The main objective of this study was to examine the effects of dynamic capability (DC) on bank performance (BP), mediated by multichannel integration quality (MCIQ) in the case of the Commercial Bank of Ethiopia (CBE), Ambo District. The study employed an explanatory sequential QUAN-qual design, a mixed-methods approach that begins with a quantitative phase to identify patterns and relationships, followed by a qualitative phase to provide deeper insights and explanations for the initial findings. Primary data were collected from 235 bank employees using simple random sampling to ensure representation across branches. The data were gathered through a standardized questionnaire and analyzed using AMOS version 23 and SPSS version 25, applying structural equation modeling to test the hypothesized relationships. The results revealed that both DC and MCIQ have significant positive effects on BP. Additionally, the effect of DC on BP was found to be partially mediated by MCIQ. The study contributes to existing literature by providing empirical evidence on the role of DC and MCIQ in enhancing bank performance. Based on these findings, it is recommended that practitioners and decision-makers focus on developing dynamic capabilities and enhancing multichannel integration quality to achieve sustainable performance. Future research could explore other mediating or moderating factors, and extend the study to other sectors or countries to improve generalizability.

| Published in | International Journal of Science and Qualitative Analysis (Volume 11, Issue 2) |

| DOI | 10.11648/j.ijsqa.20251102.11 |

| Page(s) | 39-56 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2025. Published by Science Publishing Group |

Dynamic Capability, Multichannel Integration Quality, Firm Performance

Main variables | Sub-measures | Items | Likert Scale | Sources |

|---|---|---|---|---|

Dynamic Capability | SC | five | 1 to 5 | [44-46] |

SZC | five | 1 to 5 | ||

RC | five | 1 to 5 | ||

Multichannel integration Quality | CSC | five | 1 to 5 | [44, 45, 47, 48] |

CCC | five | 1 to 5 | ||

CPC | five | 1 to 5 | ||

AQ | five | 1 to 5 | ||

Bank Performance | FP | five | 1 to 5 | [49] |

MP | five | 1 to 5 |

Main Variables | Mean | Std. Deviation | |

|---|---|---|---|

Bank Performance | 2.99 | .45 | |

Multichannel Integration Quality | 2.39 | .32 | |

Dynamic Capability | 3.21 | .64 | |

Sub-dimensions | |||

BP | Non-financial performance | 3.49 | .71 |

Financial performance | 3.53 | .66 | |

MCIQ | Assurance quality | 3.50 | .62 |

Channel process consistency | 3.40 | .62 | |

Channel content consistency | 3.66 | .64 | |

Channel service configuration | 3.72 | .63 | |

DC | Reconfiguration capability | 3.65 | .85 |

Seizing capability | 3.68 | .86 | |

Sensing capability | 3.65 | .89 | |

Main Variables | Factor Loading | Sub-dimensions | Factor Loading | Items | Reliability |

