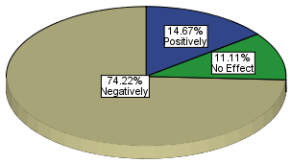

The purpose of this study is to examine the influence of collateral requirements on the performance of small and medium-sized businesses (SMEs) in Meru County, Kenya. A proportional random stratified design was used to select the 234 SMEs that make up the study's sample. Data was gathered from registered business owners and/or employees using questionnaires. Descriptive statistics, frequency tables, and chi-square tests were used to examine the data. The study established that demand of collateral affected performance of SMEs negatively by a proportion of 74%. Additionally, there was a significant relationship between collateral requirements and the performance of SMEs in Meru County. It is proposed in this study that financial institutions should consider accepting non-tangible collateral. However, this should take place after thorough customers’ background checks have been done. The findings are significant for addressing credit and financial concerns, which are critical to the growth and long-term sustainability of the SME sector.

| Published in | International Journal of Accounting, Finance and Risk Management (Volume 10, Issue 1) |

| DOI | 10.11648/j.ijafrm.20251001.14 |

| Page(s) | 62-71 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2025. Published by Science Publishing Group |

Collateral Requirements, Performance of SMEs, Credit Accessibility

Value | Df | Asymp. Sig. (2-sided) | |

|---|---|---|---|

Pearson Chi-Square | 55.855 | 12 | .000 |

Likelihood Ratio | 56.893 | 12 | .000 |

Linear-by-Linear Association | 540 | 1 | .462 |

N of Valid Cases | 225 |

SMEs | Small and Medium Enterprises |

GDP | Gross Domestic Product |

MSME | Micro, Small and Medium Enterprises |

OECD | Organization for Economic Cooperation and Development |

| [1] |

World Bank. (2015). Small and Medium Enterprises (SMEs) Finance. Retrieved From

http://www.worldbank.org/en/topic/financialsector/brief/smes-finance |

| [2] | Edinburgh Group (2013). Growing the Global Economy through SMEs. Retrieved from |

| [3] | European Commission. (2016). Entrepreneurship and Small and Medium-sized Enterprises (SMEs). Retrieved from |

| [4] | SME Europe (20160. About Us. Retrieved from |

| [5] | EBRD. (2016). EBRD/EU increase support for SMEs and Women Entrepreneurs in Eastern Partnership countries. Retrieved From |

| [6] | IFC (2016). SME Initiatives. Retrieved from |

| [7] | Obinne, U. G. & Igwebuike, A. E. (2013). The Effect of External Agencies’ Financial Assistance and Bank Credit on the Development and Growth of Small and Medium Enterprises in Nigeria. Research Journal of Finance and Accounting, 4(12), 181-194. |

| [8] | SMEFEST (2016). The Kenya SME Sector Case Study. Retrieved from |

| [9] |

KNBS (2015). Kenya Economic Survey 2014. Kenya National Bureau of Statistics. Retrieved from

http://www.knbs.or.ke/index.php?option=com_content&view=article&id=250:es&catid=82:news&Itemid=593 |

| [10] |

Syekei, J., & Opijah D. (2015). Kenya’s Vision 2030: Creating more Dinner Space for SMEs on the IP Table. Retrieved from

http://www.coulsonharney.com/News-Blog/Blog/Creating-more-dinner-space-for-SMEs |

| [11] | Katua, T. G. (2014). The Role of SMEs in Employment Creation and Economic Growth in Selected Countries. International Journal of Education and Research, 2(12), 461- 472. |

| [12] | Kinyua, A. N. (2014). Factors Affecting the Performance of Small and Medium Enterprises in the Jua Kali Sector in Nakuru Town, Kenya. IOSR Journal of Business and Management, 16(1), 80-93. |

| [13] | Harash, E., Al-Timimi, S., & Alsaadi. J. (2014). The Influence of Finance on Performance of Small and Medium Enterprises (SMES). International Journalm of Engineering and Innovative Technology, 4(3), 161-167. |

| [14] | Gichuki, J. A. N., Njeru, A. & Tirimba, O. I. (2014). The challenges facing Micro and Small Enterprises in accessing credit facilities in Kangemi Harambee Market in Nairobi City County, Kenya. International Journal of Scientific and Research Publications, 4(12), 1-25. |

