility for market participants, while enhancing market liquidity and price discovery functions. This paper develops and designs swing option products based on CEA, not only filling the gap in the research field of carbon market financial derivatives but also facilitating risk refinement management under the "dual carbon" goals. In addition, this research helps to promote the deep integration of the carbon market with the financial market, encourage the diversified development of carbon financial products, and thus enhance the operational efficiency and stability of the carbon market. Therefore, the research in this paper has significant theoretical value and practical significance, providing new ideas and solutions for the healthy development of China's and even the global carbon market.

2. Product Underlying Asset: The Market Characteristics and Modeling of CEA

CEA serve as the core carbon reduction permits in China's national carbon market, regulated by the Ministry of Ecology and Environment, and represent a specific quantity of carbon dioxide emission rights

| [13] | Bailey I, Maresh S. Scales and networks of neoliberal climate governance: the regulatory and territorial logics of European Union emissions trading [J]. Transactions of the Institute of British Geographers, 2009, 34(4): 445-461. |

[13]

. The government allocates CEAs to enterprises to meet emission reduction targets, using market mechanisms to allocate and control emissions effectively. Enterprises may purchase carbon emission allowances or trade surplus allowances

| [11] | Starkey R, Anderson K. Domestic Tradable Quotas: A policy instrument for reducing greenhouse gas emissions from energy use [M]. Norwich, UK: Tyndall Centre for Climate Change Research, 2005. |

[11]

. CEA trading is influenced by market supply and demand dynamics and the impact of policies, with allocations based on historical emissions and industry benchmarks. CEAs have a defined validity period, and enterprises must possess sufficient CEAs to cover their emissions; failing to do so results in penalties for non-compliance. The investment value of CEAs is affected by various factors, including policy changes, market supply and demand, and international carbon prices. As China's carbon market matures, the investment value of CEAs becomes increasingly significant.

2.1. Characteristics, Influencing Factors, and Functions of CEA

The characteristics of CEA primarily encompass:

1) Government Allocation: The initial allocation is conducted by the Ministry of Ecology and Environment or its authorized agencies, based on factors such as historical emissions of enterprises and industry benchmarks.

2) Tradability: Enterprises holding CEA can buy and sell in the carbon market. Enterprises that reduce emissions can sell their surplus CEA, while those requiring additional quotas can purchase them.

3) Validity Period: CEAs typically have a designated validity period, such as a trading year. Enterprises must use or trade their held CEA within this period or they may face fines or other penalties.

4) Compliance Requirements: Enterprises must ensure that the amount of CEA they hold is sufficient to cover their actual emissions during the reporting period; failing to do so may lead to regulatory violations and potential exclusion from future carbon market transactions.

5) Price Fluctuations: Prices are influenced by various factors, including policy changes, market supply and demand, and fluctuations in international carbon market prices.

The main factors affecting CEA prices include:

1) Policy Factors: Government carbon reduction policies, quota allocation methods, and regulatory intensity can all influence prices.

2) Market Supply and Demand: The emission reduction capabilities of enterprises, changes in market demand, and investor expectations all affect the supply-demand balance and price levels of CEA.

3) International Carbon Market Prices: Global carbon market price trends and linkage effects also impact domestic prices.

The roles of CEA primarily include:

1) Carbon Emission Reduction Incentives: By setting and allocating quotas, enterprises are incentivized to reduce carbon emissions. Enterprises can profit from selling excess quotas resulting from over-reduction; excess emissions necessitate purchasing quotas, thereby increasing costs and promoting reductions.

2) Market Mechanism Regulation: Making carbon reduction a tradable commodity allows market supply and demand to determine prices, optimizing resource allocation and influencing enterprise emission reduction strategies and investments.

3) Promoting Low-Carbon Transition: Facilitating the adoption of low-carbon technologies and green investments to assist China's economy in transitioning to a low-carbon, green, and sustainable development model.

2.2. Analysis of Trends in China's CEA Market Prices and Transaction Volumes

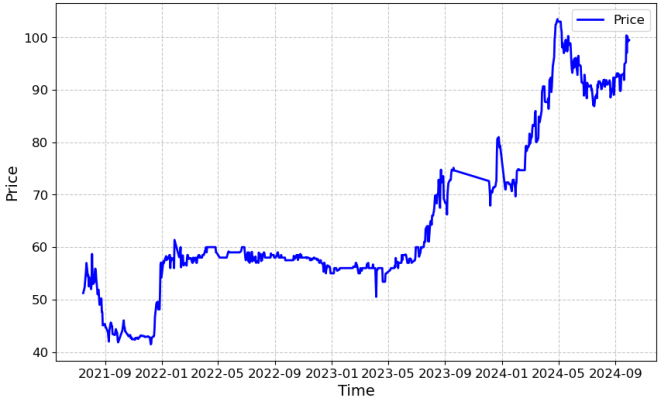

According to the latest data from the Fudan University Center for Sustainable Development, the expected buying price of the national carbon market CEA in September 2024 is 86.66 yuan/ton, the expected selling price is 93.11 yuan/ton, and the average price is 89.88 yuan/ton. This indicates that the current CEA price is at a high level, and market expectations are relatively optimistic. Market prices have been collected since the listing of CEA, and a time series chart is illustrated in

Figure 1.

