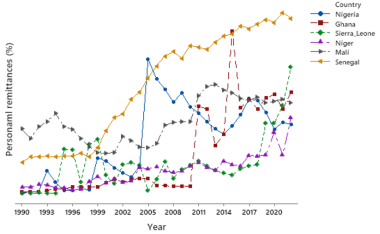

The complexity of the nexus between financial development and remittance inflows in Africa has remained largely underexplored. Therefore, we contributed to the literature by providing more specific and valuable insights into the channels through which financial development affects inward remittances in a panel of six (6) ECOWAS countries (Ghana, Mali, Niger, Nigeria, Senegal, and Sierra Leone). We utilised panel datasets from the World Bank and IMF Financial Statistics and employed the Mean Group (MG) estimator, the Hausman test, and summary statistics for the analysis. The findings showed that the long-term implications of financial institutions' development on remittance inflows are positive. In particular, the effects of financial institution access and efficiency on personal remittances are positive in the long run. This finding indicates that greater access to financial services and efficient, cost-effective allocation of financial resources are beneficial for mobilising personal remittances to the ECOWAS region. Additionally, overall financial development positively affected personal remittances in the long run, being significant at the 5% level, which suggests that gradual and consistent improvements in financial institutions' activities—such as increased access to services, size, efficiency, and stability play an important role in mobilising diaspora remittances to the ECOWAS sub-region. However, the depth of financial institutions has a positive effect on personal remittances. This finding is not significant at the 5% level, indicating that the size of financial institutions relative to GDP has not significantly enhanced the inflows of migrants’ remittances. Based on these findings, we recommend that governments and monetary authorities within ECOWAS collaborate efforts to promote financial development and expand digital financial services, thereby providing a sustainable roadmap for increased remittance inflows.

| Published in | International Journal of Economics, Finance and Management Sciences (Volume 13, Issue 4) |

| DOI | 10.11648/j.ijefm.20251304.16 |

| Page(s) | 235-243 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2025. Published by Science Publishing Group |

Remittances, Financial Development, Financial Access, Depth, Efficiency and ECOWAS

Variable | Notation | Description |

|---|---|---|

Personal remittances | PER | These involve the money remitted by migrants employed in foreign destinations to their home country. This was measured by the remittances received, including personal transfers and compensation as defined in the sixth edition of the IMF's Balance of Payments Manual. |

Financial access | FAC | This is the level to which financial agents, such as individuals or companies, have access to financial institutions in the absence of price and non-price barriers. Consistent with the World Bank definition, financial access ranges from bank account holding to credit access and distribution of bank branches, etc. The financial access index from the World Bank database was utilised as the reference for this variable. |

Financial depth | FDE | This measures the size of the financial sector relative to the economy's GDP. It is often captured by the domestic private credit to the real sector by deposit money banks as a percentage of GDP. The financial depth index provided by the World Bank was relied upon to measure this variable. |

Financial efficiency | FEE | As an important aspect of the financial sector development, financial efficiency refers to the efficient allocation of financial resources at the lowest possible cost. According to the World Bank, this concept includes the lending-deposit spread, overhead costs, and profitability, among other things. To assess this variable, the World Bank's financial efficiency index is used. |

Overall financial development | OFD | This refers to improving in the financial institutions. The World Bank identified financial depth, access, efficiency and stability as the integral aspects of financial institutions' development. This study relied on the financial institutions development index provided by the World Bank to measure this variable. |

Variable | Observation | Mean | Std. dev. | Minimum value | Maximum value |

|---|---|---|---|---|---|

PER | 198 | 3.3404 | 2.8753 | .0036 | 11.232 |

FAC | 198 | .1122 | .16324 | .0060 | .5075 |

FDE | 198 | .04459 | .0221 | .0083 | .1116 |

FEE | 198 | .52485 | .11419 | .2372 | .8937 |

OFD | 198 | .17368 | .03903 | .0843 | .25688 |

Variable | Levels test results | 1st diff. test results | Number of panels | Order of integration |

