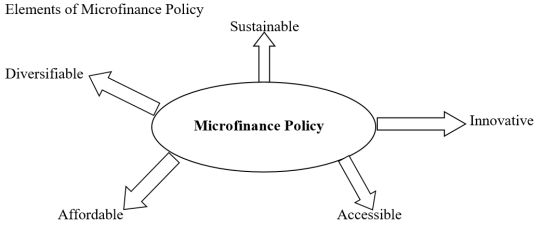

Financial policy stands as the important directives towards enhancing financial inclusion development in different levels. The higher level of financial inclusion increases the level of official savings, which in turn promotes development. This study examines the impact of resources policy on enhancing financial inclusion in Iringa Hope Joint SACCOS in Southern Highland Zone. The study used binary logistic regression model and a Cross-Sectional Survey Design. The Statistical Package for Social Science (SPSS ver. 20, IBM, USA) was used to perform analysis. The study revealed that, affordable financial services, faster financial services, secure financial services, transparent financial services and convenient financial services increases possibility of financial inclusion if microfinance policy strategies are well organized. As a policy issue, financial inclusion is said to be a major contributor to economic growth, poverty reduction, effectiveness to monetary policy transmission and financial sector stability. The findings also show that importance of leadership is recognized by policy makers, which made leadership as among of the principle for financial inclusion innovativeness. Effective financial inclusion strategies which are most important are national micro finance policy, post office savings bank loans, mobile financial services, agency banking, shared infrastructure network, insurance policy provisions. The practical implications of these study findings provided the useful information to policy makers and microfinance and financial sector management officials during planning process and decision making in the destination. The study recommends that, Policymakers should focus on developing policies considering a sustainable banking services delivery model and need-based products for rural and urban consumers.

| Published in | Journal of World Economic Research (Volume 14, Issue 1) |

| DOI | 10.11648/j.jwer.20251401.13 |

| Page(s) | 26-33 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2025. Published by Science Publishing Group |

Policy, Investment, Strategies, Microfinance

Variable name | Coefficients | Standard Error | T-Stat | P-value |

|---|---|---|---|---|

Microfinance Information | 0.880 | 0.224 | 4.352 | 0.000 |

Training on access to Saving | 0.024 | 0.086 | 1.607 | 0.109 |

Training on bank account | 0.043 | 0.014 | 0.771 | 0.532 |

Availability of banking services | 2.587 | 0.521 | 1.194 | 0.000 |

Access to financial infrastructure | 0.021 | 0.165 | 3.176 | 0.002 |

Quality of service | 0.015 | 0.105 | 2.005 | 0.046 |

Constant | 0.150 | 3.711 | 0.000 | |

F-value 7.685 |

Variable name | Coefficients | Standard Error | T-Stat | P-value |

|---|---|---|---|---|

Affordable financial services | 0.605 | 0.145 | 3.527 | 0.000 |

Faster financial services | 0.884 | 0.175 | 1.472 | 0.027 |

Secure financial services | 1.047 | 0.059 | 1.855 | 0.008 |

Transparent financial services | 0.587 | 0.169 | 2.808 | 0.009 |

Convenient financial services | 0.447 | 0.178 | 4.333 | 0.037 |

Constant | 0.315 | 2.740 | 0.000 | |

F-value 6.163 |

ATM | Automated Teller Machine |

BOT | Bank of Tanzania |

GDP | Gross Domestic Product |

IBM | International Business Machines |

ICT | Information Communication and Technology |

MFIs | Microfinance Institutions |

MoF | Ministry of Finance |

NFIF | National Financial Inclusion Framework |

SACCOS | Savings, and Credits Cooperatives Societies |

SPSS | Statistical Package for Social Science |

USA | United State of America |

| [1] | Ahmed, M. S and Wei Jianguo, W., (2014). Financial Inclusion and Challenges in Tanzania, Research Journal of Finance and Accounting, 5(21) ISSN (Paper) 2222-1697 ISSN (Online) 2222-2847. |

| [2] | Anarfo, E. B & Abor J. Y & Osei, K. A (2020) Financial regulation and financial inclusion in Sub-Saharan Africa: Does financial stability play a moderating role?, Research in International Business and Finance, Volume 51, 101070, ISSN 0275-5319, |

| [3] | Arun, T and Kamath, R., (2015). Financial inclusion: Policies and practices, IIMB Management Review, 27(4): 267-287, ISSN 0970-3896. |

| [4] | Bag, D., & Shrabanee, D., (2016). Factors Affecting Financial Inclusion: A Study in Rourkela. |

| [5] | Bourainy, M, Salah, A and Sherif, M., (2021) Assessing the Impact of Financial Inclusion on Inflation Rate in Developing Countries. Open Journal of Social Sciences, 09: 397-424. |

| [6] | Chauvet, L and Jacolin, L., (2017) Financial Inclusion, Bank Concentration, and Firm Performance, World Development, Volume 97: 1-13. |

| [7] | Cheng, H, Hu, H and Du, Y., (2024). Financial Inclusion Practice and the Status of Rural Women in Family: Based on a Field Survey in Gansu China. American Journal of Industrial and Business Management, 14: 373-391. |