|---|---|---|---|---|---|

Dynamic Capability | .895 | --> sc | .991 | --> sc5 | .992 |

.978 | --> sc4 | ||||

.961 | --> sc3 | ||||

.988 | --> sc2 | ||||

.982 | --> sc1 | ||||

.809 | -->szc | .976 | --> szc5 | .994 | |

.968 | --> szc4 | ||||

.992 | --> szc3 | ||||

.995 | --> szc2 | ||||

.990 | --> szc1 | ||||

.792 | -->rc | .996 | --> rc5 | .961 | |

.988 | --> rc4 | ||||

.997 | --> rc3 | ||||

.990 | --> rc2 | ||||

.998 | --> rc1 | ||||

Multichannel Integration Quality | .780 | -->csc | .991 | --> csc5 | .993 |

.998 | --> csc4 | ||||

.956 | --> csc3 | ||||

.990 | --> csc2 | ||||

.971 | --> csc1 | ||||

.818 | -->cc | .954 | --> cc5 | .978 | |

.958 | --> cc4 | ||||

.942 | --> cc3 | ||||

.948 | --> cc2 | ||||

.936 | --> cc1 | ||||

.647 | -->pc | .953 | --> pc5 | .991 | |

.963 | --> pc4 | ||||

.986 | --> pc3 | ||||

.995 | --> pc2 | ||||

.995 | --> pc1 | ||||

.570 | -->aq | .964 | --> aq5 | .989 | |

.933 | --> aq4 | ||||

.993 | --> aq3 | ||||

.992 | --> aq2 | ||||

.980 | --> aq1 | ||||

.981 | --> td4 | ||||

.975 | --> td3 | ||||

.965 | --> td2 | ||||

.978 | --> td1 | ||||

Bank Performance | .797 | -->fp | .981 | --> fp5 | .996 |

.995 | --> fp4 | ||||

.990 | --> fp3 | ||||

.897 | --> fp2 | ||||

.980 | --> fp1 | ||||

.727 | -->mp | .959 | --> mp5 | .982 | |

.973 | --> mp4 | ||||

.951 | --> mp3 | ||||

.971 | --> mp2 | ||||

.940 | --> mp1 |

Main Variables | CR | AVE | DC | MCIQ | BP |

|---|---|---|---|---|---|

Dynamic Capability | 0.872 | 0.694 | 0.833 | ||

Multichannel Integration Quality | 0.799 | 0.505 | 0.389 | 0.710 | |

Bank Performance | 0.739 | 0.588 | 0.395 | 0.396 | 0.767 |

Sub-dimensions | CR | AVE | Sc | szc | rc | csc | cc | pc | aq | fp | mp |

|---|---|---|---|---|---|---|---|---|---|---|---|

sc | 0.992 | 0.961 | 0.980 | ||||||||

szc | 0.994 | 0.969 | 0.721 | 0.984 | |||||||

rc | 0.997 | 0.987 | 0.710 | 0.64 | 0.994 | ||||||

csc | 0.992 | 0.963 | 0.264 | 0.212 | 0.244 | 0.981 | |||||

cc | 0.978 | 0.898 | 0.293 | 0.258 | 0.254 | 0.66 | 0.948 | ||||

pc | 0.991 | 0.957 | 0.218 | 0.199 | 0.234 | 0.481 | 0.522 | 0.978 | |||

aq | 0.989 | 0.946 | 0.202 | 0.235 | 0.151 | 0.434 | 0.423 | 0.438 | 0.973 | ||

fp | 0.996 | 0.979 | 0.291 | 0.246 | 0.191 | 0.288 | 0.263 | 0.229 | 0.216 | 0.989 | |

mp | 0.983 | 0.919 | 0.285 | 0.263 | 0.204 | 0.184 | 0.200 | 0.088 | 0.212 | 0.580 | 0.959 |

Measure | Estimate | Threshold | Interpretation |

|---|---|---|---|

CMIN/DF | 2.220 | Between 1 and 3 | Excellent |

CFI | 0.958 | >0.95 | Excellent |

SRMR | 0.038 | <0.08 | Excellent |

RMSEA | 0.072 | <0.06 | Acceptable |

Hypothesis | Path | Estimate | LL | UL | P-value | Support |

|---|---|---|---|---|---|---|

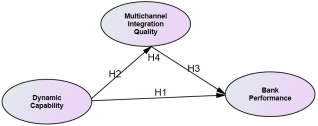

H1 | DC → BP | 0.27 | 0.045 | 0.428 | 0.018 | Supported |

H2 | DC → MCIQ | 0.39 | 0.206 | 0.535 | 0.008 | Supported |

H3 | MCIQ → BP | 0.30 | 0.095 | 0.473 | 0.016 | Supported |

H4 | DC → MCIQ → BP | 0.12 | 0.037 | 0.208 | 0.015 | Supported |

Total Effects | DC → BP (Direct + Indirect) | 0.387 | 0.195 | 0.528 | 0.007 | Supported |

Step | Activities |

|---|---|

1. Familiarization with Data | Interviews were carefully reviewed to understand the respondents' responses. |

2. Generating Initial Codes | Codes were generated based on the systematic literature review (SLR) defined measures: For DCs: sc, szc, and rc, for MCIQ: csc, pc, cc, and aq. |

3. Searching for Themes | The generated codes were grouped under pre-defined SLR themes across respondents' responses. |

4. Reviewing Themes | The themes were refined to ensure accuracy with respondents' feedback. |

5. Defining & Naming Themes | The themes were finalized: validated and refined. |

6. Writing the Report | The final report integrated with SLR-derived measures and respondents’ feedback, presenting insights for variables. |

