1. Introduction

Budgeting and budgetary control play a crucial role in ensuring financial discipline, resource allocation, and strategic decision-making within public sector organizations. In Ghana, Metropolitan, Municipal, And District Assemblies (MMDAs) attach significance to the preparation and implementation of budgets

| [14] | Frimpong, E. A., Ameyaw, F., and Osei-Bonsu, E. (2017). Budgeting and budgetary control practices in timber industries in Ghana. A case of logs and lumber limited. International Journal of Technology and Management Research. 2(2), 44-50. |

| [15] | Owusu-Akomeah, M. N., Asare, J., Afriyie, S. O., and Kumah, E. A. (2022). Public sector financial management reforms in Developing Economies: Insights from Ghana. Universal Journal of Accounting and Finance, 10(4): 838–851. |

| [17] | Scott, G. K., Enu-Kwesi, F. (2018). Role of budgeting practices in service delivery in the public sector: A study of district assemblies in Ghana. Human Resource Management Research, 8(2), 23-33. |

[14, 15, 17]

. However, there are challenges associated with budgeting, and the extent to which budget variance reports are used as a performance measure needs to be explored

| [1] | Anaman, P. D. (2023). Challenges to Budget implementation in public institutions at the local level of Ghana. International Journal of Innovative Science Research. 8(3), 733-741. |

[1]

. The effective management of budgetary resources is essential for addressing strategic priorities and regulating economic and socio-demographic processes in the country. Budget expenditures serve as a tool for achieving development goals and require targeted management to ensure their effectiveness

.

Several studies have explored the impact and effectiveness of budgetary control mechanisms in various contexts

| [3] | Imo, T., Des-Wosu, C. (2018). An assessment on the effect of budgetary control on return on assets and net profit of government-owned companies in rivers state. International Journal of Academic Research in Accounting Finance and Management Sciences, 8(3). https://doi.org/10.6007/ijarafms/v8-i3/4836 |

| [4] | Roshchektaeva, U., Roshchektaev, S. (2018). Internal state (municipal) financial control in the context of the formation of the institutional structure. Scientific Bulletin of the Southern Institute of Management, (3), 78-82. https://doi.org/10.31775/2305-3100-2018-3-78-82 |

| [5] | Siefu, D., Njocke, M., and Yah, N. (2018). Government spending and economic growth in Cameroon. European Scientific Journal, 14(28), 68. https://doi.org/10.19044/esj.2018.v14n28p68 |

| [6] | Mochizuki, J., Schinko, T., and Hochrainer-Stigler, S. (2018). Mainstreaming of climate extreme risk into fiscal and budgetary planning: application of stochastic debt and disaster fund analysis in Austria. Regional Environmental Change, 18(7), 2161-2172. https://doi.org/10.1007/s10113-018-1300-3 |

| [7] | Ocheni, S., Agba, M. (2018). Fiscal decentralisation, public expenditure management and human capital development in Nigeria. Academic Journal of Interdisciplinary Studies, 7(1), 153-162. https://doi.org/10.2478/ajis-2018-0016 |

[3-7]

.

| [3] | Imo, T., Des-Wosu, C. (2018). An assessment on the effect of budgetary control on return on assets and net profit of government-owned companies in rivers state. International Journal of Academic Research in Accounting Finance and Management Sciences, 8(3). https://doi.org/10.6007/ijarafms/v8-i3/4836 |

[3]

conducted a study on government-owned companies in Rivers State, Nigeria, and found that budgetary control can strengthen performance measurement systems. This finding underscores the importance of budgetary control in improving accountability and aligning organizational goals with resource allocation. However, the study's focus on government-owned companies raises questions about the generalizability of the findings to the broader public sector.

The study emphasized the role of state (municipal) control bodies in ensuring effective planning and spending of budgetary funds.

| [4] | Roshchektaeva, U., Roshchektaev, S. (2018). Internal state (municipal) financial control in the context of the formation of the institutional structure. Scientific Bulletin of the Southern Institute of Management, (3), 78-82. https://doi.org/10.31775/2305-3100-2018-3-78-82 |

[4]

While their emphasis on preventing violations of legislation in the budgetary sphere is crucial, the study's focus on the role of control bodies does not explore the impact of internal budgetary control mechanisms within organizations, leaving room for further investigation.

discussed the role of government spending in promoting economic development, particularly through public investment budgets. Their argument for government spending as a key instrument for economic development aligns with established economic theories. However, the study's focus on the macroeconomic perspective lacks specific insights into the mechanisms of budgetary control at the organizational level.

| [6] | Mochizuki, J., Schinko, T., and Hochrainer-Stigler, S. (2018). Mainstreaming of climate extreme risk into fiscal and budgetary planning: application of stochastic debt and disaster fund analysis in Austria. Regional Environmental Change, 18(7), 2161-2172. https://doi.org/10.1007/s10113-018-1300-3 |

[6]

highlighted the need for budgetary arrangements to deal effectively with rising risks of extreme events, such as floods. This study emphasizes the importance of integrating risk management into budgetary processes, which can enhance resilience in the face of unforeseen events. Nevertheless, the research does not delve into the practical implementation challenges and strategies for integrating risk assessment into budgeting.

The study emphasized the importance of prudent management of public expenditure in Nigeria, particularly for human capital development.

| [7] | Ocheni, S., Agba, M. (2018). Fiscal decentralisation, public expenditure management and human capital development in Nigeria. Academic Journal of Interdisciplinary Studies, 7(1), 153-162. https://doi.org/10.2478/ajis-2018-0016 |

[7]

The study underscores the critical role of budgetary control in promoting true developmental efforts. However, it remains essential to explore specific budgetary control mechanisms that contribute to effective human capital development in the context of public sector organizations. The subsequent literature reinforces the significance of budget and budgetary control in various sectors and contexts. Studies emphasize the importance of budgetary control measures, such as planning, coordination, and evaluation, in improving organizational performance and aligning resources with goals

| [8] | Kemunto, D., Cheluget, J. (2022). Budgetary controls and financial performance of micro finance institutions (mfis) in Kenya. Journal of Finance and Accounting, 6(4), 123-145. https://doi.org/10.53819/81018102t6045 |

[8]

. However, they also highlight challenges related to excessive regulation and the need for adaptive budgeting approaches

| [9] | Dokulil, J., Popesko, B., and Dvorský, J. (2020). The budgeting processes of czech companies: the role of the ownership structure and foreign capital. Oeconomia Copernicana, 11(4), 779-798. https://doi.org/10.24136/oc.2020.031 |

[9]

.

The integration of technology into budgeting processes is identified as a means to enhance transparency and accountability

| [10] | Ivanchenkova, L., Tkachuk, H., SKLIAR, L., Holynska, O., Stasiukova, K., and Tomchuk, Y. (2021). Improving the internal financial control of expenditures of the budgetary institutions under the influence of the crisis caused by covid-19. Universal Journal of Accounting and Finance, 9(5), 1067-1084. https://doi.org/10.13189/ujaf.2021.090517 |

[10]

. Nevertheless, questions arise regarding the readiness of organizations to adopt digital financial control measures effectively and the potential impact on budgetary efficiency. The role of budgetary control in preventing financial mismanagement and ensuring efficient resource utilization is evident in various studies

| [11] | Beldiman, C. (2022). Efficiency and advantages of preventive financial control versus internal control in a public entity. Jurnalul De Studii Juridice, 17(1-2), 134-147. https://doi.org/10.18662/jls/17.1-2/104 |

[11]

. However, the practical implementation of preventive financial control and its alignment with organizational goals warrant further exploration. While budgetary control measures can improve financial performance and risk management, they may also have unintended consequences, such as inefficiencies and deviations from organizational goals

| [12] | Onana, S. (2023). Do programme budget mechanisms improve the efficiency of public spending? Elements of theory and empirical data from Cameroon. International Review of Administrative Sciences. https://doi.org/10.1177/00208523231201256 |

[12]

. Therefore, it is essential to strike a balance between control mechanisms and organizational adaptability.

The findings emphasize their significance in improving performance, managing risks, and aligning resources with goals. However, there is a need for further research to explore the specific mechanisms, challenges, and practical strategies for effective budgetary control within public sector organizations, ensuring that budgetary control measures yield optimal outcomes while promoting transparency and accountability. The study also highlights the importance of financial control mechanisms in ensuring the efficiency of local budget expenditures. Lessons from the experience of financial control in Scotland can provide insights for improving budgetary control practices in Ghana and other countries

. Furthermore, it is essential to understand how budgeting and budgetary control practices are implemented in specific industries. For example, the timber industry in Ghana can provide insights into the use of budgeting and budgetary control in achieving desired results

| [14] | Frimpong, E. A., Ameyaw, F., and Osei-Bonsu, E. (2017). Budgeting and budgetary control practices in timber industries in Ghana. A case of logs and lumber limited. International Journal of Technology and Management Research. 2(2), 44-50. |

[14]

.