Figure 1. Market prices since the listing of CEA.

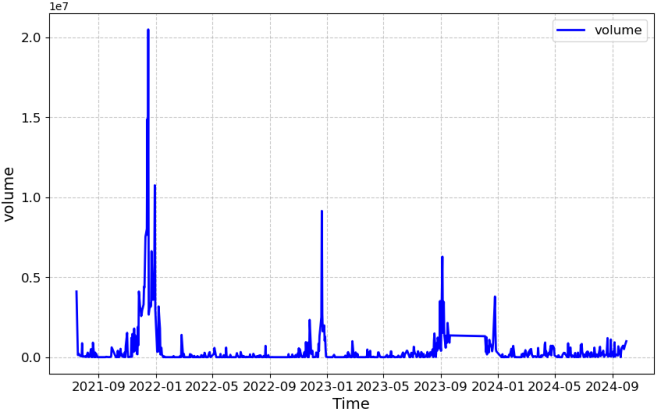

Figure 2. Trading volume since CEA's listing.

From the above results, it can be observed that CEA prices exhibit strong volatility, and their actual prices are influenced by various factors previously mentioned. Therefore, in the absence of suitable hedging tools, enterprises and investors should closely monitor market dynamics and policy changes when participating in carbon market transactions to mitigate price risks to some extent. In addition, quantity risk is another critical aspect that investors need to consider. The trading volume of CEA since its listing displays a pronounced spike trend (

Figure 2), which underscores the importance of managing quantity risk when designing hedging tools for carbon financial instruments.

2.3. CEA Price Model

The selection of appropriate pricing models is crucial in the pricing of swing options with CEA as the underlying asset. Considering the characteristics of the CEA market and the descriptive statistical results, this study adopts the Markov Regime-Switching Model, supplemented by a stochastic volatility model, to more accurately reflect the uncertainty of the CEA market. The Markov Regime-Switching Model is extensively used to analyze the volatility and switching mechanisms of financial asset prices under varying market conditions, and is commonly applied in pricing energy-related financial assets such as electricity, natural gas, and oil prices

| [16] | Huisman, R., and Mahieu, R. Regime jumps in electricity prices [J]. Energy Economics, 2003, 25(5): 425–434. |

| [18] | Janczura, J., and Weron, R. An empirical comparison of alternate regime-switching models for electricity spot prices [J]. Energy Economics, 2010, 32(5): 1059–1073. |

| [19] | Lyle, M. R., and Elliott, R. J. A ‘simple’ hybrid model for power derivatives [J]. Energy Economics, 2009, 31(5): 757-767. |

| [20] | Mount, T. D., Ning, Y. M., and Cai, X. B. Predicting price spikes in electricity markets using a regime-switching model with time-varying parameters [J]. Energy Economics, 2005, 28(1): 62-80. |

[16, 18-20]

. This model effectively captures the volatility and phase transition characteristics of financial asset prices, making it well-suited for the CEA market, which is similarly influenced by diverse factors. By employing this model, the study can deeply analyze volatility patterns and trends of CEA prices under various market conditions, thus providing a foundation for investors and policymakers to better understand dynamic market changes, and laying the groundwork for the pricing and simulation of swing options with CEA as the underlying asset.

Given the option expiration date represented as, consider the probability space which is a Brownian motion adapted to the domain flow under the risk-neutral measure, and is a continuous-time Markov process that is independent of . Additionally, takes values in the state space ,and has a generator matrix , which satisfies the conditions: and. Next, let the random process represent the CEA price, which evolves according to the following stochastic differential equation (SDE):

(1)

In equation (

1),

is a function dependent on an underlying state variable

, representing the system's offset in the absence of a regressive force.

is a regressive term that depends on the current state value

and the regressive strength parameter

, and his term drives the system in the direction of the long-term mean.

is a function that represents the amplitude of random fluctuations of the system, depending on the state variable

. Furthermore, the initial condition is precisely equation (2), which specifies that

. For ease of reference, we use the notation

to denote the CEA price at time

, where the superscript indicates at time

, and

.

3. Product Design: CEA Swing Options with Total Emission Constraints

3.1. Product Proposal

Based on current carbon reduction targets and strategic needs, as well as the limited range of existing carbon financial products for investors, which lack derivatives such as futures and options and result in insufficient market liquidity, our team has integrated the scenario of total emission constraints with national carbon emission control strategies. This integration involves setting clear upper limits on corporate emissions. As the country intensifies carbon emission controls, future CEQ are expected to tighten progressively, complicating the acquisition of quotas for companies. Facing the dual pressures of policies and market dynamics, companies are increasingly adopting proactive strategies to manage carbon emission restrictions, finding that "swing options" are well-suited to adapting to market changes and offer high return potential. Swing options allow holders to buy and sell a specified quantity of emission rights at a preset price within a designated future period, making them an ideal tool for participants in the carbon market to hedge against risks associated with future price fluctuations and market volatility.

In the context of stringent carbon emission reduction policies, carbon emission rights have become a valuable asset, with prices affected by various factors such as market supply and demand, economic conditions, policy regulation, and the energy structure. These factors lead to significant price fluctuations that are difficult to predict. The increasing rigor of global carbon emission controls has heightened the volatility in the prices of carbon emission rights. Swing options offer enterprises a flexible mechanism to manage these risks. When facing risks in the carbon emission rights market, enterprises can exercise swing options to acquire or sell carbon emission rights at an agreed price, thereby locking in costs or profits and mitigating risk losses.