Areas | Quantitative | Qualitative | Mixed Method | |

|---|---|---|---|---|

Introduction | Background | Focus on measurable relationships between variables. | Focus on in-depth exploration of the phenomenon. | Integrates both empirical and interpretative |

Research problem | Framed around gaps in empirical studies. | Focuses on gaps in understanding lived experiences. | Justifies the need for both quantitative and qualitative insights. | |

Hypotheses | Clearly defined hypotheses. | No hypotheses; open-ended research questions. | Includes for hypotheses quantitative and research questions for qualitative. | |

Objectives | Aim at hypothesis testing. | Emphasize deep insight into concepts. | Combine testing and exploration. | |

Research questions | Focus on statistical relationships. | No hypotheses; open-ended research questions. | common | |

Significance | Emphasizes numerical impact. | Emphasizes theoretical and practical contributions. | common | |

Literature Review | Theoretical framework | Built on empirical studies with statistical models. | Based on interpretive and conceptual models. | Integrates from both methodologies. |

Research gap | Focuses on lack of statistical clarity. | Focuses on conceptual limitations. | Highlights the lack of integrated perspectives. | |

Empirical review | Focuses on quantitative studies. | Emphasizes qualitative studies. | Discusses both quantitative and qualitative studies. |

Research Methodology | Research Approach | Deductive hypothesis testing. | Inductive theory building. | Combines both deductive (hypothesis testing) and inductive (exploratory) |

Philosophical Paradigm | Post-positivism. | Constructivism. | Pragmatic | |

Sample Size | Large sample size, | Small sample size | Combines both. | |

Sampling | Random and stratified sampling. | Purposive/saturation sampling. | Both used. | |

Data Collection | Structured questionnaire. | Interviews | Surveys (quantitative) + interviews (qualitative). | |

Data Analysis | SEM-AMOS | Thematic analysis. | Integrated analysis | |

Validity & Reliability | Cronbach’s alpha, CFA. | Credibility, dependability. | Validity through comparison of results. |

Measurement Model Analysis | Uses reliability testing, factor analysis, and SEM for construct validity. - Focus on model fit. | Not applicable (qualitative research doesn’t use measurement models). | Uses measurement models for QUAN and validates QUAL themes. Triangulation of findings |

|---|---|---|---|

Descriptive Analysis | Uses tables and graphs with mean, and standard deviation. | Describes respondents’ profiles with narrative summaries. | Integrates findings using a comparative approach. |

Structural Mediation Model Analysis | Uses SEM models to assess mediation effects. | Not applicable (qualitative research does not use SEM). | Uses SEM for QUAN mediation analysis. Integrated discussion of findings. |

Qualitative Data Analysis | Not applicable (quantitative research does not use qualitative data analysis). | Thematic analysis of interview transcripts using.key themes. | The 4 themes were analysed to support QUAN findings. |

Mixed Analysis | Purely quantitative. | Purely qualitative. | Integrates QUAN and qual findings. |

Summary, Conclusions, and Implications | Summarizes key statistical findings. | Summarizes key qualitative themes. | Provides integrated Summary, conclusions, and recommendations. |

DC | Dynamic Capability |

MCIQ | Multichannel Integration Quality |

BP | Bank Performance |

CBE | Commercial Bank of Ethiopia |

SEM | Structural Equation Modeling |

AMOS | Analysis of Moment Structures |

QUAN-qual | Quantitative-qualitative |

| [1] | Teece, “Business models and dynamic capabilities,” Long Range Plann., vol. 51, no. 1, pp. 40-49, 2018, |

| [2] | T. M. T. Hossain, “Integration quality dynamics in multichannel services marketing,” 2020, [Online]. Available: |

| [3] | R. Singh, P. Charan, and M. Chattopadhyay, “Dynamic capabilities and responsiveness: moderating effect of organization structures and environmental dynamism,” Decision, vol. 46, no. 4, pp. 301-319, 2019, |

| [4] | P. T. Nguyen, “The Impact of Banking Sector Development on Economic Growth: The Case of Vietnam’s Transitional Economy,” J. Risk Financ. Manag., vol. 15, no. 8, 2022, |