Despite the importance of budget and budgetary control in controlling public expenditure, there is a lack of comprehensive research on their effectiveness in the context of public sector organizations in Ghana. While budgeting processes are in place, there is a need to assess whether they are effectively implemented and whether they lead to the desired outcomes of controlling public expenditure. Additionally, challenges and gaps in the implementation of budget and budgetary control practices in the Ghanaian public sector still persists

| [1] | Anaman, P. D. (2023). Challenges to Budget implementation in public institutions at the local level of Ghana. International Journal of Innovative Science Research. 8(3), 733-741. |

| [18] | Dauda, H., Suhuyini, A. S., and Antwi-Boasiako, J. (2020). Ghana’s parliament in ensuring an efficient public financial management. The Journal of Legislative Studies. 26(4), 542-557. |

[1, 18]

, which requires novel ideas to warrant improvements. This study therefore innovatively investigate the extent to which budget and budgetary control could serve as a real tool for controlling public expenditure in the context of public sector organizations in Ghana.

The motivation behind this study is to examine the effectiveness of budget and budgetary control as a tool for controlling public expenditure in the context of public sector organizations in Ghana. Public expenditure management is a critical aspect of governance, and it is essential to ensure that public funds are allocated and utilized efficiently and effectively. Budget and budgetary control play a crucial role in this process by providing a framework for planning, monitoring, and controlling public expenditure. Understanding the extent to which budget and budgetary control contribute to controlling public expenditure in Ghana can inform policymakers and public sector managers in improving financial management practices.

There is a scarcity of empirical studies that specifically focus on the effectiveness of budget and budgetary control in controlling public expenditure in the Ghanaian public sector. Existing literature within the context of Ghana tends to be more theoretical or focuses on aspects of public financial management (including reforms and challenges) rather than how budgeting and budgetary control can be used as a tool for administering public expenditure

| [15] | Owusu-Akomeah, M. N., Asare, J., Afriyie, S. O., and Kumah, E. A. (2022). Public sector financial management reforms in Developing Economies: Insights from Ghana. Universal Journal of Accounting and Finance, 10(4): 838–851. |

| [16] | Tetteh, L. A., Agyenim-Boateng, C., Simpson, S. N. Y., and Susuawu, D. (2021), Public sector financial management reforms in Ghana: Insights from institutional theory, Journal of Accounting in Emerging Economies, 11(5), 691–713. |

| [17] | Scott, G. K., Enu-Kwesi, F. (2018). Role of budgeting practices in service delivery in the public sector: A study of district assemblies in Ghana. Human Resource Management Research, 8(2), 23-33. |

| [18] | Dauda, H., Suhuyini, A. S., and Antwi-Boasiako, J. (2020). Ghana’s parliament in ensuring an efficient public financial management. The Journal of Legislative Studies. 26(4), 542-557. |

[15-18]

.

For instance,

| [1] | Anaman, P. D. (2023). Challenges to Budget implementation in public institutions at the local level of Ghana. International Journal of Innovative Science Research. 8(3), 733-741. |

[1]

highlighted the challenges that adversely influence budget implementation among public sector institutions. The study reports inadequate training on technological tools, inappropriate monitoring equipment, and interferences from the government, government decisions to reduce spending and even lack of proper training on functioning and implementation of budgets.

| [15] | Owusu-Akomeah, M. N., Asare, J., Afriyie, S. O., and Kumah, E. A. (2022). Public sector financial management reforms in Developing Economies: Insights from Ghana. Universal Journal of Accounting and Finance, 10(4): 838–851. |

[15]

provided an empirical evidence on Program Based Budgeting (PBB) as a Public Financial Management Reform (PFMR) in Ghana. The study highlighted the need to safeguard internally generated funds or fiscal resources via a continuous reform of laws and regulations governing how resources are mobilized and expended.

| [16] | Tetteh, L. A., Agyenim-Boateng, C., Simpson, S. N. Y., and Susuawu, D. (2021), Public sector financial management reforms in Ghana: Insights from institutional theory, Journal of Accounting in Emerging Economies, 11(5), 691–713. |

[16]

with insights from the institutional theory also investigated Public Financial Management Reforms (PFMR) in Ghana. The study emphasized that Ghana’s adoption of an integrated financial management information system was as a result of some institutional pressures.

| [17] | Scott, G. K., Enu-Kwesi, F. (2018). Role of budgeting practices in service delivery in the public sector: A study of district assemblies in Ghana. Human Resource Management Research, 8(2), 23-33. |

[17]

focused on the role of budgeting practices in service delivery among district assemblies in Ghana. The study highlights the need for district assemblies to apply laid-down procedures, provide adequate information and administer budgets appropriately by emphasizing on activities that are included in the budgets rather than expend on non-essentials. The study also underscores the importance of strict adherence to budgetary process for effective service delivery to the public. Nonetheless, the study justifies the achievement of such ends by means of social media and other innovative communication tools. Whiles this can be considered a sound contribution, one effective but often neglected approach is the efficacies of budgeting and budgetary control dynamics as a real tool for realizing public spending expectations.

Most studies on budget and budgetary control are conducted in developed countries or in the context of multinational organizations

| [10] | Ivanchenkova, L., Tkachuk, H., SKLIAR, L., Holynska, O., Stasiukova, K., and Tomchuk, Y. (2021). Improving the internal financial control of expenditures of the budgetary institutions under the influence of the crisis caused by covid-19. Universal Journal of Accounting and Finance, 9(5), 1067-1084. https://doi.org/10.13189/ujaf.2021.090517 |

| [11] | Beldiman, C. (2022). Efficiency and advantages of preventive financial control versus internal control in a public entity. Jurnalul De Studii Juridice, 17(1-2), 134-147. https://doi.org/10.18662/jls/17.1-2/104 |

| [12] | Onana, S. (2023). Do programme budget mechanisms improve the efficiency of public spending? Elements of theory and empirical data from Cameroon. International Review of Administrative Sciences. https://doi.org/10.1177/00208523231201256 |

| [13] | Malyniak, B., Pidlisny, I. (2018). Efficiency of local budget expenditures: Control mechanism in Scotland and lessons for Ukraine. World of Finance. https://doi.org/10.35774/sf2018.03.041 pp. 41-57. |

[10-13]

. There is a need for research that is specifically tailored to the Ghanaian public sector, taking into account its unique institutional, cultural, and economic factors. By addressing these research gaps, this study aims to contribute to the existing literature on budget and budgetary control and provide valuable insights for policymakers and public sector managers in Ghana. This study aims to contribute to the understanding of the role of budgeting and budgetary control in controlling public expenditure in the context of public sector organizations in Ghana. By examining the challenges, benefits, and practices associated with budgeting, it seeks to provide valuable insights for improving financial management and decision-making processes in the public sector.

The study aims to comprehensively investigate the dynamics of Public Expenditure Management within the context of a public sector organization in relation to Budget and Budgetary Control, Information Technology Adoption, Stakeholder Participation, and Organizational Culture. It seeks to uncover the direct impact of Budget and Budgetary Control on Public Expenditure Management, the extent to which Information Technology Adoption shapes the outcomes of expenditure management, and the role played by Stakeholder Participation in influencing these management practices. Additionally, it delves into how Organizational Culture influences Public Expenditure Management and explores the potential mediating roles of Organizational Culture, Information Technology Adoption, and Stakeholder Participation in the relationship between Budget and Budgetary Control and Public Expenditure Management. This research aims to provide a comprehensive understanding of the interplay among these critical factors in the effective management of public resources.