|---|---|---|---|---|

PER | 0.2937 (0.6155) | -5.5929*** (0.0000) | 6 | I (1) |

FAC | 0.6341 (0.7370) | -1.8182** (0.0345) | 6 | I (1) |

FDE | 0.5926 (0.2767) | -4.4117*** (0.0000) | 6 | I (1) |

FEE | -1.4808* (0.0693) | -7.247*** (0.0000) | 6 | I (1) |

OFD | -1.2274 (0.1098) | -6.7871*** (0.0000) | 6 | I (1) |

Series: PER FAC FDE FEE OFD | ||

|---|---|---|

H0: No cointegration Number of panels = 6 | ||

Ha: All panels are cointegrated Number of periods = 32 | ||

Cointegrating vector: Panel-specific | ||

Statistic | p-value | |

Modified Phillips-Perron t | 0.8593 | 0.1951 |

Phillips-Perron t | -1.6108** | 0.0536 |

Augmented Dickey-Fuller t | -1.7692** | 0.0384 |

Dependent variable: PER | ||

|---|---|---|

(1) | (2) | |

Variables | MG | PMG |

Ec | -0.437*** | -0.363*** |

(0.151) | (0.138) | |

D. FAC | -214.5* | -73.16 |

(117.0) | (57.40) | |

D. FDE | -142.0 | -29.70 |

(101.4) | (35.63) | |

D. FEE | -96.36* | -26.26 |

(55.78) | (16.27) | |

D. OFD | 373.1* | 104.4* |

(220.5) | (63.42) | |

FAC | 630.7*** | 135.5 |

(194.19) | (120.6) | |

FDE | 519.9 | 16.20 |

(458.5) | (109.9) | |

FEE | 330.5*** | 36.25 |

(82.08) | (69.99) | |

OFD | 1,296** | -139.3 |

(504.916) | (273.3) | |

Constant | -0.998 | -0.147 |

(1.228) | (0.452) | |

Observations | 192 | 192 |

Hausman test results | ||

Chi-square statistic | 27.41 | |

Probability value | 0.000 | |

ECOWAS | Economic Community of West African States |

ODA | Official Development Assistance |

GDP | Gross Domestic Product |

PMG | Pooled Mean Group |

| [1] | Adekunle, I. A., Tella, S. A., Subair, K., & Adegboyega, S. B. (2022). Remittances and financial development in Africa. Journal of Public Affairs, 22(3), e2545. |

| [2] | Aggarwal, R., Demirgüç-Kunt, A., & Peria, M. S. M. (2011). Do remittances promote financial development? Journal of Development Economics, 96(2), 255-264. |

| [3] | Ali Bare, U. A., Bani, Y., Ismail, N. W., & Rosland, A. (2022). Does financial development mediate the impact of remittances on sustainable human capital investment? New insights from SSA countries. Cogent Economics & Finance, 10(1), 2078460. |

| [4] | Appiah-Otoo, I., Acheampong, A. O., Song, N., Obeng, C. K., & Appiah, I. K. (2022). Foreign aid—economic growth nexus in Africa: Does financial development matter? International Economic Journal, 36(3), 418-444. |

| [5] | Asongu, S., & Odhiambo, N. M. (2020). Financial access, governance and insurance sector development in Sub-Saharan Africa. Journal of Economic Studies, 47(4), 849-875. |

| [6] | Bang, J. T., Mitra, A., & Wunnava, P. V. (2015). Financial liberalization and remittances: Recent panel evidence. The Journal of International Trade & Economic Development, 24(8), 1077-1102. |

| [7] | Bolarinwa, T. S., & Akinbobola, T. O. (2021). Remittances-financial development nexus: causal evidence from four African countries. Ilorin Journal of Economic Policy, 8(1). |

| [8] | Coulibaly, D. (2015). Remittances and financial development in Sub-Saharan African countries: A system approach. Economic Modelling, 45, 249-258. |

| [9] | Donou-Adonsou, F., Pradhan, G., & Basnet, H. C. (2020). Remittance inflows and financial development: evidence from the top recipient countries in Sub-Saharan Africa. Applied Economics, 52(53), 5807-5820. |

| [10] | Hausman, J. A. (1978). Specification tests in econometrics. Econometrica: Journal of the Econometric Society, 46(6), 1251-1271. |

| [11] | Iheonu, C. O., Asongu, S. A., Odo, K. O., & Ojiem, P. K. (2020). Financial sector development and Investment in selected countries of the Economic Community of West African States: empirical evidence using heterogeneous panel data method. Financial Innovation, 6(1), 29. |

| [12] | Kakhkharov, J., & Rohde, N. (2020). Remittances and financial development in transition economies. Empirical Economics, 59(2), 731-763. |

| [13] | Karikari, N. K., Mensah, S., & Harvey, S. K. (2016). Do remittances promote financial development in Africa? SpringerPlus, 5(1), 1011. |