| [5] | D. J. Teece, G. Pisano, and A. Shuen, “Dynamic capabilities and strategic management,” Strateg. Manag. J., vol. 18, no. March, pp. 77-116, 1997, |

| [6] | S. Handoyo, H. Suharman, E. K. Ghani, and S. Soedarsono, “A business strategy, operational efficiency, ownership structure, and manufacturing performance: The moderating role of market uncertainty and competition intensity and its implication on open innovation,” J. Open Innov. Technol. Mark. Complex., vol. 9, no. 2, p. 100039, 2023, |

| [7] | L. C. C. Paez et al., “Dynamic capabilities configurations: the firm lifecycle and the interplay of DC dimensions,” Int. J. Entrep. Behav. Res., vol. 28, no. 4, pp. 910-934, 2022, |

| [8] | M. J. Janssen, C. Castaldi, and A. Alexiev, “Dynamic capabilities for service innovation: conceptualization and measurement,” R D Manag., vol. 46, no. 4, pp. 797-811, 2016, |

| [9] | P. C. Verhoef, P. K. Kannan, and J. J. Inman, “From Multi-Channel Retailing to Omni-Channel Retailing. Introduction to the Special Issue on Multi-Channel Retailing.,” J. Retail., vol. 91, no. 2, pp. 174-181, 2015, |

| [10] |

Y. Li, H. Liu, E. T. K. Lim, J. M. Goh, F. Yang, and M. K. O. Lee, “Customer’s reaction to cross-channel integration in omnichannel retailing: The mediating roles of retailer uncertainty, identity attractiveness, and switching costs,” Decis. Support Syst., 2018, [Online]. Available:

https://www.sciencedirect.com/science/article/pii/S0167923617302397 |

| [11] | Z. W. Y. Y. Lee et al., “Customer engagement through omnichannel retailing: The effects of channel integration quality,” Ind. Mark. Manag., vol. 77, no. October, pp. 90-101, 2019, |

| [12] | H. Wu, J. Chen, and H. Jiao, “Dynamic capabilities as a mediator linking international diversification and innovation performance of firms in an emerging economy,” J. Bus. Res., vol. 69, no. 8, pp. 2678-2686, 2016, |

| [13] | D. Ellström, J. Holtström, E. Berg, and C. Josefsson, “Dynamic capabilities for digital transformation,” J. Strateg. Manag., vol. 15, no. 2, pp. 272-286, 2022, |

| [14] | Y. Liu and G. Song, “Role of Logistics Integration Capability in Enhancing Performance in Omni-Channel Retailing: Supply Chain Integration as Mediator,” Sustain., vol. 15, no. 11, 2023, |

| [15] | L. Matysiak, A. M. Rugman, and A. Bausch, “Dynamic Capabilities of Multinational Enterprises: The Dominant Logics Behind Sensing, Seizing, and Transforming Matter!,” Manag. Int. Rev., vol. 58, no. 2, pp. 225-250, 2018, |

| [16] | A. Jantunen, A. Tarkiainen, S. Chari, and P. Oghazi, “Dynamic capabilities, operational changes, and performance outcomes in the media industry,” J. Bus. Res., vol. 89, no. June 2017, pp. 251-257, 2018, |

| [17] | M. (2019) Warner, K. S. R. and Wäger, “Building Dynamic Capabilities For Digital Transformation: An Ongoing Process Of Strategic Renewal,” vol. 52, no. February, pp. 326-349, 2019, |

| [18] | H. Shang, R. Chen, and Z. Li, “Dynamic sustainability capabilities and corporate sustainability performance: The mediating effect of resource management capabilities,” Sustain. Dev., vol. 28, no. 4, pp. 595-612, 2020, |

| [19] | F. Svahn and L. Mathiassen, “Embracing Digital Innovation in Incumbent Firms : How Volvo Cars Managed E Mbracing D Igital I Nnovation In I Ncumbent F Irms : H Ow V Olvo C Ars M Anaged C Ompeting C OncernS 1,” no. March, 2017, |

| [20] | O. Schilke, S. Hu, and C. E. Helfat, “Quo vadis, dynamic capabilities? A content-analytic review of the current state of knowledge and recommendations for future research,” Acad. Manag. Ann., vol. 12, no. 1, pp. 390-439, 2018, |