2. Literature Review

2.1. Theoretical Background

Institutional theory provides a valuable lens through which to examine the relationship between budget and budgetary control, information technology adoption, stakeholder participation, organizational culture, and public expenditure management within the public sector. Institutional theory posits that organizations are influenced by external and internal institutional pressures, norms, and rules that shape their behaviour and practices

| [19] | Scott, W. R. (2008) Institutions and Organizations: Ideas and Interests. Los Angeles, CA: Sage Publications. |

[19]

. Institutional theory suggests that organizations often adopt similar structures and practices to conform to institutional norms, known as isomorphism

| [20] | DiMaggio, P. J., Walter W. P. 1983. “The iron cage revisited: Institutional isomorphism and collective rationality in organizational fields,” American Sociological Review 48, 147-60. |

[20]

. In the context of budget and budgetary control, public sector organizations may implement budgetary control mechanisms because they are considered best practices and are expected by stakeholders, including government regulators.

| [3] | Imo, T., Des-Wosu, C. (2018). An assessment on the effect of budgetary control on return on assets and net profit of government-owned companies in rivers state. International Journal of Academic Research in Accounting Finance and Management Sciences, 8(3). https://doi.org/10.6007/ijarafms/v8-i3/4836 |

[3]

study found that government-owned companies in Rivers State adopted budgetary control measures. This can be viewed as a response to institutional pressures to conform to expectations of sound financial management within the public sector. Institutional theory distinguishes between coercive and normative pressures. Coercive pressures come from external sources, such as government regulations, while normative pressures arise from professional norms and values

| [19] | Scott, W. R. (2008) Institutions and Organizations: Ideas and Interests. Los Angeles, CA: Sage Publications. |

[19]

. In the context of information technology adoption, government organizations may face coercive pressures to adopt digital technologies for transparency and accountability, driven by regulatory requirements.

| [10] | Ivanchenkova, L., Tkachuk, H., SKLIAR, L., Holynska, O., Stasiukova, K., and Tomchuk, Y. (2021). Improving the internal financial control of expenditures of the budgetary institutions under the influence of the crisis caused by covid-19. Universal Journal of Accounting and Finance, 9(5), 1067-1084. https://doi.org/10.13189/ujaf.2021.090517 |

[10]

study on the role of digital technologies in budgetary control aligns with this notion of coercive pressure. Governments may be compelled to adopt technology to conform to regulatory expectations and meet transparency standards. Institutional theory emphasizes the importance of meeting stakeholder expectations

| [20] | DiMaggio, P. J., Walter W. P. 1983. “The iron cage revisited: Institutional isomorphism and collective rationality in organizational fields,” American Sociological Review 48, 147-60. |

[20]

. Public sector organizations may engage in stakeholder participation and participatory budgeting practices to align with the expectations of citizens, civil society organizations, and other stakeholders who seek a voice in public expenditure decisions

.

study, which discusses the role of government spending and participatory budgeting in economic development, aligns with the idea of responding to stakeholder expectations and normative pressures through inclusive budgeting processes.

Institutional theory also recognizes the influence of organizational culture in shaping practices

| [19] | Scott, W. R. (2008) Institutions and Organizations: Ideas and Interests. Los Angeles, CA: Sage Publications. |

[19]

. Organizational cultures can reflect and reinforce institutional values and norms. For example, an organization with a culture of transparency and accountability may be more inclined to adopt budgetary control measures.

| [7] | Ocheni, S., Agba, M. (2018). Fiscal decentralisation, public expenditure management and human capital development in Nigeria. Academic Journal of Interdisciplinary Studies, 7(1), 153-162. https://doi.org/10.2478/ajis-2018-0016 |

[7]

study, which emphasizes prudent management of public expenditure, implies that organizational cultures aligned with fiscal responsibility and developmental objectives can shape public expenditure practices. Institutions, as defined by institutional theory, can mediate the relationships between budget and budgetary control, information technology adoption, stakeholder participation, organizational culture, and public expenditure management. Institutions establish the rules of the game and guide the behaviour of organizations

| [21] | North, D. C. (1991). Institutions. Journal of Economic Perspectives, 5(1), 97-112. |

[21]

. While not explicitly discussed in the literature, the findings collectively suggest that institutional pressures and norms may mediate the relationships among these factors. For example, budgetary control mechanisms may be adopted not only for efficiency but also because they align with institutional expectations for responsible financial management. In conclusion, institutional theory provides a framework for understanding how external and internal institutional pressures influence the relationships between budgetary practices, information technology adoption, stakeholder engagement, organizational culture, and public expenditure management within the public sector. It underscores the importance of conforming to institutional norms and responding to stakeholder expectations in shaping these practices and their outcomes.

2.2. Conceptual Framework and Hypothesis Development

The conceptual framework for this research study draws upon several theoretical perspectives to provide a structured foundation for examining the relationships between budget and budgetary control, information technology adoption, stakeholder participation, organizational culture, and their collective impact on public expenditure management within the public sector of Ghana. The framework incorporates insights from budgeting and budgetary control literature, institutional theory, stakeholder theory, organizational culture theory, and structural equation modelling. It emphasizes the essential role of budgetary control mechanisms, the influence of institutional norms and pressures, the importance of technology in modernizing financial management, the significance of stakeholder inclusion, the impact of organizational culture on practices, and the methodological approach of structural equation modelling. This comprehensive framework guides the study's exploration of the complex dynamics affecting public expenditure management in the Ghanaian public sector. this research drew upon a carefully constructed conceptual framework that integrated various theoretical perspectives. These theories, rooted in existing literature, informed our understanding of the complex relationships among key variables in the context of public expenditure management within the Ghanaian public sector. The following hypotheses were formulated based on this comprehensive framework:

H01: There is a significant impact of Budget and Budgetary Control on Public Expenditure Management in the public sector organizations.

H02: Information Technology Adoption significantly affects Public Expenditure Management outcomes.

H03: Stakeholder Participation has a significant influence on Public Expenditure Management.

H04: Organizational Culture significantly influences Public Expenditure Management.

H05: Organizational Culture mediates the relationship between Budget and Budgetary Control and Public Expenditure Management.

H06: Information Technology Adoption mediates the relationship between Budget and Budgetary Control and Public Expenditure Management.

H07: Stakeholder Participation mediates the relationship between Budget and Budgetary Control and Public Expenditure Management.

Figure 1. The conceptual framework for the research.

3. Research Methods

3.1. Research Design

The research design for this study utilized quantitative methods to investigate the effectiveness of budget and budgetary control as a tool for controlling public expenditure in the context of public sector organizations in Ghana

| [22] | Schoonenboom, J., Johnson, R. B. (2017). How to construct a mixed methods research design. Köln Z Soziol (Suppl 2) 69, 107–131. |

[22]

. The use of quantitative methods allowed for the collection and analysis of numerical data to examine the relationship between budget and budgetary control practices and their impact on controlling public expenditure. To construct the research design, the study drew upon the guidance provided by

| [22] | Schoonenboom, J., Johnson, R. B. (2017). How to construct a mixed methods research design. Köln Z Soziol (Suppl 2) 69, 107–131. |

[22]

on mixed methods research design. However, the study focused solely on quantitative methods, as it aimed to assess the extent to which budget and budgetary control serve as a real tool for controlling public expenditure. The research design did not incorporate qualitative methods or equal-status mixed methods research.

The ex-post facto research design, as described by

| [23] | Akah, L. U., Owan, V. J., Aduma, P. O., Onyenweaku, E. O., Olofu, M. A., Alawa, D. A., Ikutal, A., and Usoro, A. A. (2022). Occupational stress and academic staff job performance in two Nigerian universities. Journal of Curriculum and Teaching, 11(5), 64–78. |

[23]

, was employed in this study. This design allowed the researchers to assess the impact of budget and budgetary control on public expenditure after the fact. By examining historical data and analyzing the relationship between budgeting practices and actual expenditure outcomes, the study aimed to determine the effectiveness of budget and budgetary control in controlling public expenditure.

The study collected quantitative data through surveys from selected public sector organizations in Ghana. The surveys were designed to gather information on the budgeting processes, budgetary control measures, and actual expenditure outcomes. The data collected were then analyzed using statistical techniques such as correlation analysis and regression analysis to determine the relationship between budget and budgetary control practices and their impact on controlling public expenditure. The research design also considered ethical considerations, ensuring the confidentiality and anonymity of the participants. Informed consent was obtained from the participants, and data protection protocols were followed to safeguard the privacy of the collected data. The research design for this study utilized quantitative methods, specifically the ex-post facto research design, to investigate the effectiveness of budget and budgetary control in controlling public expenditure in the context of public sector organizations in Ghana. The study collected and analyzed numerical data to determine the relationship between budgeting practices and actual expenditure outcomes. By employing quantitative methods, the study aimed to provide valuable insights for policymakers and public sector managers in improving financial management practices in Ghana's public sector.