| [15] | Obwocha, H. (2006). Small businesses and Economic Growth in Eastern Africa. Speech by Minister for Planning and National Development, Republic of Kenya to the International Finance Corporation “Credit Reporting Conference” at Safari Park Hotel, Nairobi. |

| [16] | Hvingelby, C. E., & Jensen, P. M. (2013). Problems the Danish small and medium-sized enterprises face in the process of funding in the European Union (Unpublished thesis). Aarhus School of Business. |

| [17] | Avevor, E. E. (2016). Challenges faced by SMEs when accessing funds from financial institutions in Ghana. University of Applied Sciences. |

| [18] | Ackah, J. & Vuvor, S. (2011). Challenges faced by small & medium enterprises (SMEs) in obtaining credit in Ghana (Unpublished\ thesis). |

| [19] | Falkena, H., Abedian, I., von Blottnitz, M., Coovadia, C., Davel, G., Madungandaba, J., Masilela, E., & Rees, S. (2001). SMEs access to finance in South Africa - a supply side regulatory review. Pretoria, South Africa: Policy Board for Financial Services and Regulation. |

| [20] | Omboi B. M., & Wangai, P. N. (2011). Factors that Influence the Demand for Credit for Credit Among Small-Scale Investors: a case study of Meru Central District, Kenya. Research Journal of Finance and Accounting, 2(2), 1-30. |

| [21] | Nyumba, E. O. et. al., (2015). Loan Interest Rate and Performance of Small and Medium Enterprises in Kenya. International Journal of Management Research & Review, 5(10), 712-728. |

| [22] | Grant, S., & Vidler, C. (2002). Economics in Context. Oxford: Heinemann. |

| [23] | McEachern, W. A. (2013). Contemporary Economics (3rd ed.). Mason, OH: South- Western Cengage Learning. |

| [24] | Basu, S. (2012). Financial Liberalization and Intervention: A New Analysis of Credit Rationing. Northampton, MA: E. Elgar. |

| [25] | Matthews, K., & Thomson, J. (2005). The Economics of Banking. London: John Wiley & Sons. |

| [26] | Bebczuk, R. N. (2003). Asymmetric Information in Financial Markets: Introduction and Applications. Cambridge: CUP. |

| [27] | Bloem, A. M., & Gorter, C. N. (2001). The Treatment for Non-Performing Loans in Macroeconomic Statistics. IMF Working Paper/01/209. Retrieved from |

| [28] | Brigham, E., & Houston, J. F. (2009). Fundamentals of Financial Management. Boston, MA: Cengage Learning. |

| [29] | Greuning, H., & Bratanovic, S. B. (2009). Analyzing Banking Risk: A Framework for Assessing Corporate Governance and Risk Management (3rd ed.). Washington DC: World Bank. |

| [30] | Beaver, G., & Prince, C. (2002). Innovation, entrepreneurship and competitive advantage in the entrepreneurial venture. J. Small Bus. & Enterprise Develop, 9(1): 28-37. |

| [31] |

Allbusiness.com (2016). What Lenders Look for Before Granting a Small Business Loan. Retrieved from

https://www.allbusiness.com/what-lenders-look-for-before-granting-a-small-business-loan-3532-1.html |

| [32] | Osano, H. M. & Languitone, H. (2016). Factors influencing access to finance by SMEs in Mozambique: case of SMEs in Maputo Central Business District. Journal of Innovation and Entrepreneurship, 5: 13. |

| [33] | Kung’u, G. K. (2011). Factors influencing SMEs access to finance: A case study of Westland Division, Kenya. MPPRA, 1-27. Retrieved from |

| [34] | Lore, M. (2011). An Evaluation of Human Capital Factors That Enhance Access to Credit Among Retailers in Nairobi. USIU Nairobi, Kenya. |

| [35] | Trochim, W., Donnelly, J. P., & Arora, K. (2015). Research Methods: The Essential Knowledge Base. Mason, OH: Cengage Learning. |

| [36] | Rubin, A., & Babbie, E. R. (2010). Essential Research Methods for Social Work (2ed ed.). Belmont, CA: Brooks / Cole Cengage Learning. |

| [37] | Meru County Government (2016). Registered SMEs in Meru County. County Government of Meru. |