| [21] | A. Parasuraman, V. A. Zeithaml, and A. Malhotra, “E-S-QUAL a multiple-item scale for assessing electronic service quality,” J. Serv. Res., vol. 7, no. 3, pp. 213-233, 2005, |

| [22] | M. Banerjee, “Misalignment and Its Influence on Integration Quality in Multichannel Services,” J. Serv. Res., vol. 17, no. 4, pp. 460-474, 2014, |

| [23] | S. S. Zhou, A. J. Zhou, J. Feng, and S. Jiang, “Dynamic capabilities and organizational performance: The mediating role of innovation,” J. Manag. Organ., vol. 25, no. 5, pp. 731-747, 2019, |

| [24] | S. Shi, Y. Wang, X. Chen, and Q. Zhang, “Conceptualization of omnichannel customer experience and its impact on shopping intention: A mixed-method approach,” Int. J. Inf. Manage., vol. 50, no. February 2019, pp. 325-336, 2020, |

| [25] | Lee Zach, T. Chan, C. A. Yee-Loong, and Nottingham, “Customer engagement through omnichannel retailing: The effects of channel integration quality,” Ind. Mark. Manag., vol. 44, no. December 2018, pp. 0-32, 2019. |

| [26] | A. Hanelt, R. Bohnsack, D. Marz, and C. Antunes Marante, “A Systematic Review of the Literature on Digital Transformation: Insights and Implications for Strategy and Organizational Change,” J. Manag. Stud., vol. 58, no. 5, pp. 1159-1197, 2021, |

| [27] | T. M. T. Hossain, S. Akter, U. Kattiyapornpong, and Y. Dwivedi, “Reconceptualizing Integration Quality Dynamics for Omnichannel Marketing,” Ind. Mark. Manag., vol. 87, no. May, pp. 225-241, 2020, |

| [28] | D. Ellstr, J. Holtstr, E. Berg, and C. Josefsson, “Dynamic capabilities for digital transformation,” no. September 2021, 2024, |

| [29] | M. Ferasso, A. R. W. Takahashi, and M. R. May, “Dynamic capabilities, operational capabilities and SMEs performance: A synthesis of researches,” 26th Int. Assoc. Manag. Technol. Conf. IAMOT 2017, no. May, pp. 693-710, 2020. |

| [30] | C. E. Helfat and R. S. Raubitschek, “Dynamic and integrative capabilities for profiting from innovation in digital platform-based ecosystems,” Res. Policy, vol. 47, no. 8, pp. 1391-1399, 2018, |

| [31] | R. Cannas, “Exploring digital transformation and dynamic capabilities in agrifood SMEs,” J. Small Bus. Manag., vol. 00, no. 00, pp. 1-27, 2021, |

| [32] | L. Cao and L. Li, “Determinants of Retailers’ Cross-channel Integration: An Innovation Diffusion Perspective on Omni-channel Retailing,” J. Interact. Mark., vol. 44, pp. 1-16, 2018, |

| [33] | A. Buallay, “Is sustainability reporting (ESG) associated with performance? Evidence from the European banking sector,” Manag. Environ. Qual. An Int. J., vol. 30, no. 1, pp. 98-115, 2019, |

| [34] | L. Gao, I. Melero, and F. J. Sese, “Multichannel integration along the customer journey: a systematic review and research agenda,” Serv. Ind. J., vol. 40, no. 15, pp. 1087-1118, 2020, |

| [35] | A. F. Hayes and N. J. Rockwood, “Conditional Process Analysis: Concepts, Computation, and Advances in the Modeling of the Contingencies of Mechanisms,” Am. Behav. Sci., vol. 64, no. 1, pp. 19-54, 2020, |

| [36] | M. F. Sorkun, “Omni-channel capability and customer satisfaction : mediating roles of flexibility and operational logistics service quality,” vol. 48, no. 6, pp. 629-648, 2020, |

| [37] | T. M. T. Hossain et al., “Reconceptualizing Integration Quality Dynamics for Omnichannel Marketing,” Ind. Mark. Manag., vol. 87, no. May, pp. 225-241, 2020, |

| [38] | R. CBE, “Annual Report CBE,” Annu. Rep. CBE, vol. 7, no. November, pp. 14-25, 2023. |