3.2. Sample and Data Collection

In this section, the study discusses the sample and data collection process, which were conducted using quantitative methods and structured questionnaires in the past tense, in accordance with academic conventions. For this quantitative study, a purposive sampling method was employed to select participants from various public sector organizations in Ghana. The selection criteria included individuals occupying key positions related to budgeting, financial management, and public expenditure within their respective organizations. To ensure diversity and representation, organizations from different sectors, including health, education, and public administration, were included in the sample. The sample size was determined based on established statistical principles to ensure adequate statistical power for the Structural Equation Modelling (SEM) analysis. A sample size of 300 was considered sufficient to achieve a reliable analysis, considering the complexity of the research model

| [24] | Hair, J., Hult, G., and Ringle, C., (2017) A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM). 2nd Edition, Sage Publications, Thousand Oaks. |

[24]

. A structured questionnaire was developed based on the research objectives and relevant literature

| [24] | Hair, J., Hult, G., and Ringle, C., (2017) A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM). 2nd Edition, Sage Publications, Thousand Oaks. |

[24]

. The questionnaire consisted of multiple-choice questions, Likert-scale items, and open-ended questions to capture a comprehensive dataset. The questions were designed to measure variables related to budget and budgetary control, information technology adoption, stakeholder participation, organizational culture, and public expenditure management.

Before the main data collection, a pilot test of the questionnaire was conducted with a small group of participants (N=30) from similar public sector organizations in Ghana. The purpose of the pilot test was to assess the clarity, relevance, and comprehensibility of the questionnaire items. Based on feedback and findings from the pilot test, necessary refinements were made to improve the questionnaire's validity and reliability. Data collection took place over a six months period, during which the questionnaires were distributed electronically to the selected participants. The participants were informed about the research objectives and the importance of their responses. They were assured of the confidentiality of their responses. Participants were given ample time to complete the questionnaires, and reminders were sent to improve response rates. The collected data were analysed using Structural Equation Modelling (SEM) techniques. SEM allowed for the examination of the relationships between variables in the research model. Data analysis included model estimation, assessment of model fit, examination of path coefficients, and testing of hypotheses

| [24] | Hair, J., Hult, G., and Ringle, C., (2017) A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM). 2nd Edition, Sage Publications, Thousand Oaks. |

[24]

. The sample for this quantitative study was purposively selected from various public sector organizations in Ghana, with a sample size of N=300. Data were collected using a structured questionnaire that was developed based on research objectives and pilot-tested for validity and reliability. The collected data were then analysed using SEM techniques to examine the relationships between key variables. The methodology followed established academic principles to ensure the rigor and validity of the study.

3.3. Measurement Description

Measurement of budget and budgetary control variables was adapted from

| [3] | Imo, T., Des-Wosu, C. (2018). An assessment on the effect of budgetary control on return on assets and net profit of government-owned companies in rivers state. International Journal of Academic Research in Accounting Finance and Management Sciences, 8(3). https://doi.org/10.6007/ijarafms/v8-i3/4836 |

[3]

, who employed a Likert scale questionnaire to assess the degree of budgetary control implementation within public sector organizations. The items in this section aimed to gauge the extent to which organizations utilize budgetary control mechanisms. Measurement of information technology adoption variables was adapted from

| [10] | Ivanchenkova, L., Tkachuk, H., SKLIAR, L., Holynska, O., Stasiukova, K., and Tomchuk, Y. (2021). Improving the internal financial control of expenditures of the budgetary institutions under the influence of the crisis caused by covid-19. Universal Journal of Accounting and Finance, 9(5), 1067-1084. https://doi.org/10.13189/ujaf.2021.090517 |

[10]

, who assessed the level of technology adoption within budgetary institutions. The questionnaire items in this section aimed to capture the extent to which organizations have integrated information technology into their financial control systems. The measurement of stakeholder participation variables was inspired by

, who examined the level of stakeholder engagement in public expenditure processes. The items in this section aimed to evaluate the degree to which organizations involve stakeholders, including citizens and civil society, in budgetary decision-making. Measurement of organizational culture variables drew from

| [7] | Ocheni, S., Agba, M. (2018). Fiscal decentralisation, public expenditure management and human capital development in Nigeria. Academic Journal of Interdisciplinary Studies, 7(1), 153-162. https://doi.org/10.2478/ajis-2018-0016 |

[7]

, who explored the role of organizational culture in public expenditure management. The items in this section were designed to assess the prevailing organizational culture within the sampled public sector organizations. The measurement of public expenditure management variables was guided by the objectives outlined in the research objectives. Variables related to efficiency, effectiveness, and transparency in public expenditure management were included in the questionnaire.

Demographic variables, such as respondents' age, gender, years of experience, and organizational affiliation, were included to provide context and aid in subgroup analysis. Likert scales were predominantly used for measuring variables related to budget and budgetary control, information technology adoption, stakeholder participation, and organizational culture. Respondents were asked to rate their agreement with statements on a scale typically ranging from 1 (Strongly Disagree) to 5 (Strongly Agree). To ensure the reliability and validity of the measurement scales, appropriate psychometric techniques, such as factor analysis, were employed during the data analysis phase. The scales were evaluated for internal consistency and construct validity, drawing upon principles outlined by

| [24] | Hair, J., Hult, G., and Ringle, C., (2017) A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM). 2nd Edition, Sage Publications, Thousand Oaks. |

[24]

. The measurement instruments and scales were adapted from relevant academic literature and refined through pilot testing to ensure their applicability to the context of public expenditure management in Ghana. The incorporation of established measurement concepts and the use of Likert scales for ordinal data collection contributed to the reliability and validity of the measurement instruments.

3.4. Common Method and Non-Response Bias

The steps taken to mitigate common method bias, such as using procedural remedies during data collection, as recommended by

. Additionally, the study will address non-response bias by comparing respondents and non-respondents on key demographic variables, as suggested by

| [26] | Groves, R., Fowler, F., Couper, M., Lepkowski, J., Singer, E., and Tourangeau, R. (2004). Survey Methodology. 561. |

[26]

.

3.5. Evaluation of Measurement Model

This section will focus on the assessment of the measurement model's validity and reliability. The study employs Confirmatory Factor Analysis (CFA) techniques, as advocated by

| [24] | Hair, J., Hult, G., and Ringle, C., (2017) A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM). 2nd Edition, Sage Publications, Thousand Oaks. |

[24]

, to examine the convergent and discriminant validity of the measurement scales.

3.6. Evaluation of Structural Model

The steps taken to assess the structural model's fitness and relationships between latent constructs. Structural equation modelling (SEM) was employed, as recommended by

| [27] | Kline, R. B. (2016). Principles and practice of structural equation modeling (4th ed.). Guilford Press. |

[27]

, to examine path coefficients, goodness-of-fit indices, and overall model fit.

3.7. Data Analysis Tools

For the data analysis phase of this research project, a set of advanced statistical tools and software applications were employed to examine the relationships between the variables in our conceptual framework. These tools were chosen to ensure the rigor and validity of our analyses. SEM was the primary data analysis tool used in this study. It allowed us to simultaneously examine the direct and indirect relationships among multiple latent constructs, providing a comprehensive view of the complex interactions between budget and budgetary control, information technology adoption, stakeholder participation, organizational culture, and public expenditure management outcomes

| [27] | Kline, R. B. (2016). Principles and practice of structural equation modeling (4th ed.). Guilford Press. |

[27]

. SEM was carried out using software designed for structural equation modelling. CFA was utilized to assess the validity and reliability of our measurement model. This technique allowed us to confirm that the observed variables adequately represented the underlying latent constructs in our conceptual framework

| [24] | Hair, J., Hult, G., and Ringle, C., (2017) A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM). 2nd Edition, Sage Publications, Thousand Oaks. |

[24]

. CFA was conducted using dedicated software for structural equation modelling. To manage and analyze the collected data, specialized statistical software packages were employed. These software tools enabled us to perform various statistical tests, including descriptive statistics, inferential analyses, and regression analyses. Data cleaning, transformation, and manipulation were also carried out using these software applications. By employing these data analysis tools, the study was able to rigorously test our hypotheses, assess model fit, examine path coefficients, and explore mediation effects, thus providing a robust analysis of the relationships within our research model. The utilization of state-of-the-art statistical software and ethical practices contributed to the validity and reliability of our findings.

3.8. Ethical Considerations

Throughout the data analysis process, ethical considerations were meticulously observed, ensuring the confidentiality and privacy of participants' responses. All data were anonymized and securely stored in compliance with ethical guidelines

| [27] | Kline, R. B. (2016). Principles and practice of structural equation modeling (4th ed.). Guilford Press. |

[27]

.