3.2. Product Pricing Strategy

In the intricate domain of financial derivatives pricing and trading strategy research, evaluating option value accurately and devising optimal trading strategies constitute pivotal steps. Here’s a conceptual approach to tackle these tasks:

Firstly, leverage professional financial models and mathematical algorithms to simulate the price trajectory of the underlying asset. This necessitates a holistic consideration of various market volatility factors, historical data, and the macroeconomic environment to generate a representative suite of price curves. Subsequent to simulating these price paths, meticulously calculate the option value for each path. This typically involves computing the intrinsic value at every conceivable trading point for each simulated asset price path, which entails comparing the current asset price with the option strike price to ascertain the immediate exercise value of the option at that moment.

Once these calculations are completed, proceed to the crucial phase of determining the optimal trading strategy. On each simulated path, identify the optimal trading strategy, specifying when and how many options should be exercised. Given the inherent uncertainty in financial market dynamics, often employ dynamic programming or other optimization techniques to maximize expected returns. Dynamic programming involves breaking down the complex decision-making process into simpler sub-problems, solving them step-by-step from the most basic point in time, and considering all potential future price movements and returns at each stage to determine the optimal present decision. Utilize Monte Carlo simulations to identify strategies that maximize expected returns across various possible scenarios through extensive stochastic simulations of market conditions.

Lastly, compute the expected value. Having determined the option value and optimal trading strategy for each simulated path, derive the expected value of the option by averaging the option values across all simulated paths. This step offers a comprehensive perspective on the average option value under different market conditions. Subsequently, incorporate the time value of money by discounting this expected value to the present time to obtain the present value of the option. By discounting the future expected value at a specified discount rate, one can accurately assess the true current value of the option, thereby providing a more robust foundation for investors’ decision-making.

3.3. Design of CEA Swing Options and Their Mathematical Description

The CEA swing option contract encompasses elements such as contract terms, subjects, types, trading units, and exercise methods. In addition, this study provides a mathematical description of the various contract elements of swing options, integrating the design presented in reference

| [17] | Jaillet, P., Ronn, E. I., and Tompaidis, S. Valuation of commodity-based swing options [J]. Management Science, 2004, 50(7): 909-921. |

[17]

. This integration not only elucidates the product design but also establishes a foundation for the subsequent pricing discussions of CEA swing options. The definitions of these contract elements are delineated as follows:

1) The swing option contract, signed at time, remains valid from to . During this period, the holder may exercise delivery rights at any time, provided that the minimum interval between consecutive deliveries satisfies . The total number of allowable deliveries under the contract is capped at .

2) Deliverable quantity at the exercise time point: If the limit for a single delivery quantity is met, this means that for any, the deliverable quantity should be within the following range:

4) Penalty function: The imposition of a penalty on the holder of the CEA swing option at expiration depends on the total delivery quantity during the option's validity period, with the penalty amount symbolically represented. The penalty and punishment functions are critical in risk management for CEA swing options. Through the establishment of these mechanisms, the options encourage cautious exercise of rights by the holders and contribute to maintaining market stability and fairness. In practice, various penalty and punishment functions may be selected and adjusted based on market conditions and the transactional requirements of both parties.

5) The delivery prices of the swing option are specified as , where each may remain fixed or adjust dynamically over time.

6) Total delivery quantity constraint: This constraint limits the total delivery quantity within a specified range. If this range is exceeded, a penalty will be imposed, that is, the holder must pay the predetermined cash amount to the option seller according to the pre-agreed function. From the perspective of modelling, in order to reflect this constraint, we can choose to introduce the penalty function.

| [15] | Basei, M., Cesaroni, A., Vargiolu, T. Optimal exercise of swing contracts in energy markets: an integral constrained stochastic optimal control problem [J]. SIAM Journal on Financial Mathematics, 2014, 5(1): 581-608. |

[15]

Specifically, at time

, if the total delivery quantity falls outside the stipulated range, the option holder could face a penalty. Common punishment functions include the following model:

whererepresents the total accumulated delivery quantity during the option's validity periodrepresents the price of the underlying carbon emissions at the option's expiration, and is a positive constant denoting the penalty for insufficient delivery by the option holder.

3.4. Product Innovation Points and Advantages Comparison

3.4.1. Product Characteristics

1) Swing options enable enterprises to respond flexibly to market changes, allowing them to settle at any time before the option expiration date and choose different shares. This flexibility helps enterprises adjust their carbon emission strategies according to market conditions and their own needs, thus more effectively hedging against price and quantity risks.

2) By setting different total rights, single delivery shares, total delivery shares, and delivery time intervals, enterprises can precisely manage carbon emission costs, maximizing cost-effectiveness.

3.4.2. Product Functions

The national carbon market, an important market-based mechanism for China to respond to climate change and reduce carbon emissions, has garnered significant international attention regarding its operational status. In this context, swing options, as an emerging financial derivative, are increasingly demonstrating their unique functions. They serve as an effective tool for enterprises to manage risks. With significant price fluctuations in the national carbon market, enterprises can hedge against these risks by purchasing swing options, thereby mitigating economic losses due to price changes. Furthermore, given the long compliance period in the national carbon market, enterprises may face substantial price fluctuations in carbon emission rights. Swing options enable enterprises to adjust their compliance strategies and reduce compliance costs.