| [39] | J. W. Creswell and C. N. Poth, “Philosophical, paradigm, and interpretive frameworks,” Qual. Inq. Res. Des. Choos. among five Tradit., pp. 15-30, 2018. |

| [40] | M. Saunders, P. Lewis, and A. Thornhill, Reserch Methods for business students fifth edition. 2019. |

| [41] |

K. M. Eisenhardt and J. A. Martin, “Dynamic capabilities: What are they?,” Strateg. Manag. J., vol. 21, no. 10-11, pp. 1105-1121, 2000,

https://doi.org/10.1002/1097-0266(200010/11)21:10/11<1105::AID-SMJ133>3.0.CO;2-E |

| [42] | J. W. R. Creswell, Research design : qualitative, quantitative, and mixed methods approaches / John W. Creswell. — 4th ed. 2014. |

| [43] | Cochran, “The Estimation of Sample Size in Experiments: II. Using Comparisons of Proportions,” J. Dent. Res., vol. 32, no. 5, pp. 606-612, 1977, |

| [44] | E. Danneels, “Survey Measures Of First- And Second-Order Competences,” Strateg. Manag. J., vol. 920, no. October, pp. 1-43, 2015, |

| [45] | V. Cataltepe, R. Kamasak, F. Bulutlar, and D. P. Alkan, “Dynamic and marketing capabilities as determinants of fi rm performance : evidence from automotive industry,” 2021, |

| [46] | M. A. Shafia, S. Shavvalpour, M. Hosseini, and R. Hosseini, “Mediating effect of technological innovation capabilities between dynamic capabilities and competitiveness of research and technology organisations,” Technol. Anal. Strateg. Manag., vol. 28, no. 7, pp. 811-826, 2016, |

| [47] | T. M. T. Hossain, S. Akter, U. Kattiyapornpong, and Y. K. Dwivedi, “Multichannel integration quality: A systematic review and agenda for future research,” J. Retail. Consum. Serv., vol. 49, no. January, pp. 154-163, 2019, |

| [48] | X. L. Shen, Y. J. Li, Y. Sun, and N. Wang, “Channel integration quality, perceived fluency and omnichannel service usage: The moderating roles of internal and external usage experience,” Decis. Support Syst., vol. 109, no. 2017, pp. 61-73, 2018, |

| [49] | A. Pezeshkan, S. Fainshmidt, A. Nair, M. L. Frazier, and E. Markowski, “An empirical assessment of the dynamic capabilities - performance relationship,” J. Bus. Res., 2015, |

| [50] | V. Braun and V. Clarke, “Using thematic analysis in psychology,” Qual. Res. Psychol., vol. 3, no. 2, pp. 77-101, 2006, |

| [51] | S. Moosavi, S. M., & Ghassabian, “We are IntechOpen, the first native scientific publisher of Open Access books TOP 1% Nutritional Value of Soybean Meal,” Web Sci., pp. 109-127, 2018. |

| [52] | N. V. Ivankova, J. W. Creswell, and S. L. Stick, “Using Mixed-Methods Sequential Explanatory Design: From Theory to Practice,” Field methods, vol. 18, no. 1, pp. 3-20, 2006, |

| [53] | S. K. Ahmed, “Journal of Medicine, Surgery, and Public Health,” J. Med. Surgery, Public Heal., vol. 2, no. January, pp. 0-3, 2024, |

| [54] | P. Akhtar, S. Ullah, S. H. Amin, G. Kabra, and S. Shaw, “Dynamic capabilities and environmental sustainability for emerging economies’ multinational enterprises,” Int. Stud. Manag. Organ., vol. 50, no. 1, pp. 27-42, 2020, |

| [55] | P. Mikalef, M. Boura, G. Lekakos, and J. Krogstie, “Big Data Analytics Capabilities and Innovation : The Mediating Role of Dynamic Capabilities and Moderating Effect of the Environment,” vol. 30, no. 2019, pp. 272-298, 2020, |

| [56] | S. Akter, M. S. Hossain, S. Q. Lu, S. Aditya, T. M. T. Hossain, and U. Kattiyapornpong, “Does Service Quality Perception in Omnichannel Retailing Matter? A Systematic Review and Agenda for Future Research,” Springer eBooks, pp. 71-97, 2019, |