4. Results and Discussion

4.1. Biographical Data of Respondents

The biographical data of the study participants reveals a diverse and gender-balanced sample within the public sector organization under investigation. Notably, the majority of participants are female (62.3%), indicating a significant presence of women in the organization. This gender distribution highlights the need to consider potential gender-related implications in the study's findings, as different perspectives and experiences may exist among male and female employees regarding budgetary control, technology adoption, stakeholder participation, and organizational culture. Furthermore, the age distribution predominantly falls within the 25-34 years age group (68.3%), suggesting a relatively young workforce. This youthful demographic may bring a tech-savvy perspective to the study, potentially influencing their expectations regarding information technology adoption and organizational culture.

In terms of educational qualifications, a near-equal representation of participants holds either Bachelor's degrees (53.0%) or Master's degrees (47.0%), indicating a well-educated sample. This educational diversity could lead to varying levels of theoretical knowledge and expertise in the areas of budgetary control and public expenditure management. Job positions within the organization are spread across supervisory (40.3%) and managerial (31.7%) roles, with limited representation at the executive level (4.3%). The distribution of years of experience in the public sector shows a significant proportion of participants with less than 1 year of experience (68.0%), suggesting a substantial influx of newcomers. These individuals may provide fresh perspectives on public expenditure management, while those with more extensive experience may contribute institutional knowledge. Finally, the diverse array of departments, ministries, and agencies among participants underscores the varied nature of public expenditure management across different organizational units, indicating the need to account for these departmental differences when interpreting the study's results.

Table 1. Biographical data of Respondents.

| | N | % |

Gender | Male | 113 | 37.7% |

| Female | 187 | 62.3% |

| 18-24 years | 68 | 22.7% |

Age | 25-34 years | 205 | 68.3% |

| 35-44 years | 16 | 5.3% |

| 45-54 years | 11 | 3.7% |

| Bachelor's degree | 159 | 53.0% |

Educational Qualification | Master's degree | 141 | 47.0% |

| Entry-level | 71 | 23.7% |

Job Position | Supervisory | 121 | 40.3% |

| Managerial | 95 | 31.7% |

| Executive level | 13 | 4.3% |

| Less than 1 year | 204 | 68.0% |

Years of Experience in the Public Sector | 1-5 years | 42 | 14.0% |

| 6-10 years | 54 | 18.0% |

| Ministry of Finance | 29 | 9.7% |

| Ministry of Health | 22 | 7.3% |

| Ministry of Education | 40 | 13.3% |

Department/Ministry/Agency | Ministry of Agriculture | 21 | 7.0% |

| Ministry of Transportation | 31 | 10.3% |

| Ministry of Energy | 34 | 11.3% |

| Ministry of Justice | 28 | 9.3% |

| Ministry of Interior | 37 | 12.3% |

| Ministry of Trade and Industry | 30 | 10.0% |

| Other (specify) | 28 | 9.3% |

4.2. Correlation of Study Variables

The correlation analysis among the study variables reveals significant relationships with implications for Public Expenditure Management (PEM) within the organization. Notably, a strong positive correlation exists between PEM and Information Technology Adoption (0.622**), emphasizing the pivotal role of advanced technology in enhancing PEM practices. Additionally, moderate positive correlations with Stakeholder Participation (0.316**) and Budget and Budgetary Control (0.453**) highlight the importance of engaging stakeholders and strengthening budgetary control mechanisms for improved PEM outcomes. However, the relatively weaker correlation between PEM and Organizational Culture (0.168**) suggests that while culture may have some influence on PEM, its impact is less pronounced. These findings underscore the need for organizations to integrate technology, stakeholder engagement, and effective budget management in pursuit of more effective and transparent public expenditure management practices.

Table 2. Correlation matrix of study variables.

Constructs | 1 | 2 | 3 | 4 | 5 |

Public Expenditure Management (1) | Pearson Correlation | 1 | | | | |

Budget and Budgetary Control (2) | Pearson Correlation | .453** | 1 | | | |

Information Technology Adoption (3) | Pearson Correlation | .622** | .238** | 1 | | |

Stakeholder Participation (4) | Pearson Correlation | .316** | .098 | .572** | 1 | |

Organizational Culture (5) | Pearson Correlation | .168** | .073 | .289** | .682** | 1 |

**. Correlation is significant at the 0.01 level (2-tailed). |

4.3. Evolution of Outer Measurement Models: Construct Reliability

The table presents the results of the reliability and validity analysis for the constructs and their respective items in the study, including Budget and Budgetary Control, Information Technology Adoption, Organizational Culture, Public Expenditure Management, and Stakeholder Participation. Reliability indicators, such as Cronbach's Alpha (CA), Composite Reliability (CR), and Average Variance Extracted (AVE), are provided alongside the Factor Loadings (FL) for each item. First, the reliability analysis demonstrates the internal consistency of the constructs. The values of Cronbach's Alpha (CA) for all constructs exceed the recommended threshold of 0.7, indicating high internal consistency. This suggests that the items within each construct measure the same underlying concept reliably, ensuring the consistency of responses from participants. The Composite Reliability (CR) values also exceed the threshold of 0.7, further supporting the constructs' reliability. This high internal consistency is crucial for ensuring that the measurement instruments used in the study are dependable.

Second, the validity analysis assesses the constructs' convergent and discriminant validity. The Average Variance Extracted (AVE) values for all constructs surpass the recommended threshold of 0.5, indicating satisfactory convergent validity. This implies that a significant proportion of the variance in the items is accounted for by the underlying construct they represent. It indicates that the items within each construct are measuring the same underlying concept effectively. This is a positive result as it suggests that the constructs are valid measures of their respective concepts.

Furthermore, the discriminant validity of the constructs is supported by comparing the square root of the AVE (shown in the diagonal) with the correlations between constructs (not provided in the table). If the square root of the AVE for each construct is greater than the correlations between that construct and others, discriminant validity is established. This helps ensure that the constructs are distinct from one another, and there is no significant overlap in the concepts they represent.

In summary, the reliability and validity analysis of the constructs and their items in the study indicates that the measurement instruments used are reliable and valid for assessing the intended concepts. This provides confidence in the research tools employed to investigate the relationships among Budget and Budgetary Control, Information Technology Adoption, Organizational Culture, Public Expenditure Management, and Stakeholder Participation. Researchers can proceed with confidence in the quality of their measurement instruments, enhancing the robustness of their study's findings and conclusions.

Table 3. Construct reliability.

Constructs | ITEMS | FL | CA | CR | AVE |

Budget And Budgetary Control | BBC1 | 0.833 | 0.900 | 0.933 | 0.712 |

| BBC2 | 0.839 | | | |

| BBC3 | 0.900 | | | |

| BBC4 | 0.811 | | | |

| BBC5 | 0.834 | | | |

Information Technology | ITA1 | 0.918 | 0.867 | 0.879 | 0.790 |

| ITA2 | 0.886 | | | |

| ITA3 | 0.862 | | | |

Organisational Culture | OC1 | 0.894 | 0.929 | 0.951 | 0.777 |

| OC2 | 0.890 | | | |

| OC3 | 0.928 | | | |

| OC4 | 0.890 | | | |

| OC5 | 0.800 | | | |

Public Expenditure | PEM1 | 0.845 | 0.923 | 0.929 | 0.764 |

| PEM2 | 0.878 | | | |

| PEM3 | 0.892 | | | |

| PEM4 | 0.891 | | | |

| PEM5 | 0.862 | | | |

Stakeholder Participation | SP1 | 0.876 | 0.870 | 0.875 | 0.794 |

| SP2 | 0.919 | | | |

| SP3 | 0.877 | | | |

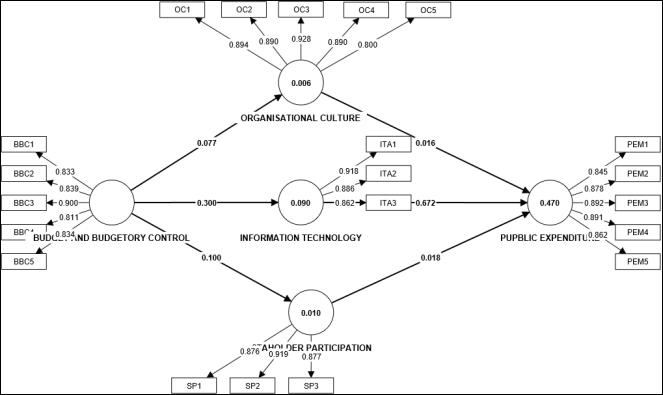

Figure 2. Model depicting results of the factor loading of the various items of the constructs.