| [14] | Keho, Y. (2024). Impact of remittances on domestic investment in West African countries: the mediating role of financial development. SN Business & Economics, 4(2), 20-37. |

| [15] | Kim, J. (2021). Financial development and remittances: The role of institutional quality in developing countries. Economic Analysis and Policy, 72, 386-407. |

| [16] | Levin, A., Lin, C. F., & Chu, C. S. J. (2002). Unit root tests in panel data: asymptotic and finite-sample properties. Journal of Econometrics, 108(1), 1-24. |

| [17] | Liu, Y., Luan, L., Wu, W., Zhang, Z., & Hsu, Y. (2021). Can digital financial inclusion promote China's economic growth? International Review of Financial Analysis, 78, 101889. |

| [18] | Makina, D. (2013). Financial access for migrants and intermediation of remittances in South Africa. International Migration, 51, e133-e147. |

| [19] | McKinnon, R. I. (1973). Money and capital in economic development. Washington, DC: Brookings Institution. |

| [20] | Munyegera, G. K., & Matsumoto, T. (2016). Mobile money, remittances, and household welfare: Panel evidence from rural Uganda. World Development, 79, 127-137. |

| [21] | Nshia, C., Fayissa, B., & Wu, C. (2019). The long-run impact of financial development on remittances: Evidence from developing countries. Review of Economics & Finance, 16, 31-46. |

| [22] | Odhiambo, N. M., & Musakwa, M. T. (2024). Remittance inflows and financial development in Sub-Saharan African countries: Does governance matter? Heliyon, 10(5), 1-8. |

| [23] | Olanipekun, D. B. (2024). Workers’ Remittances to Sub-Saharan Africa: Do Institutional Quality and Financial Development Matter? Journal of International Commerce, Economics and Policy, 15(02), 2450008. |

| [24] | Periola, O., & Salami, M. F. (2024). Remittance outflow, financial development and macroeconomic indicators: evidence from the UK. Future Business Journal, 10(1), 83. |

| [25] | Pesaran, M. H., & Smith, R. (1995). Estimating long-run relationships from dynamic heterogeneous panels. Journal of Econometrics, 68(1), 79-113. |

| [26] | Pesaran, M. H., Shin, Y., & Smith, R. P. (1999). Pooled mean group estimation of dynamic heterogeneous panels. Journal of the American Statistical Association, 94(446), 621-634. |

| [27] | Ratha, D., Mohapatra, S., & Scheja, E. (2011). Impact of migration on economic and social development: A review of evidence and emerging issues. World Bank Policy Research Working Paper No. 5558. |

| [28] | Shaw, E. S. (1973). Financial deepening in economic development. New York: Oxford University Press. |

| [29] | Sibindi, A. B. (2014). Remittances, financial development and economic growth: empirical evidence from Lesotho. Journal of Governance and Regulation, 3(4), 116-124. |

| [30] | Sobiech, I. (2019). Remittances, finance and growth: Does financial development foster the impact of remittances on economic growth? World Development, 113, 44-59. |

| [31] | United Nations (2022). Strengthening the developmental impact of remittances and diaspora finance in Africa. Retrieved from: |

| [32] | United Nations (2024). Remittances In West Africa: Challenges and Opportunities for Economic Development. Retrieved from: |

| [33] | Williams, K. (2016). Remittances and financial development: Evidence from sub‐Saharan Africa. African Development Review, 28(3), 357-367. |

| [34] | Williamson, O. E. (1981). The economics of organisation: The transaction cost approach. American Journal of Sociology, 87(3), 548-577. |

| [35] |

World Bank (2020). Global Financial Development Report 2019 / 2020: Bank Regulation and Supervision a Decade after the Global Financial Crisis. Available on:

https://www.worldbank.org/en/publication/gfdr/data/global-financial-development-database |

APA Style

Ezekwe, C. I., Agama, E. I., Enebeli, J. (2025). Financial Development and Remittances Inflow: Evidence from a Panel of Six Countries in the Economic Community of West African States (ECOWAS). International Journal of Economics, Finance and Management Sciences, 13(4), 235-243. https://doi.org/10.11648/j.ijefm.20251304.16

ACS Style

Ezekwe, C. I.; Agama, E. I.; Enebeli, J. Financial Development and Remittances Inflow: Evidence from a Panel of Six Countries in the Economic Community of West African States (ECOWAS). Int. J. Econ. Finance Manag. Sci. 2025, 13(4), 235-243. doi: 10.11648/j.ijefm.20251304.16