| [8] | FinScope Tanzania. (2017), Insights that drive innovations. Financial Sector Deepening Trust (FSDT), Dar es Salaam, United Republic of Tanzania. |

| [9] | Gambe. B and Sandada, M., (2018) The Effectiveness of Selected Financial Inclusion Strategies: Evidence a Developing Country, AUDŒ, 14(3): 59-64. |

| [10] | Hannig, K and Jansen, C., (2010) Financial Inclusion and Financial Stability: Current Policy Issues. ADBI Working Paper 259. Tokyo: Asian Development Bank Institute. Available: |

| [11] | Hassan, I., (2019). An examination of the Impact of Financial Inclusion on Poverty Reduction: An Empirical Evidence from Sub-Saharan Africa. International Journal of Scientific and Research Publications (IJSRP). 9. p8532. |

| [12] | Hassouba, T. A., (2023). "Financial inclusion in Egypt: the road ahead", Review of Economics and Political Science, Vol. ahead-of-print No. ahead-of-print. |

| [13] | Hussain, S, Rehman, A. U, Ullah, S, Waheed, A & Hassan, S., (2024). Financial Inclusion and Economic Growth: Comparative Panel Evidence from Developed and Developing Asian Countries. Sage Open, 14(1). |

| [14] | Koomson, I, Villano, R. A & Hadley, D., (2020) Intensifying financial inclusion through the provision of financial literacy training: a gendered perspective. Applied Economics, 52(4): 375-387, |

| [15] | Mdasha, Z., Irungu, D., & Wachira, M. (2018). Effects of Financial Inclusion Strategy on Performance of Small and Medium Enterprises: A case of Selected SMEs in Dar es Salaam, Tanzania. Journal of Strategic Management, 2(1), 51-70. |

| [16] | National Microfinance Policy (NMP), (2017). Ministry of Finance and Planning, Dar Es Salaam, United Republic of Tanzania. |

| [17] | Sani, I. S, Ozdeser, H & Cavusoglu, B., (2018). Financial inclusion as a pathway to welfare enhancement and income equality: Micro-level evidence from Nigeria. Development Southern Africa, 36(3), 390–407. |

| [18] | Sarpong, B & Nketiah-Amponsah, E., (2022). Financial inclusion and inclusive growth in sub-Saharan Africa. Cogent Economics & Finance, 10(1). |

| [19] | Suprapti, I, Harsono, I, Sutanto, H, Chaidir, T and Arini, G., (2024). Financial Inclusion Strategies (Exploring the Landscape Through Systematic Literature Review). Accounting Studies and Tax Journal (COUNT). 1: 101-110. |

| [20] | Van Rooyen, C& Stewart, R& De Wet, T. (2012). The Impact of Microfinance in Sub-Saharan Africa: A Systematic Review of the Evidence. World Development. 40. 2249-2262. |

| [21] | Were, M & Odongo, M & Israel, C (2021). Gender disparities in financial inclusion in Tanzania," WIDER Working Paper Series wp-2021-97, World Institute for Development Economic Research (UNU-WIDER). |

| [22] |

World Bank, (2013). Financial Inclusion: Helping Countries Meet the Needs of the Under-Banked and Under-Served, © Washington,

http://hdl.handle.net/10986/16091 License: CC BY 3.0 IGO. |

| [23] | Tanha, M., Amin, M. R., Masum, M. Y., Bairagi, M., Rahman, M. H., & Hasan, M. Z. (2024). Cashless mobile financial services: Rapid growing financial sector in Bangladesh's financial industry. Annals of Management and Organization Research, 6(2), 107-125. |

| [24] | Godswill O. (2024). The impact of financial inclusion on poverty reduction and economic growth in Sub-Saharan Africa: A comparative study of digital financial services. Social Sciences & Humanities Open. 11. |

| [25] | Showkat M, Nagina R, Baba M. A & Yahya A. T, (2024). The impact of financial literacy on women’s economic empowerment: exploring the mediating role of digital financial services. Cogent Economics & Finance. 13. |

| [26] | Lakshmi K & Mukhopadhyay, J. P., (2013). Patterns of Financial Behavior Among Rural and Urban Clients: Some Evidence from Tamil Nadu, India. Institute for Money, Technology and Financial Inclusion (IMTFI). |

| [27] | Ariyanto D. Y, Soejono F. E & Dewi S. P. (2020). Digital Economy and Financial Inclusion. Journal of Environmental Treatment Techniques, Volume 8, Issue1, Pages: 241-243. |

| [28] | Lethiwe N, Thanda S & Bozkuş K. S. (2023). The impact of government effectiveness on trade and financial openness: The generalized quantile panel regression approach, Journal of Risk and Financial Management, ISSN 1911-8074, MDPI, Basel, Vol. 16, Iss. 1, pp. 1-20, |

| [29] | Ampenberger, M, Schmid, T, Achleitner, A. K Kaserer, C. (2009). Capital structure decisions in family firms: empirical evidence from a bank-based economy, Working Paper, No. 2009-05, Technische Universität München, Center for Entrepreneurial and Financial Studies (CEFS), München. |