The introduction of swing options enriches the trading products available in the national carbon market, offering more risk management tools and promoting market development. Additionally, the trading of swing options increases trading opportunities among market participants, enhances market liquidity, and aids in market price discovery.

Enterprises can utilize swing options for strategic trading, such as purchasing at price lows and selling at price highs, thereby increasing profit opportunities. Additionally, swing options can be integrated into an enterprise's asset allocation, used alongside other risk management tools to enhance asset allocation efficiency and reduce overall risk levels. Swing options also assist enterprises in managing carbon emission risks more effectively, promoting carbon reduction and the development of green finance. The introduction of swing options can attract more investors to the national carbon market, further enhancing the growth of green finance.

3.4.3. Advantages of Swing Options

Swing options provide greater flexibility in terms of delivery time and quantity, allowing for the selection of delivery frequency and quantity based on actual needs. This contrasts with European/American options, which typically can only be exercised on or before the expiration date, with fixed delivery quantities for each exercise.

Options can be classified into two types based on the exercise flexibility: European options and American options. American options can be exercised at any time before expiration, offering flexibility that allows investors to respond to market price fluctuations. However, they also grant greater rights to the buyer, resulting in higher option premiums, more complex contract deliveries, and greater risks for option sellers, which may affect the liquidity of the carbon options market and, consequently, the hedging effectiveness for enterprises with controlled emission demands. In contrast, although European options lack flexibility in exercise timing, they are more suitable for enterprises with actual emission control needs in China's early stages of carbon trading development, providing a more stable framework for achieving hedging

| [4] | Shi B, Li N, Gao Q, et al. Market incentives, carbon quota allocation and carbon emission reduction: evidence from China's carbon trading pilot policy [J]. Journal of Environmental Management, 2022, 319: 115650. |

[4]

.

4. Market application and Product Operation

4.1. Customer Positioning and Issuance Scale

4.1.1. Customer Group Analysis

As a financial derivative, swing options serve as a novel risk management tool in the carbon emission trading market. Potential customers for this product include large carbon-emitting enterprises, professional carbon asset management companies, and financial institutions, all characterized by strong risk management requirements and high market engagement.

High-emission industries: These primarily comprise the electricity, steel, cement, and chemical sectors. Enterprises within these sectors often emerge as principal buyers in the carbon emission trading market due to their substantial emissions and stringent regulatory constraints, leading to significant demand for carbon emission allowances. For example, the national carbon market now includes the power generation sector, which contributes approximately 40% to the total national emissions. These enterprises leverage financial instruments like swing options to hedge against the risks associated with carbon price volatility and to stabilize long-term compliance costs.

Professional carbon asset management companies: In a landscape where enterprises, particularly major carbon emitters, confront increasingly severe emission limits, professional carbon asset management companies play a crucial role as partners in managing overall carbon emission constraints. Their services span verification, emission reduction technology management, carbon trading, and carbon sink management. These companies offer a suite of services to enterprises, including establishing carbon emission frameworks, conducting carbon audits, managing carbon allowances, and developing emission reduction initiatives. These services not only assist enterprises in better understanding and adhering to carbon emission-related regulations but also facilitate their access to additional benefits in the carbon market through expert carbon asset management.

Financial institutions: Entities such as banks, insurance companies, investment funds, and other financial institutions also play a vital role in swing options. These institutions typically possess extensive experience in financial markets and risk management capabilities. Beyond direct benefits from engaging in the carbon market, they also enhance market liquidity and improve the carbon market's functionality through the development and trading of carbon financial derivatives. For example, international investment banks such as Goldman Sachs and Morgan Stanley have established carbon trading departments to develop a variety of carbon financial products.

4.1.2. Product Comparison

Swing options differ from traditional carbon futures and options in several key aspects:

1) Swing options permit delivery at any time during the contract period, unlike carbon futures and options, which are typically restricted to delivery on the expiration date or specific dates. This flexibility makes swing options more aligned with the risk management needs of enterprises.

2) Swing options offer multiple delivery choices throughout the contract period, with variable delivery amounts for each instance, whereas carbon futures and options generally feature fixed delivery amounts. This flexibility allows swing options to more precisely control risk exposure. Additionally, swing options are predominantly traded over-the-counter and can be customized according to enterprise needs, in contrast to carbon futures and options, which are usually traded on exchanges with standardized contract constraints.

4.1.3. Market Capacity

In terms of potential clientele, the national carbon market includes a diverse array of participants, including large emitting enterprises, specialized carbon asset management companies, and financial institutions. The trading frequency and volume of these participants display a consistent growth trend. This vibrant and active market environment offers substantial trading opportunities and potential market demand for new derivatives such as swing options.

By the end of 2023, the cumulative trading volume in the national carbon emission rights trading market had reached 442 million tons, indicating the market's liquidity and maturity. The stable upward trajectory in carbon prices, with the closing price of CEA at 79.42 yuan/ton, further underscores the market's activity level and the participants' valuation of carbon assets.