| [57] | M. H. Al Dhaheri, S. Z. Ahmad, and A. Papastathopoulos, “Do environmental turbulence, dynamic capabilities, and artificial intelligence force SMEs to be innovative?,” J. Innov. Knowl., vol. 9, no. 3, p. 100528, 2024, |

| [58] | D. yuan Li et al., “Dynamic capabilities, environmental dynamism, and competitive advantage: Evidence from China,” J. Bus. Res., vol. 67, no. 1, pp. 2793-2799, 2014, |

| [59] | M. Rashidirad and H. Salimian, “SMEs’ dynamic capabilities and value creation: the mediating role of competitive strategy,” Eur. Bus. Rev., vol. 32, no. 4, pp. 591-613, 2020, |

| [60] | S. Cheng, Q. Fan, and M. Huang, “Strategic Orientation, Dynamic Capabilities, and Digital Transformation of Commercial Banks: A Fuzzy-Set QCA Approach,” Sustain., vol. 15, no. 3, pp. 1-19, 2023, |

| [61] | S. Y. Kuo, P. C. Lin, and C. S. Lu, “The effects of dynamic capabilities, service capabilities, competitive advantage, and organizational performance in container shipping,” Transp. Res. Part A Policy Pract., vol. 95, pp. 356-371, 2017, |

| [62] | S. H. Bhatti, A. Ahmed, A. Ferraris, W. M. Hirwani Wan Hussain, and S. F. Wamba, “Big data analytics capabilities and MSME innovation and performance: A double mediation model of digital platform and network capabilities,” Ann. Oper. Res., 2022, |

| [63] | A. Čirjevskis, “The role of dynamic capabilities as drivers of business model innovation in mergers and acquisitions of technology-advanced firms,” J. Open Innov. Technol. Mark. Complex., vol. 5, no. 1, 2019, |

| [64] | B. Il Park and S. S. Xiao, “Is exploring dynamic capabilities important for the performance of emerging market firms? The moderating effects of entrepreneurial orientation and environmental dynamism,” Int. Stud. Manag. Organ., vol. 50, no. 1, pp. 57-73, 2020, |

| [65] | R. Sousa and C. Voss, “The impacts of e-service quality on customer behaviour in multi-channel e-services,” Total Qual. Manag. Bus. Excell., vol. 23, no. 7-8, pp. 789-806, 2012, |

| [66] |

T. M. T. Hossain, S. Akter, U. Kattiyapornpong, and..., “Reconceptualizing integration quality dynamics for omnichannel marketing,” Ind. Mark. …, 2020, [Online]. Available:

https://www.sciencedirect.com/science/article/pii/S0019850119304869 |

| [67] | D. Kolbe, H. Calderón, and M. Frasquet, “Multichannel integration through innovation capability in manufacturing SMEs and its impact on performance,” J. Bus. Ind. Mark., vol. 37, no. 1, pp. 115-127, 2021, |

| [68] | T. Yeğin and M. Ikram, “Developing a Sustainable Omnichannel Strategic Framework toward Circular Revolution: An Integrated Approach,” Sustainability, 2022, [Online]. Available: |

| [69] | L. Bin Oh et al., “The effects of retail channel integration through the use of information technologies on firm performance,” J. Oper. Manag., vol. 30, no. 5, pp. 368-381, 2012, |

APA Style

Etana, N. G., Kero, C. A., Getahun, M. (2025). The Effect of Dynamic Capability and Multichannel Integration Quality on Bank Performance in Case of Commercial Bank of Ethiopia: Application of Sequential QUAN-qual Explanatory Design. International Journal of Science and Qualitative Analysis, 11(2), 39-56. https://doi.org/10.11648/j.ijsqa.20251102.11

ACS Style

Etana, N. G.; Kero, C. A.; Getahun, M. The Effect of Dynamic Capability and Multichannel Integration Quality on Bank Performance in Case of Commercial Bank of Ethiopia: Application of Sequential QUAN-qual Explanatory Design. Int. J. Sci. Qual. Anal. 2025, 11(2), 39-56. doi: 10.11648/j.ijsqa.20251102.11