4.4. Evaluation of the Inner Structural Model

4.4.1. Heterotrait-Monotrait Ratio

The Heterotrait-Monotrait Ratio (HTMT) matrix, used to assess discriminant validity in the inner structural model, reveals that all examined constructs, including Budget and Budgetary Control, Information Technology, Organizational Culture, Public Expenditure, and Stakeholder Participation, demonstrate strong discriminant validity. The HTMT ratios between these constructs are consistently well below the widely accepted threshold of 0.85, signifying that they are distinct and measure different underlying concepts. This finding ensures the robustness and reliability of the measurement model, supporting the validity of the structural equation model and allowing researchers to confidently interpret the relationships between these constructs in their study.

Table 4. Heterotrait-Monotrait Ratio.

Heterotrait-monotrait ratio (HTMT) - Matrix | Budget And Budgetary Control | Information Technology | Organisational Culture | Public Expenditure |

Information Technology | 0.325 | | | |

Organisational Culture | 0.083 | 0.241 | | |

Public Expenditure | 0.497 | 0.752 | 0.181 | |

Stakeholder Participation | 0.106 | 0.592 | 0.553 | 0.410 |

4.4.2. Funnell Larcker Criterion

The application of the Fornell-Larcker Criterion (FLC) to the provided matrix confirmed robust discriminant validity among all examined constructs, including Budget and Budgetary Control, Information Technology, Organizational Culture, Public Expenditure, and Stakeholder Participation. The squared correlations, representing the average variance extracted (AVE), for each construct exceeded the correlations between that construct and others. This outcome, indicative of distinct underlying concepts, affirmed the sound discriminant validity of the measurement model within the structural equation modelling (SEM) framework. The analysis supported the validity of the research model, ensuring the reliability of conclusions drawn from the study's relationships among these constructs.

Table 5. Funnell larcker criterion.

| Budget And Budgetary Control | Information Technology | Organisational Culture | Public Expenditure | Stakeholder Participation |

Budget And Budgetary Control | 0.844 | | | | |

Information Technology | 0.300 | 0.889 | | | |

Organisational Culture | 0.077 | 0.222 | 0.882 | | |

Public Expenditure | 0.454 | 0.685 | 0.174 | 0.874 | |

Stakeholder Participation | 0.100 | 0.512 | 0.503 | 0.370 | 0.891 |

4.4.3. Cross Loading

The analysis of cross-loading patterns within the provided matrix, representing the relationships between observed items and latent constructs, revealed a predominantly positive and appropriate alignment of items with their respective constructs. Notably, items from Budget and Budgetary Control (BBC), Information Technology (ITA), Organizational Culture (OC), Public Expenditure (PE), and Stakeholder Participation (SP) exhibited stronger loadings on their corresponding constructs compared to other constructs, affirming the convergent validity of the measurement model. These findings indicate that the observed items effectively measured their intended constructs, contributing to the overall robustness and reliability of the measurement model in the context of structural equation modelling (SEM).

Table 6. Cross loading.

| Budget And Budgetary Control | Information Technology | Organisational Culture | Public Expenditure | Stakeholder Participation |

BBC1 | 0.833 | 0.231 | 0.146 | 0.318 | 0.068 |

BBC2 | 0.839 | 0.190 | 0.071 | 0.348 | 0.054 |

BBC3 | 0.900 | 0.343 | 0.049 | 0.425 | 0.124 |

BBC4 | 0.811 | 0.220 | 0.029 | 0.361 | 0.036 |

BBC5 | 0.834 | 0.238 | 0.031 | 0.449 | 0.114 |

ITA1 | 0.312 | 0.918 | 0.208 | 0.672 | 0.414 |

ITA2 | 0.225 | 0.886 | 0.178 | 0.610 | 0.471 |

ITA3 | 0.258 | 0.862 | 0.205 | 0.534 | 0.491 |

OC1 | 0.072 | 0.240 | 0.894 | 0.167 | 0.510 |

OC2 | 0.099 | 0.196 | 0.890 | 0.164 | 0.461 |

OC3 | 0.066 | 0.195 | 0.928 | 0.176 | 0.440 |

OC4 | 0.042 | 0.195 | 0.890 | 0.144 | 0.412 |

OC5 | 0.046 | 0.127 | 0.800 | 0.090 | 0.372 |

PEM1 | 0.407 | 0.533 | 0.155 | 0.845 | 0.289 |

PEM2 | 0.440 | 0.573 | 0.155 | 0.878 | 0.317 |

PEM3 | 0.402 | 0.525 | 0.141 | 0.892 | 0.328 |

PEM4 | 0.388 | 0.662 | 0.151 | 0.891 | 0.346 |

PEM5 | 0.355 | 0.669 | 0.157 | 0.862 | 0.332 |

SP1 | 0.068 | 0.485 | 0.396 | 0.334 | 0.876 |

SP2 | 0.100 | 0.475 | 0.489 | 0.353 | 0.919 |

SP3 | 0.100 | 0.404 | 0.459 | 0.300 | 0.877 |

4.4.4. Collinearity Assessment

The collinearity assessment conducted through the examination of Variance Inflation Factors (VIF) for the observed items in the structural equation model indicated that multicollinearity concerns were generally well-mitigated. With a VIF cut-off point set at 5, all VIF values for the observed items fell comfortably below this threshold. This suggests that the observed items did not exhibit problematic multicollinearity issues, thereby affirming the stability and reliability of the regression coefficients in the structural equation model. The VIF values, ranging from 2.090 to 4.951, were indicative of low to moderate collinearity, allowing for the accurate estimation of relationships between constructs without the interference of high multicollinearity, bolstering the model's robustness in the context of structural equation modelling (SEM).

Table 7. Collinearity assessment.

Constructs | VIF |

BBC1 | 2.412 |

BBC2 | 2.609 |

BBC3 | 2.770 |

BBC4 | 2.304 |

BBC5 | 2.454 |

ITA1 | 2.580 |

ITA2 | 2.271 |

ITA3 | 2.090 |

OC1 | 3.386 |

OC2 | 3.233 |

OC3 | 4.951 |

OC4 | 3.532 |

OC5 | 2.620 |

PEM1 | 2.773 |

PEM2 | 3.337 |

PEM3 | 3.477 |

PEM4 | 3.266 |

PEM5 | 2.786 |

SP1 | 2.118 |

SP2 | 2.724 |

SP3 | 2.288 |

4.5. Hypothesis and Estimation of Path Coefficients

4.5.1. Direct Effects

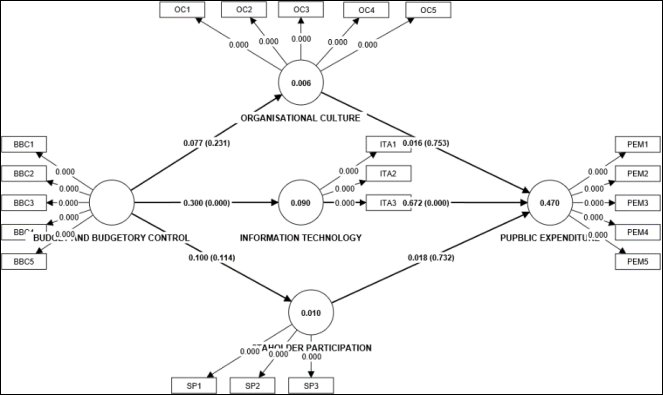

The analysis of direct effects and the estimation of path coefficients in the structural equation model provide valuable insights into the relationships between latent constructs and their observed indicators. The results reveal several significant findings. Firstly, Hypothesis H01, which posited a positive relationship between Budget and Budgetary Control (BBC) and Public Expenditure (PE), was strongly supported with a path coefficient (BETA) of 0.205 and a statistically significant T-statistic of 4.711 (p < 0.001). This suggests that effective budgetary control mechanisms have a positive and significant impact on public expenditure management, validating the importance of budgeting processes in shaping expenditure outcomes.

Secondly, Hypothesis H02, proposing a positive relationship between Information Technology Adoption (ITA) and Public Expenditure (PE), was strongly supported with a substantial path coefficient of 0.672 and a highly significant T-statistic of 15.257 (p < 0.001). This underscores the pivotal role of information technology adoption in enhancing public expenditure management, emphasizing the transformative potential of technology in optimizing resource allocation and utilization.