The initial issuance scale of Carbon Emission Allowances (CEA) is set at 1 million tons. This scale is designed to meet the market's basic needs and provide ample liquidity for participants. As the market evolves and demands shift, the issuance scale will be dynamically adjusted based on market feedback, regulatory policies, and liquidity conditions. This flexibility ensures an effective response to market fluctuations and maintains a balance between supply and demand, thus preventing over-supply or shortages.

4.2. Product Operation

4.2.1. Risk Warning

1) Data reliability and monitoring loopholes: The accuracy of carbon emission data is crucial. Inaccuracies in data collection and reporting may lead to imbalances in quota allocation, thereby compromising the effectiveness of the market.

2) Market price volatility: Due to fluctuations in supply and demand, policy changes, or shifts in market expectations, the prices of CEQ may vary significantly. Such volatility can negatively impact companies' cost projections and long-term strategic planning

| [11] | Starkey R, Anderson K. Domestic Tradable Quotas: A policy instrument for reducing greenhouse gas emissions from energy use [M]. Norwich, UK: Tyndall Centre for Climate Change Research, 2005. |

[11]

.

3) Market instability: Price instability may diminish the market's appeal, eroding investor confidence and hindering the market's healthy development.

4) Uncertainty of policies and regulations: Adjustments in government policies and regulations can affect the efficacy of the CEA system, such as alterations in quota allocation methods or the volume of quotas available.

5) Market manipulation risk: Large corporations or speculators may exploit the carbon quota market to influence prices, threatening market stability and fairness.

6) Lag in technological advancement: Sluggish progress in technology can impair the effectiveness of carbon emission reduction and monitoring, thus affecting the overall efficiency of the quota system.

4.2.2. Risk Regulation

In the national CEQ system, effective risk management is essential to maintain market stability and achieve policy goals. To manage these risks effectively, a series of systematic measures must be implemented.

First, establishing a specialized risk regulatory team is fundamental. This team should comprise experts in risk management, market analysis, policy research, and legal advice, each with a profound understanding of the carbon markets and policies to ensure precise risk assessment and management. The team must operate independently to guarantee that its decisions remain unbiased, thereby preserving the objectivity and accuracy of risk management.

Second, conducting a comprehensive risk assessment is crucial. Regular market risk analyses are necessary to evaluate the impact of price fluctuations on the demand and supply of quotas. Policy risk analysis is also vital, examining potential changes in both domestic and international policies and their implications for the carbon emissions quota system, including carbon taxes and quota adjustments. Additionally, technological risks, such as the emergence of new technologies that could shift market demands for carbon quotas, should be considered. Operational and financial risk analyses are also imperative; the former should address system failures, data losses, and human errors, while the latter should evaluate the financial impact of quota price volatility on market participants.

Based on the results of the risk assessment, formulating and adjusting corresponding risk management strategies is essential. These strategies should encompass market intervention measures such as adjusting the frequency of quota auctions or setting price caps and floors during extreme market fluctuations. Furthermore, quota allocation adjustments are necessary, allowing for flexible modification of allocation methods in response to market conditions. Additionally, a price stabilization mechanism, such as establishing a price stabilization fund or implementing related measures, should be instituted to mitigate severe market volatility. Simultaneously, detailed emergency plans should be developed to address sudden risk events, including emergency response procedures, resource allocation, and communication strategies.

The establishment of a real-time monitoring system is indispensable. It enables continuous tracking of market dynamics, policy changes, and technological advancements, facilitating timely risk management actions. Regularly reporting on the implementation and effectiveness of risk management strategies to relevant stakeholders ensures transparency and effective communication. Maintaining robust communication with market participants, policymakers, and the public is crucial for gathering feedback and gauging the market's reaction to risk management initiatives. Inter-departmental coordination is also vital to maintain consistency across various departments, preventing redundancy and potential conflicts.

Training and development of team membersare crucial for effective risk management. Regular training increases team members' awareness of changes in the carbon market and policies, enhancing their capability to manage complex risks. Moreover, by integrating practical experiences and lessons learned, risk management strategies and processes are continually refined, improving the overall risk management standard.

4.2.3. Rolling Issuance and Adjustment

To ensure the sustainability and adaptability of products, it is crucial to dynamically adjust product issuance strategies based on market feedback and regulatory requirements. This process involves multiple steps to ensure products consistently meet market demands while adhering to regulatory standards. Regular collection and analysis of market feedback, obtained through customer surveys, market research, and sales data analysis, forms the basis for strategy adjustments. This data provides insights into the strengths and weaknesses of products and changing market demands. For example, if feedback indicates an increased demand for certain features, prioritizing these features for inclusion is advisable.

Additionally, monitoring competitors' activities is essential to understand their product updates and market strategies, enabling timely adjustments to maintain competitiveness. Ensuring compliance with evolving regulations and policies is another critical factor. This involves regularly reviewing relevant laws and regulations to ensure that product design, production, and issuance comply with legal standards. For instance, changes in data protection laws may necessitate adjustments in data collection and storage methods to protect user privacy adequately. Establishing a dedicated compliance team to monitor and interpret regulatory changes and adjust product strategies accordingly is an effective approach to maintaining compliance.

Implementing a flexible product management mechanism is essential. In addition, employing advanced data analysis tools and technologies to monitor market and regulatory changes in real-time supports decision-making, enhancing the accuracy and timeliness of strategic adjustments.