AMA Style

Etana NG, Kero CA, Getahun M. The Effect of Dynamic Capability and Multichannel Integration Quality on Bank Performance in Case of Commercial Bank of Ethiopia: Application of Sequential QUAN-qual Explanatory Design. Int J Sci Qual Anal. 2025;11(2):39-56. doi: 10.11648/j.ijsqa.20251102.11

@article{10.11648/j.ijsqa.20251102.11,

author = {Negash Geleta Etana and Chalchissa Amentie Kero and Misganu Getahun},

title = {The Effect of Dynamic Capability and Multichannel Integration Quality on Bank Performance in Case of Commercial Bank of Ethiopia: Application of Sequential QUAN-qual Explanatory Design

},

journal = {International Journal of Science and Qualitative Analysis},

volume = {11},

number = {2},

pages = {39-56},

doi = {10.11648/j.ijsqa.20251102.11},

url = {https://doi.org/10.11648/j.ijsqa.20251102.11},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ijsqa.20251102.11},

abstract = {The main objective of this study was to examine the effects of dynamic capability (DC) on bank performance (BP), mediated by multichannel integration quality (MCIQ) in the case of the Commercial Bank of Ethiopia (CBE), Ambo District. The study employed an explanatory sequential QUAN-qual design, a mixed-methods approach that begins with a quantitative phase to identify patterns and relationships, followed by a qualitative phase to provide deeper insights and explanations for the initial findings. Primary data were collected from 235 bank employees using simple random sampling to ensure representation across branches. The data were gathered through a standardized questionnaire and analyzed using AMOS version 23 and SPSS version 25, applying structural equation modeling to test the hypothesized relationships. The results revealed that both DC and MCIQ have significant positive effects on BP. Additionally, the effect of DC on BP was found to be partially mediated by MCIQ. The study contributes to existing literature by providing empirical evidence on the role of DC and MCIQ in enhancing bank performance. Based on these findings, it is recommended that practitioners and decision-makers focus on developing dynamic capabilities and enhancing multichannel integration quality to achieve sustainable performance. Future research could explore other mediating or moderating factors, and extend the study to other sectors or countries to improve generalizability.},

year = {2025}

}

TY - JOUR T1 - The Effect of Dynamic Capability and Multichannel Integration Quality on Bank Performance in Case of Commercial Bank of Ethiopia: Application of Sequential QUAN-qual Explanatory Design AU - Negash Geleta Etana AU - Chalchissa Amentie Kero AU - Misganu Getahun Y1 - 2025/07/28 PY - 2025 N1 - https://doi.org/10.11648/j.ijsqa.20251102.11 DO - 10.11648/j.ijsqa.20251102.11 T2 - International Journal of Science and Qualitative Analysis JF - International Journal of Science and Qualitative Analysis JO - International Journal of Science and Qualitative Analysis SP - 39 EP - 56 PB - Science Publishing Group SN - 2469-8164 UR - https://doi.org/10.11648/j.ijsqa.20251102.11 AB - The main objective of this study was to examine the effects of dynamic capability (DC) on bank performance (BP), mediated by multichannel integration quality (MCIQ) in the case of the Commercial Bank of Ethiopia (CBE), Ambo District. The study employed an explanatory sequential QUAN-qual design, a mixed-methods approach that begins with a quantitative phase to identify patterns and relationships, followed by a qualitative phase to provide deeper insights and explanations for the initial findings. Primary data were collected from 235 bank employees using simple random sampling to ensure representation across branches. The data were gathered through a standardized questionnaire and analyzed using AMOS version 23 and SPSS version 25, applying structural equation modeling to test the hypothesized relationships. The results revealed that both DC and MCIQ have significant positive effects on BP. Additionally, the effect of DC on BP was found to be partially mediated by MCIQ. The study contributes to existing literature by providing empirical evidence on the role of DC and MCIQ in enhancing bank performance. Based on these findings, it is recommended that practitioners and decision-makers focus on developing dynamic capabilities and enhancing multichannel integration quality to achieve sustainable performance. Future research could explore other mediating or moderating factors, and extend the study to other sectors or countries to improve generalizability. VL - 11 IS - 2 ER -

Department of Management, Ambo University, Ambo, Ethiopia

Department of Management, Ethiopian Civil Service University, Addis Ababa, Ethiopia

Department of Management, Wollega University, Nekemte, Ethiopia

Information