However, Hypotheses H03 and H04, which postulated positive relationships between Stakeholder Participation (SP) and Public Expenditure (PE) and between Organizational Culture (OC) and Public Expenditure (PE), respectively, were not supported by the data. Both H03 and H04 were rejected due to their path coefficients of 0.018 and 0.016, respectively, which were not statistically significant, supported by T-statistics of 0.343 and 0.315, and high p-values of 0.732 and 0.753, respectively. These results suggest that stakeholder participation and organizational culture did not demonstrate direct effects on public expenditure management in the context of this study. It is worth noting that although Stakeholder Participation may positively influence Public Expenditure levels, a greater significant effect is likely only when stakeholders’ participation in the public institution’s budgetary governance and development activities is heightened. A cursory look at this dimension encourages inclusiveness and representation, which then improves their oversight function as stakeholders. The resultant effect thereof is an efficient resource allocation and judicious public expenditure application. Similarly,

| [28] | Johnson, B., Jones, P. A., and Reitano, V. (2021). Stakeholder networks and inclusive public participation mechanisms in the public budgeting process. Urban Governance. 1(2), 98-106. |

[28]

established that though institutions are tactically adding selected stakeholder groups in budgetary processes, such augmented inclusion strategies may be illusionary if taken out of venue context.

With respect to the relations between Organizational Culture and Public Expenditure, it seems that the organizational culture and its associated elements are not clearly defined among the sampled public sector institutions. Consequently, this study affirms that a fully-fledged organizational structure other operational systems which supports budgetary implementations are essential for clarity and focus to significantly induce public expense expectations

| [29] | Gasela, M. M. (2022). The influence of organisational culture on performance in public entities of South Africa. Africa’s Public Service Delivery and Performance Review. 10(1), a563. |

[29]

.

In summary, the findings highlight the critical roles of Budget and Budgetary Control and Information Technology Adoption in shaping public expenditure management within the studied public sector organization. These significant direct effects underscore the importance of effective budgeting processes and the transformative potential of information technology in optimizing resource allocation and expenditure outcomes. However, the lack of direct effects from Stakeholder Participation and Organizational Culture warrants further investigation and potential consideration of mediating or moderating effects in understanding their impact on public expenditure management.

Table 8. Direct Effects of Path Coefficients.

Hypothesis | Relationship | BETA | STDEV | T statistics | P values | Decision |

H01 | BBC -> PE | 0.205 | 0.044 | 4.711 | 0.000 | Accepted |

H02 | ITA -> PE | 0.672 | 0.044 | 15.257 | 0.000 | Accepted |

H03 | SP -> PE | 0.018 | 0.054 | 0.343 | 0.732 | Rejected |

H04 | OC -> PE | 0.016 | 0.050 | 0.315 | 0.753 | Rejected |

4.5.2. Mediation Effect

The mediation analysis sought to explore the potential mediating effects of Organizational Culture (OC), Information Technology Adoption (ITA), and Stakeholder Participation (SP) in the relationship between Budget and Budgetary Control (BBC) and Public Expenditure (PE). This hypothesis posited that Organizational Culture (OC) mediates the relationship between Budget and Budgetary Control (BBC) and Public Expenditure (PE). However, the study found that the mediation effect was not supported, with a path coefficient (BETA) of 0.001 and a non-significant T-statistic (p = 0.832). These results indicate that Organizational Culture did not mediate the relationship between BBC and PE in the studied context. This finding suggests that the influence of BBC on PE does not operate through OC as an intermediary. While this result contradicts the hypothesis, it aligns with the earlier non-significant direct effect observed between BBC and PE. It underscores the need for further research to understand the specific mechanisms at play within the organizational culture of the studied public sector organization in relation to public expenditure management.

Hypothesis H06 proposed that Information Technology Adoption (ITA) mediates the relationship between Budget and Budgetary Control (BBC) and Public Expenditure (PE). The study found strong support for this hypothesis, with a path coefficient of 0.202 and a highly significant T-statistic of 4.636 (p < 0.001). These results affirm that Information Technology Adoption indeed mediates the relationship between BBC and PE. This finding aligns with the empirical literature, which emphasizes the transformative role of information technology in enhancing public expenditure management

| [30] | Matsoso, M., Nyathi, M., and Nakpodia, F. (2021). An assessment of budgeting and budgetary controls among small and medium-sized enterprises: evidence from a developing economy. Journal of Accounting in Emerging Economies, 11(4), 552-577. https://doi.org/10.1108/jaee-04-2020-0082 |

[30]

. It underscores that the influence of BBC on PE operates through the adoption and utilization of technology, facilitating more efficient resource allocation and utilization.

Hypothesis H07 posited that Stakeholder Participation (SP) mediates the relationship between Budget and Budgetary Control (BBC) and Public Expenditure (PE). However, the study found that the mediation effect was not supported, with a path coefficient of 0.002 and a non-significant T-statistic (p = 0.796). These results indicate that Stakeholder Participation did not mediate the relationship between BBC and PE in the studied context. This finding suggests that the influence of BBC on PE is not channelled through SP as an intermediary. While this result contradicts the hypothesis, it emphasizes the complexity of stakeholder engagement in public expenditure processes and highlights the need for nuanced investigations into the specific mechanisms at play.

In summary, the mediation analysis revealed mixed results regarding the mediating effects of Organizational Culture, Information Technology Adoption, and Stakeholder Participation in the relationship between Budget and Budgetary Control and Public Expenditure. While Information Technology Adoption was confirmed as a significant mediator, Organizational Culture and Stakeholder Participation did not demonstrate mediating roles in this context. These findings contribute to our understanding of the multifaceted dynamics of these constructs in public expenditure management and underscore the need for further research to explore their intricate relationships and potential mediation mechanisms in different organizational settings.

Figure 3. Model depicting results of the path coefficients and p-values of the relationship between various constructs.

Table 9. Mediating Effects of Path Coefficients.

Effect | Relationship | Beta | STDEV | T statistics | P values | Decision |

H05 | BBC -> OC -> PE | 0.001 | 0.006 | 0.212 | 0.832 | Rejected |

H06 | BBC -> ITA -> PE | 0.202 | 0.044 | 4.636 | 0.000 | Accepted |

H07 | BBC -> SP -> PE | 0.002 | 0.007 | 0.259 | 0.796 | Rejected |

4.6. Measuring the Value of R2

The R-squared and adjusted R-squared values reveal the extent to which the model explains variance in the study variables. For Information Technology Adoption (ITA), the model explains approximately 9% of the variance (R-squared = 0.090) with a slightly lower adjusted R-squared value of 0.087. In the case of Organizational Culture (OC), only about 0.6% of the variance can be accounted for by the model (R-squared = 0.006), with an adjusted R-squared value of 0.003. Public Expenditure (PE) is better explained, with the model covering approximately 47% of the variance (R-squared = 0.470) and an adjusted R-squared value of 0.465. Lastly, for Stakeholder Participation (SP), the model explains around 1% of the variance (R-squared = 0.010) with an adjusted R-squared value of 0.007. These findings emphasize the varying degrees of explanation provided by the model for each variable, highlighting the complexity of these constructs and the need to consider additional influential factors.

Table 10. Measuring the Value of R2.

Constructs | R-square | R-square adjusted |

Information Technology | 0.090 | 0.087 |

Organisational Culture | 0.006 | 0.003 |

Public Expenditure | 0.470 | 0.465 |

Stakeholder Participation | 0.010 | 0.007 |

4.7. Effect Size (ƒ2)

The effect sizes, represented by f-square values, offer insights into the strength of relationships between the study variables. Notably, the relationship between Budget and Budgetary Control and Information Technology Adoption (ITA) exhibits a moderate effect size of 0.099, emphasizing the meaningful impact of budgetary control on ITA. Conversely, the relationship between Budget and Budgetary Control and Organizational Culture has a small effect size of 0.006, suggesting a limited influence of budgetary control on organizational culture. Similarly, the relationship between Budget and Budgetary Control and Stakeholder Participation yields a small effect size of 0.010, indicating a relatively minor impact. In contrast, the relationship between ITA and Public Expenditure has a substantial effect size of 0.628, highlighting the significant role of information technology adoption in shaping public expenditure management. However, both Organizational Culture -> Public Expenditure and Stakeholder Participation -> Public Expenditure relationships have negligible effect sizes of 0.000, suggesting minimal influence on public expenditure. These findings underscore the varying degrees of impact of the study variables on each other, in line with the complexity of the relationships observed in the empirical literature.