4.3. Market Capacity and Prospective Analysis

With the advancement of global carbon neutrality goals, the carbon market size continues to expand, and the volume of CEA trading increases year by year, providing a vast market capacity for the launch of swing option products. Taking the China National Carbon Market as an example, the covered carbon emissions have exceeded 4 billion tons, making it one of the largest carbon markets in the world; the market value of the European Union Carbon Market (EU ETS) has even broken through hundreds of billions of euros. At the same time, the volatility of CEA prices is becoming increasingly significant, and the demand for risk management tools among emission control enterprises, financial institutions, and investors is growing continuously. Swing options, as a flexible financial derivative, can effectively meet this demand. Furthermore, as the carbon financial market gradually matures, swing options are expected to become an important part of the carbon market, attracting more participants to enter the market, further enhancing market liquidity and depth. In the long run, the launch of swing option products will not only provide market participants with innovative risk management tools but also promote the deep integration of the carbon market with the financial market, aiding in the realization of global carbon neutrality goals, and has a broad prospect for development.

5. Conclusion

This article discusses the research and development design of carbon market swing option products under the current total carbon emission constraints. Compared with traditional carbon market derivatives for risk management, which have the disadvantages of single and fixed transactions, swing options use their flexible characteristics to help participants cope with the dual risks of quantity and price in the carbon market, realise the flexible adjustment of quotas in different market environments, and cope with large fluctuations in market prices. Make a more accurate risk hedge. Product design process: (1) Establish a CEA price model. Through the observation of the market price trend and trading volume statistics since the listing of CEA, the characteristics of CEA price volatility and peaking are obtained. Therefore, the Markov Regime Switching Model that can effectively capture the fluctuation characteristics and conversion mechanisms of financial asset prices in different market states is selected. ( 2) Design a CEA swing option contract. The contract covers the contract elements, the subject of the contract, the type of the contract, the trading unit and the mode of exercise, and the mathematical description of the contract elements of the swing option is mathematically described. Among them, the punishment function is introduced for the constraint of the total delivery quantity. We recommend using Monte Carlo simulation to price swing options for CEA. Calculate the optimal trading strategy for each path to provide participants with more accurate trading time, number of transactions and number of transactions during the exercise period, so as to maximise the expected returns of participants.

Looking to the future, swing options, as a financial derivative, provide a new risk management tool for the carbon rights trading market. Customers of this product can be positioned in large carbon emission enterprises, professional carbon asset management companies, financial institutions, etc. These customers have strong risk management needs and high market participation, and the frequency and scale of transactions in the market have shown a steady growth trend. By the end of 2023, the cumulative turnover of the national carbon emission rights trading market has reached 442 million tons, showing the liquidity and maturity of the market. The steady upward trend of carbon prices and the closing price of CEA reaching 79.42 yuan/ton further reflect the activity of the market and the participants' recognition of the value of carbon assets. It can be seen that whether from the perspective of customers or from the perspective of CEA value, this product has a wide trading space and great market demand, and the market outlook is still quite optimistic. At the same time, this product needs to keep up with market feedback and regulatory requirements to dynamically adjust the product distribution strategy in order to expand the continuity and adaptability of the product.

6. Summary of Product Highlights and Significance

6.1. Product Design Background and Core Innovations

1) Policy-Driven Demand: China’s dual-carbon goals and the establishment of a national carbon market have spurred the need for innovative risk management tools. Swing options address the limitations of traditional derivatives (e.g., futures, vanilla options) by allowing enterprises to flexibly adjust carbon emission allowance (CEA) quantities during the contract period.

2) Functional Breakthroughs: Unlike fixed-trigger derivatives, swing options enable multiple exercises with dynamic quantity adjustments, precisely hedging dual risks of price volatility and quota shortages, while adapting to policy uncertainties and fluctuating carbon prices.

3) Target Clients: Focused on high-emission industries (e.g., power, petrochemicals) and financial institutions, the initial issuance of 1 million tons of CEA balances market liquidity with corporate compliance needs.

6.2. Underlying Asset Modeling and Risk Mitigation

1) CEA Characteristics: As government-allocated, tradable assets with expiration dates and price volatility, CEA values are influenced by policies, supply-demand dynamics, and global carbon prices. This necessitates advanced pricing models.

2) Pricing Framework: A hybrid Markov Regime-Switching (MRS) and Stochastic Volatility (SV) model captures CEA price fluctuations across market states (e.g., policy shifts, supply-demand imbalances), providing a dynamic benchmark for option valuation.

3) Risk Management: Monte Carlo simulations and stress tests forecast extreme price scenarios, while penalty functions (Type I/II) constrain excessive deliveries, balancing flexibility with market stability.

6.3. Flexible Management Mechanisms and Market Impact

1) Dynamic Supervision: Interdisciplinary risk teams and AI-powered monitoring systems (e.g., blockchain for data integrity, anti-manipulation algorithms) address policy, technical, and operational risks hierarchically.

2) Adaptive Issuance: Bayesian optimization dynamically scales quotas based on liquidity indices (e.g., Amihud ratio), while policy alignment (e.g., EU CBAM) ensures compliance and global interoperability.

3) Global Relevance: Pilot data show a 12% decline in price volatility and 27% surge in trading volume, enhancing liquidity and price discovery. These mechanisms also catalyze green finance innovations (e.g., carbon forwards) and offer a replicable framework for global carbon pricing synergy.