@article{10.11648/j.ijefm.20251304.16,

author = {Christopher Ifeanyi Ezekwe and Evwienure Ibunor Agama and James Enebeli},

title = {Financial Development and Remittances Inflow: Evidence from a Panel of Six Countries in the Economic Community of West African States (ECOWAS)

},

journal = {International Journal of Economics, Finance and Management Sciences},

volume = {13},

number = {4},

pages = {235-243},

doi = {10.11648/j.ijefm.20251304.16},

url = {https://doi.org/10.11648/j.ijefm.20251304.16},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ijefm.20251304.16},

abstract = {The complexity of the nexus between financial development and remittance inflows in Africa has remained largely underexplored. Therefore, we contributed to the literature by providing more specific and valuable insights into the channels through which financial development affects inward remittances in a panel of six (6) ECOWAS countries (Ghana, Mali, Niger, Nigeria, Senegal, and Sierra Leone). We utilised panel datasets from the World Bank and IMF Financial Statistics and employed the Mean Group (MG) estimator, the Hausman test, and summary statistics for the analysis. The findings showed that the long-term implications of financial institutions' development on remittance inflows are positive. In particular, the effects of financial institution access and efficiency on personal remittances are positive in the long run. This finding indicates that greater access to financial services and efficient, cost-effective allocation of financial resources are beneficial for mobilising personal remittances to the ECOWAS region. Additionally, overall financial development positively affected personal remittances in the long run, being significant at the 5% level, which suggests that gradual and consistent improvements in financial institutions' activities—such as increased access to services, size, efficiency, and stability play an important role in mobilising diaspora remittances to the ECOWAS sub-region. However, the depth of financial institutions has a positive effect on personal remittances. This finding is not significant at the 5% level, indicating that the size of financial institutions relative to GDP has not significantly enhanced the inflows of migrants’ remittances. Based on these findings, we recommend that governments and monetary authorities within ECOWAS collaborate efforts to promote financial development and expand digital financial services, thereby providing a sustainable roadmap for increased remittance inflows.},

year = {2025}

}

TY - JOUR T1 - Financial Development and Remittances Inflow: Evidence from a Panel of Six Countries in the Economic Community of West African States (ECOWAS) AU - Christopher Ifeanyi Ezekwe AU - Evwienure Ibunor Agama AU - James Enebeli Y1 - 2025/08/20 PY - 2025 N1 - https://doi.org/10.11648/j.ijefm.20251304.16 DO - 10.11648/j.ijefm.20251304.16 T2 - International Journal of Economics, Finance and Management Sciences JF - International Journal of Economics, Finance and Management Sciences JO - International Journal of Economics, Finance and Management Sciences SP - 235 EP - 243 PB - Science Publishing Group SN - 2326-9561 UR - https://doi.org/10.11648/j.ijefm.20251304.16 AB - The complexity of the nexus between financial development and remittance inflows in Africa has remained largely underexplored. Therefore, we contributed to the literature by providing more specific and valuable insights into the channels through which financial development affects inward remittances in a panel of six (6) ECOWAS countries (Ghana, Mali, Niger, Nigeria, Senegal, and Sierra Leone). We utilised panel datasets from the World Bank and IMF Financial Statistics and employed the Mean Group (MG) estimator, the Hausman test, and summary statistics for the analysis. The findings showed that the long-term implications of financial institutions' development on remittance inflows are positive. In particular, the effects of financial institution access and efficiency on personal remittances are positive in the long run. This finding indicates that greater access to financial services and efficient, cost-effective allocation of financial resources are beneficial for mobilising personal remittances to the ECOWAS region. Additionally, overall financial development positively affected personal remittances in the long run, being significant at the 5% level, which suggests that gradual and consistent improvements in financial institutions' activities—such as increased access to services, size, efficiency, and stability play an important role in mobilising diaspora remittances to the ECOWAS sub-region. However, the depth of financial institutions has a positive effect on personal remittances. This finding is not significant at the 5% level, indicating that the size of financial institutions relative to GDP has not significantly enhanced the inflows of migrants’ remittances. Based on these findings, we recommend that governments and monetary authorities within ECOWAS collaborate efforts to promote financial development and expand digital financial services, thereby providing a sustainable roadmap for increased remittance inflows. VL - 13 IS - 4 ER -

Department of Economics, Rivers State University, Port Harcourt, Nigeria

Financial Institutions Department, Central Bank of Nigeria (CBN), Port Harcourt, Nigeria

Department of Economics, Rivers State University, Port Harcourt, Nigeria

Information