| [38] | Kothari C. R. (2003). Research Methodology: Methods and Techniques (2nd Ed.). New Delhi: New Age (P) Limited International Publisher. |

| [39] | Krejcie, R. V. & Morgan, D. W. (1970). Determining Sample Size for Research Activities. Educational and Psychological Measurement, 30, 607-610. |

| [40] | Kombo, D. K. & Tromp, D. L. A. (2006). An Introduction to Proposal and Thesis Writing. (Reprint 11th ed.). Pauline’s Publications Africa. |

| [41] | Denscombe, M. (2007). The Good Research Guide: For Small-Scale Social Research Projects (3rd ed.). New York: Open University Press. |

| [42] | Mugenda, A. G., & Mugenda, O. M. (2003). Research Methods, Quantitative and Qualitative Approaches. ACTS Press, Nairobi. |

| [43] | Tabachnick, B. G. & Fidell, L. S. (2007). Using Multivariate Statistics, (6th ed.). California State University – Northridge. |

| [44] | Kihimbo, B. W., Ayako, B. A., Omoka, K. W., & Otuya, W. L. (2012). Financing of Small and Medium Enterprises (SMEs) in Kenya: A study of selected SMEs in Kakamega Municipality. International Journal of Current Research, 4(4), 303-309. Retrieved from |

| [45] |

Department for Business, Innovation and Skills. (2015, October 14). Business population estimates for the UK and regions 2015(URN 15/92). Department for Business, Innovation and Skills.

https://www.gov.uk/government/collections/business-population-estimates |

| [46] |

Sousa dos Santos, J. F. (2015). Why SMEs are key to growth in Africa. World Economic. Forum. Retrieved from

https://www.weforum.org/agenda/2015/08/why-smes-are-key-to-growth-in-africa/ |

| [47] | King, K., & McGrath, S. (2002). Globalization, Enterprise and Knowledge: Education, Training and Development in Africa (Monographs in International Education). Westminster, IR: Symposium Books. |

| [48] | Mertler, C. A. (2006). Action Research: Teachers as Researchers in the Classroom. Thousand Oaks, CA: Sage Publications. |

| [49] | Ross, A. Westerfield &Jordan (2008),” Essentials of corporate Finance” Hill international edition. |

| [50] | Ahmed, S. F., & Malik, Q. A. (2015). Credit risk management and loan performance: Empirical investigation of microfinance banks of Pakistan. International Journal of Economics and Financial Issues, 5(2), 574-579. Retrieved from |

| [51] | Atta-Mensah, J. (2015). The Role of Collateral in Credit Markets. Journal of Mathematical Finance, 5, 315-327. |

| [52] | Kamunge, M. S., Njeru, A., & Tirimba, O. I. (2014). Factors affecting the performance of small and micro enterprises (SMEs) traders at Limuru Town market in Kiambu County. International Journal of Scientific and Research Publications, 4(12), 1-20. |

APA Style

Kaimenyi, M. S. (2025). Influence of Collateral Requirements on Performance of SMEs Business in Meru County, Kenya. International Journal of Accounting, Finance and Risk Management, 10(1), 62-71. https://doi.org/10.11648/j.ijafrm.20251001.14

ACS Style

Kaimenyi, M. S. Influence of Collateral Requirements on Performance of SMEs Business in Meru County, Kenya. Int. J. Account. Finance Risk Manag. 2025, 10(1), 62-71. doi: 10.11648/j.ijafrm.20251001.14

AMA Style

Kaimenyi MS. Influence of Collateral Requirements on Performance of SMEs Business in Meru County, Kenya. Int J Account Finance Risk Manag. 2025;10(1):62-71. doi: 10.11648/j.ijafrm.20251001.14

@article{10.11648/j.ijafrm.20251001.14,

author = {Muriungi Silas Kaimenyi},

title = {Influence of Collateral Requirements on Performance of SMEs Business in Meru County, Kenya

},

journal = {International Journal of Accounting, Finance and Risk Management},

volume = {10},

number = {1},

pages = {62-71},

doi = {10.11648/j.ijafrm.20251001.14},

url = {https://doi.org/10.11648/j.ijafrm.20251001.14},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ijafrm.20251001.14},

abstract = {The purpose of this study is to examine the influence of collateral requirements on the performance of small and medium-sized businesses (SMEs) in Meru County, Kenya. A proportional random stratified design was used to select the 234 SMEs that make up the study's sample. Data was gathered from registered business owners and/or employees using questionnaires. Descriptive statistics, frequency tables, and chi-square tests were used to examine the data. The study established that demand of collateral affected performance of SMEs negatively by a proportion of 74%. Additionally, there was a significant relationship between collateral requirements and the performance of SMEs in Meru County. It is proposed in this study that financial institutions should consider accepting non-tangible collateral. However, this should take place after thorough customers’ background checks have been done. The findings are significant for addressing credit and financial concerns, which are critical to the growth and long-term sustainability of the SME sector.