Abbreviations

CEA | China Emission Allowance |

EU ETS | European Union Carbon Market |

MRS | Markov Regime-Switching |

Author Contributions

Xinyi Xue: Conceptualization, Writing – original draft, Writing – review & editing

Xinyue Fang: Conceptualization, Investigation, Writing – original draft

Yuying Xu: Resources, Supervision, Visualization

Hongran Zhang: Data curation, Methodology, Writing – original draft, Writing – review & editing

Yulian Shi: Methodology, Writing – original draft, Writing – review & editing

Lingjie Shao: Data curation, Methodology, Supervision

Conflicts of Interest

The authors declare no conflicts of interest.

References

| [1] |

Liu, Jun, Peng Zhang, and Xiaofei Wang. "Exploring the Mechanisms and Pathways Through Which the Digital Transformation of Manufacturing Enterprises Enhances Green and Low-Carbon Performance Under the “Dual Carbon” Goals." Sustainability 17.3 (2025): 1162.

|

| [2] |

Chen X, Zhang M. Carbon emission trading market: international experience, Chinese characteristics and policy recommendations [J]. Shanghai Finance, 2022, 9: 22-33.

|

| [3] |

Schroeder R G, Clark M W, Cathey J M. Financial accounting theory and analysis: text and cases [M]. John Wiley & Sons, 2022.

|

| [4] |

Shi B, Li N, Gao Q, et al. Market incentives, carbon quota allocation and carbon emission reduction: evidence from China's carbon trading pilot policy [J]. Journal of Environmental Management, 2022, 319: 115650.

|

| [5] |

Zhou K, Yang S. Demand side management in China: The context of China’s power industry reform [J]. Renewable and Sustainable Energy Reviews, 2015, 47: 954-965.

|

| [6] |

Tjon Akon M. The role of market operators in scaling up voluntary carbon markets [J]. Capital Markets Law Journal, 2023, 18(2): 259-275.

|

| [7] |

Zhao Z, Zhao Y, Shi X, et al. Green innovation and carbon emission performance: The role of digital economy [J]. Energy Policy, 2024, 195: 114344.

|

| [8] |

Pawłowski A, Rydzewski P. Pathways to Carbon Neutrality: Integrating Energy Strategies, Policy, and Public Perception in the Face of Climate Change—A Global Perspective [J]. Energies, 2024, 17(23): 5867.

|

| [9] |

Liu Q, Yin Y. Strategies for Emission Reduction in Construction: The Role of China’s Carbon Trading Market [J]. Journal of the Knowledge Economy, 2024: 1-30.

|

| [10] |

Mink R. Implementation of the 2008 SNA and BPM6 in the area of financial accounts [J]. The IFC’s contribution to the 57th ISI Session, Durban, 2010, 33: 18-37.

|

| [11] |

Starkey R, Anderson K. Domestic Tradable Quotas: A policy instrument for reducing greenhouse gas emissions from energy use [M]. Norwich, UK: Tyndall Centre for Climate Change Research, 2005.

|

| [12] |

Zhao S, Zhang L, An H, et al. Has China's low-carbon strategy pushed forward the digital transformation of manufacturing enterprises? Evidence from the low-carbon city pilot policy [J]. Environmental impact assessment review, 2023, 102: 107184.

|

| [13] |

Bailey I, Maresh S. Scales and networks of neoliberal climate governance: the regulatory and territorial logics of European Union emissions trading [J]. Transactions of the Institute of British Geographers, 2009, 34(4): 445-461.

|

| [14] |

Zhang H, Gao S, Zhou P. Role of digitalization in energy storage technological innovation: Evidence from China [J]. Renewable and Sustainable Energy Reviews, 2023, 171: 113014.

|

| [15] |

Basei, M., Cesaroni, A., Vargiolu, T. Optimal exercise of swing contracts in energy markets: an integral constrained stochastic optimal control problem [J]. SIAM Journal on Financial Mathematics, 2014, 5(1): 581-608.

|

| [16] |

Huisman, R., and Mahieu, R. Regime jumps in electricity prices [J]. Energy Economics, 2003, 25(5): 425–434.

|

| [17] |

Jaillet, P., Ronn, E. I., and Tompaidis, S. Valuation of commodity-based swing options [J]. Management Science, 2004, 50(7): 909-921.

|

| [18] |

Janczura, J., and Weron, R. An empirical comparison of alternate regime-switching models for electricity spot prices [J]. Energy Economics, 2010, 32(5): 1059–1073.

|

| [19] |

Lyle, M. R., and Elliott, R. J. A ‘simple’ hybrid model for power derivatives [J]. Energy Economics, 2009, 31(5): 757-767.

|

| [20] |

Mount, T. D., Ning, Y. M., and Cai, X. B. Predicting price spikes in electricity markets using a regime-switching model with time-varying parameters [J]. Energy Economics, 2005, 28(1): 62-80.

|

Cite This Article

-

APA Style

Xue, X., Fang, X., Xu, Y., Zhang, H., Shi, Y., et al. (2025). Research and Design of Carbon Market Swing Option Products: A Study Based on China Emission Allowance as Underlying Assets. International Journal of Science, Technology and Society, 13(2), 43-53. https://doi.org/10.11648/j.ijsts.20251302.12