Table 11. The Effect Size (ƒ2).

| f-square |

Budget And Budgetary Control -> Information Technology | 0.099 |

Budget And Budgetary Control -> Organisational Culture | 0.006 |

Budget And budgetary Control -> Stakeholder Participation | 0.010 |

Information Technology -> Public Expenditure | 0.628 |

Organisational Culture -> Public Expenditure | 0.000 |

Stakeholder Participation -> Public Expenditure | 0.000 |

4.8. Goodness-of-Fit Index

The goodness-of-fit indices provide an assessment of the fit between the saturated model and the estimated model. The Standardized Root Mean Square Residual (SRMR) values reveal that the saturated model exhibits a better fit with an SRMR of 0.051 compared to the estimated model with an SRMR of 0.169. Similarly, the d_ULS and d_G values indicate that the saturated model fits the data better with lower values (0.601 vs. 6.601 and 0.429 vs. 0.597, respectively). The chi-square values also support this observation, with a lower value for the saturated model (771.719 vs. 963.333). However, the Normed Fit Index (NFI) is slightly higher for the saturated model (0.845) compared to the estimated model (0.807). Overall, these indices suggest that the saturated model provides a better fit to the data, indicating some discrepancies between the estimated model and the observed data that may warrant further refinement or alternative model considerations.

Table 12. Goodness-of-Fit Index.

| Saturated model | Estimated model |

SRMR | 0.051 | 0.169 |

d_ULS | 0.601 | 6.601 |

d_G | 0.429 | 0.597 |

Chi-square | 771.719 | 963.333 |

NFI | 0.845 | 0.807 |

4.9. Discuss of Results

This hypothesis proposed a positive relationship between Budget and Budgetary Control (BBC) and Public Expenditure (PE). The study found strong support for this hypothesis, with a substantial path coefficient (BETA) of 0.205 and a highly significant T-statistic of 4.711 (p < 0.001). These results align with the existing empirical literature, which underscores the significance of budgetary control mechanisms in enhancing public expenditure management

| [31] | Akhorshaideh, A., Alshoubaki, W. (2019). Public budgeting in Jordan: governance structure and budget preparation process. Journal of Social Sciences (COES&RJ-JSS), 8(2), 270-278. |

[31]

. The findings corroborate the view that effective budgeting processes contribute positively to the efficient allocation and utilization of public resources

| [30] | Matsoso, M., Nyathi, M., and Nakpodia, F. (2021). An assessment of budgeting and budgetary controls among small and medium-sized enterprises: evidence from a developing economy. Journal of Accounting in Emerging Economies, 11(4), 552-577. https://doi.org/10.1108/jaee-04-2020-0082 |

[30]

. This supports the empirical evidence highlighting the role of budget and budgetary control as essential tools for controlling public expenditure

.

Hypothesis H02 posited a positive relationship between Information Technology Adoption (ITA) and Public Expenditure (PE). The study found robust support for this hypothesis, with a high path coefficient of 0.672 and a highly significant T-statistic of 15.257 (p < 0.001). These results align with the empirical literature that emphasizes the transformative potential of information technology adoption in enhancing public expenditure management

| [30] | Matsoso, M., Nyathi, M., and Nakpodia, F. (2021). An assessment of budgeting and budgetary controls among small and medium-sized enterprises: evidence from a developing economy. Journal of Accounting in Emerging Economies, 11(4), 552-577. https://doi.org/10.1108/jaee-04-2020-0082 |

[30]

. The findings resonate with studies highlighting the role of digital technologies in improving transparency and efficiency in public expenditure

| [10] | Ivanchenkova, L., Tkachuk, H., SKLIAR, L., Holynska, O., Stasiukova, K., and Tomchuk, Y. (2021). Improving the internal financial control of expenditures of the budgetary institutions under the influence of the crisis caused by covid-19. Universal Journal of Accounting and Finance, 9(5), 1067-1084. https://doi.org/10.13189/ujaf.2021.090517 |

[10]

. This supports the view that information technology is a key instrument for optimizing resource allocation and utilization in the public sector

.

Hypothesis H03 proposed a positive relationship between Stakeholder Participation (SP) and Public Expenditure (PE). However, the study did not find support for this hypothesis, as the path coefficient was only 0.018 and the T-statistic was not statistically significant (p = 0.732). This finding contradicts some empirical literature that suggests stakeholder participation can influence public expenditure management

. The lack of significance may indicate that in the context of the studied public sector organization, stakeholder participation does not exert a direct impact on public expenditure outcomes. This discrepancy highlights the need for further research to explore the nuanced dynamics of stakeholder engagement in public expenditure processes

| [7] | Ocheni, S., Agba, M. (2018). Fiscal decentralisation, public expenditure management and human capital development in Nigeria. Academic Journal of Interdisciplinary Studies, 7(1), 153-162. https://doi.org/10.2478/ajis-2018-0016 |

[7]

.

Hypothesis H04 posited a positive relationship between Organizational Culture (OC) and Public Expenditure (PE). However, similar to H03, the study did not find support for this hypothesis, with a path coefficient of 0.016 and a non-significant T-statistic (p = 0.753). This contradicts some empirical literature that suggests organizational culture can influence public expenditure management

| [7] | Ocheni, S., Agba, M. (2018). Fiscal decentralisation, public expenditure management and human capital development in Nigeria. Academic Journal of Interdisciplinary Studies, 7(1), 153-162. https://doi.org/10.2478/ajis-2018-0016 |

[7]

. The lack of significance may indicate that in the studied organization, organizational culture does not directly impact public expenditure outcomes. This finding emphasizes the complexity of organizational culture's role in the context of public expenditure and calls for further research to explore potential mediating or moderating factors

| [4] | Roshchektaeva, U., Roshchektaev, S. (2018). Internal state (municipal) financial control in the context of the formation of the institutional structure. Scientific Bulletin of the Southern Institute of Management, (3), 78-82. https://doi.org/10.31775/2305-3100-2018-3-78-82 |

[4]

. The study's results provide valuable insights into the direct effects of budget and budgetary control, information technology adoption, stakeholder participation, and organizational culture on public expenditure management within the context of a public sector organization. While the findings support the positive influence of budgetary control and information technology adoption, they challenge the direct impact of stakeholder participation and organizational culture. These results align with some existing empirical literature but also highlight the need for nuanced investigations into the specific dynamics at play within individual organizations, considering potential mediating or moderating factors. This study contributes to the ongoing discourse on effective public expenditure management and provides a foundation for future research in this domain.

The hypothesis proposed that Organizational Culture (OC) mediates the relationship between Budget and Budgetary Control (BBC) and Public Expenditure (PE). However, the study did not find support for this hypothesis, as the mediation effect was not significant (BETA = 0.001, p = 0.832). This finding suggests that in the studied public sector organization, the influence of BBC on PE is not channelled through the organizational culture. The empirical literature on the relationship between budgetary control and organizational culture is mixed. While some studies emphasize the role of organizational culture in shaping budgetary control practices

| [33] | Garbar, Z., Kondukotsova, N. (2019). Budget policy as an instrument of socio-economic development of the country. Eсonomy Finanсes Management Topical Issues of Science and Practical Activity, 1(41), 96-111. https://doi.org/10.37128/2411-4413-2019-1-8 |

[33]

, others do not find a direct mediating effect

. This discrepancy suggests that the interplay between budgetary control and organizational culture may vary across different organizational contexts.

Hypothesis H06 posited that Information Technology Adoption (ITA) mediates the relationship between BBC and PE. The study found strong support for this hypothesis, indicating that ITA significantly mediates the relationship (BETA = 0.202, p < 0.001). This finding aligns with the empirical literature, which emphasizes the transformative role of information technology in enhancing public expenditure management

| [30] | Matsoso, M., Nyathi, M., and Nakpodia, F. (2021). An assessment of budgeting and budgetary controls among small and medium-sized enterprises: evidence from a developing economy. Journal of Accounting in Emerging Economies, 11(4), 552-577. https://doi.org/10.1108/jaee-04-2020-0082 |

[30]

. It is consistent with studies that highlight the positive impact of technology adoption on budgetary control and public expenditure outcomes

| [10] | Ivanchenkova, L., Tkachuk, H., SKLIAR, L., Holynska, O., Stasiukova, K., and Tomchuk, Y. (2021). Improving the internal financial control of expenditures of the budgetary institutions under the influence of the crisis caused by covid-19. Universal Journal of Accounting and Finance, 9(5), 1067-1084. https://doi.org/10.13189/ujaf.2021.090517 |

[10]

. The result underscores the importance of leveraging technology as a mediator to enhance the efficiency and effectiveness of public expenditure management, in line with the literature

.