},

year = {2025}

}

TY - JOUR T1 - Influence of Collateral Requirements on Performance of SMEs Business in Meru County, Kenya AU - Muriungi Silas Kaimenyi Y1 - 2025/02/20 PY - 2025 N1 - https://doi.org/10.11648/j.ijafrm.20251001.14 DO - 10.11648/j.ijafrm.20251001.14 T2 - International Journal of Accounting, Finance and Risk Management JF - International Journal of Accounting, Finance and Risk Management JO - International Journal of Accounting, Finance and Risk Management SP - 62 EP - 71 PB - Science Publishing Group SN - 2578-9376 UR - https://doi.org/10.11648/j.ijafrm.20251001.14 AB - The purpose of this study is to examine the influence of collateral requirements on the performance of small and medium-sized businesses (SMEs) in Meru County, Kenya. A proportional random stratified design was used to select the 234 SMEs that make up the study's sample. Data was gathered from registered business owners and/or employees using questionnaires. Descriptive statistics, frequency tables, and chi-square tests were used to examine the data. The study established that demand of collateral affected performance of SMEs negatively by a proportion of 74%. Additionally, there was a significant relationship between collateral requirements and the performance of SMEs in Meru County. It is proposed in this study that financial institutions should consider accepting non-tangible collateral. However, this should take place after thorough customers’ background checks have been done. The findings are significant for addressing credit and financial concerns, which are critical to the growth and long-term sustainability of the SME sector. VL - 10 IS - 1 ER -

Department of Accounting and Finance, Kenyatta University, Nairobi, Kenya

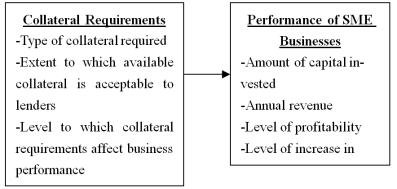

Figure 1. Conceptual Framework.

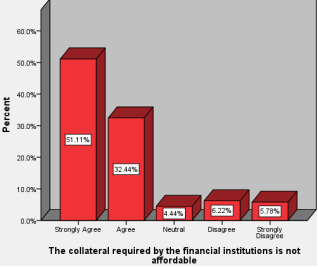

Figure 2. Collateral required in not affordable.

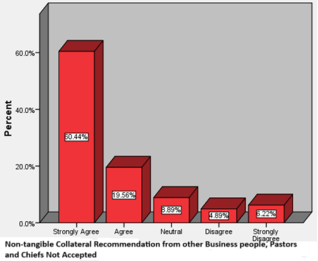

Figure 3. Non-tangible collateral not accepted.

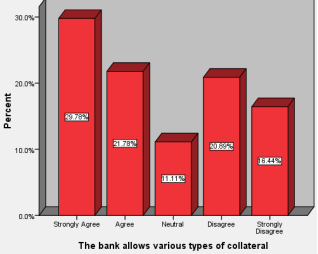

Figure 4. The bank allows various types of collateral.

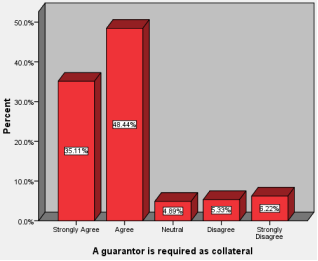

Figure 5. A guarantor is required as collateral.

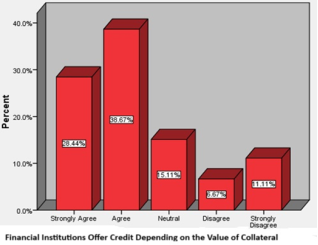

Figure 6. Credit value depends on the value of collateral.

Figure 7. How demand for collateral affected performance of SMEs.

Information