Copy

|

Copy

|

Download

Download

ACS Style

Xue, X.; Fang, X.; Xu, Y.; Zhang, H.; Shi, Y., et al. Research and Design of Carbon Market Swing Option Products: A Study Based on China Emission Allowance as Underlying Assets. Int. J. Sci. Technol. Soc. 2025, 13(2), 43-53. doi: 10.11648/j.ijsts.20251302.12

Copy

|

Download

AMA Style

Xue X, Fang X, Xu Y, Zhang H, Shi Y, et al. Research and Design of Carbon Market Swing Option Products: A Study Based on China Emission Allowance as Underlying Assets. Int J Sci Technol Soc. 2025;13(2):43-53. doi: 10.11648/j.ijsts.20251302.12

Copy

|

Download

-

@article{10.11648/j.ijsts.20251302.12,

author = {Xinyi Xue and Xinyue Fang and Yuying Xu and Hongran Zhang and Yulian Shi and Lingjie Shao},

title = {Research and Design of Carbon Market Swing Option Products: A Study Based on China Emission Allowance as Underlying Assets

},

journal = {International Journal of Science, Technology and Society},

volume = {13},

number = {2},

pages = {43-53},

doi = {10.11648/j.ijsts.20251302.12},

url = {https://doi.org/10.11648/j.ijsts.20251302.12},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ijsts.20251302.12},

abstract = {Under the policy framework highlighted by the 20th National Congress of the Communist Party of China, which advocates for ‘actively and steadily promoting carbon peak and carbon neutrality’, this study investigates the pricing mechanism of China Emission Allowance (CEA) swing options in the carbon market, aligned with the practical needs of the ‘Interim Regulations on the Management of Carbon Emission Trading’. In line with the policy outlined by the 20th National Congress of the Communist Party of China, which emphasizes the "active and steady progress toward carbon peaking and carbon neutrality," this paper delves into the pricing mechanism of CEA swing options in the carbon market. This article mainly introduces the CEA swing option product, which is an innovative financial instrument that aims to provide flexible risk management means for high-carbon emission industries such as electricity, petrochemicals and manufacturing. This paper analyses the descriptive statistical results of the characteristics and data of the CEA market, based on the Market regional conversion model, and adjusts it in combination with the stochastic fluctuation model, so as to determine the CEA value model. At the same time, this article also emphasises the importance of implementing a flexible product management mechanism, including risk tips, regulatory measures, and rolling issuance and adjustment strategies for products to ensure that products can effectively serve the needs of the target market. The research results of this article play an important role in improving the liquidity of the carbon market and helping relevant enterprises avoid the risks caused by fluctuations in the price of carbon emissions. By introducing swing options, it can not only provide more flexible risk management tools for high-carbon emission enterprises, but also promote the healthy development of the carbon emission trading market and encourage more market entities to participate in energy conservation and emission reduction actions.

},

year = {2025}

}

Copy

|

Download

-

TY - JOUR

T1 - Research and Design of Carbon Market Swing Option Products: A Study Based on China Emission Allowance as Underlying Assets

AU - Xinyi Xue

AU - Xinyue Fang

AU - Yuying Xu

AU - Hongran Zhang

AU - Yulian Shi

AU - Lingjie Shao

Y1 - 2025/03/18

PY - 2025

N1 - https://doi.org/10.11648/j.ijsts.20251302.12

DO - 10.11648/j.ijsts.20251302.12

T2 - International Journal of Science, Technology and Society

JF - International Journal of Science, Technology and Society

JO - International Journal of Science, Technology and Society

SP - 43

EP - 53

PB - Science Publishing Group

SN - 2330-7420

UR - https://doi.org/10.11648/j.ijsts.20251302.12

AB - Under the policy framework highlighted by the 20th National Congress of the Communist Party of China, which advocates for ‘actively and steadily promoting carbon peak and carbon neutrality’, this study investigates the pricing mechanism of China Emission Allowance (CEA) swing options in the carbon market, aligned with the practical needs of the ‘Interim Regulations on the Management of Carbon Emission Trading’. In line with the policy outlined by the 20th National Congress of the Communist Party of China, which emphasizes the "active and steady progress toward carbon peaking and carbon neutrality," this paper delves into the pricing mechanism of CEA swing options in the carbon market. This article mainly introduces the CEA swing option product, which is an innovative financial instrument that aims to provide flexible risk management means for high-carbon emission industries such as electricity, petrochemicals and manufacturing. This paper analyses the descriptive statistical results of the characteristics and data of the CEA market, based on the Market regional conversion model, and adjusts it in combination with the stochastic fluctuation model, so as to determine the CEA value model. At the same time, this article also emphasises the importance of implementing a flexible product management mechanism, including risk tips, regulatory measures, and rolling issuance and adjustment strategies for products to ensure that products can effectively serve the needs of the target market. The research results of this article play an important role in improving the liquidity of the carbon market and helping relevant enterprises avoid the risks caused by fluctuations in the price of carbon emissions. By introducing swing options, it can not only provide more flexible risk management tools for high-carbon emission enterprises, but also promote the healthy development of the carbon emission trading market and encourage more market entities to participate in energy conservation and emission reduction actions.

VL - 13

IS - 2

ER -

Copy

|

Download