| [30] | Peskes, M, Tang Z. F., (2024). Significance of Private Equity Investments, especially for SMEs - Blessing or Curse? Working Papers des IUCF, No. 7/2024, ZBW Leibniz Information Centre for Economics, Kiel, Hamburg. |

| [31] | Wafula, W. N., Rono, L., & Tuwey, J. (2024). Financial Risk Attitude, Environmental Dynamism and Financial Sustainability of Small and Medium Enterprises in Nairobi, Kenya. Journal of Finance and Accounting, 8(9), 25–39. |

| [32] | Ngatia, J., Makori, D., & Theuri, J. (2024). Camel Financial Indicators and Performance of Tier Three Commercial Banks in Kenya. Journal of Finance and Accounting, 8(9), 80–99. |

| [33] | Njoki, K. M., & Reuben, N. (2024). The Influence of Financial Restructuring on Organizational Performance at Equity Bank Kenya Limited. Journal of Finance and Accounting, 8(9), 69–79. |

| [34] | Clatworthy, M., García Lara, J. M., & Lee, E. (2024). Introduction to the 2024 Accounting and Business Research International Accounting Policy Forum. Accounting and Business Research, 54(7), 757–759. |

| [35] | Nobes, C., 2020. A half-century of Accounting and Business Research: the impact on the study of international financial reporting. Accounting and Business Research, 50 (7), 693–701. |

| [36] | Caomique P. G., Belem F., Tapsoba S. J. (2024) "Revamping African and the United States Economic Ties: A Quest for More Trade and Investment", Ferdi Note brève B277, Novembre. |

| [37] | Sorgho Z. (2024) "US suspension policy from the African Growth and Opportunity Act (AGOA): An estimation of the missing exports from sub-Saharan Africa", South African Journal of Economics (SAGE), vol. 92 (issue 4), pp. 413-580. |

| [38] | Roemer M. L., (2024). National Financial Inclusion and Education Strategy for Suriname. 2024–2027. |

| [39] | Aloulou, M., Grati, R., Al-Qudah, A. A. and Al-Okaily, M. (2024), "Does FinTech adoption increase the diffusion rate of digital financial inclusion? A study of the banking industry sector", Journal of Financial Reporting and Accounting, Vol. 22 No. 2, pp. 289-307. |

| [40] | Chinoda, T and Kapingura F. M. (2023). The Impact of Digital Financial Inclusion and Bank Competition on Bank Stability in Sub-Saharan Africa. Economies 11(1), 15; |

| [41] | Kamble, P. A., Mehta, A. & Rani, N. (2024). Financial Inclusion and Digital Financial Literacy: Do they Matter for Financial Well-being?. Soc Indic Res 171, 777–807 (2024). |

| [42] | Obiedallah, Y. R & Abdelaziz, A. H. (2024). Financial inclusion and Financial Performance: The interplay role of capital adequacy requirements in Egyptian Banks. Futur Bus J 10, 96. |

| [43] | Josyula, H. P. (2024). Impact on Financial Inclusion. In: Redefining Cross-Border Financial Flows. Apress, Berkeley, CA. |

| [44] | Song, X., Li, J. & Wu, X. (2024). Financial inclusion, education, and employment: empirical evidence from 101 countries. Humanit Soc Sci Commun 11, 172. |

| [45] | Okello C, Bongomin, G & Yourougou, P, Balinda, R & Lubega, J. (2024). Customized financial literacy: a boon for universal financial inclusion of PWDs post COVID-19 pandemic in developing countries. Journal of Financial Regulation and Compliance. 32. |

| [46] | Koomson, I, Asongu, S & Acheampong A. (2022). Financial inclusion and food insecurity: Examining linkages and potential pathways. Journal of Consumer Affairs. 57. |

| [47] | Wong, Z. Z. A., Badeeb, R. A. & Philip, A. P. (2023). Financial Inclusion, Poverty, and Income Inequality in ASEAN Countries: Does Financial Innovation Matter? Soc Indic Res 169, 471–503. |

| [48] | Zhang, S & Posso, A. (2019). Thinking Inside the Box: A Closer Look at Financial Inclusion and Household Income. Journal of Development Studies. 55. 1616-1631. |

| [49] | Development Bank (2013) Financial Inclusion in Africa, (Triki, T & Faye, I -editors) Tunis Belvédère TunisiaAghion, P., and P. Howitt (1992). ‘A Model of Growth Through Creative Destruction’. Econometrical, 60(2): 323–51. |

APA Style

Ugulumu, E. S., Nyankweli, E., Lyanga, T. (2025). Impact of Resources Policy for Enhancing Financial Inclusion in Iringa Hope Joint SACCOS in Southern Highland Zone. Journal of World Economic Research, 14(1), 26-33. https://doi.org/10.11648/j.jwer.20251401.13

ACS Style

Ugulumu, E. S.; Nyankweli, E.; Lyanga, T. Impact of Resources Policy for Enhancing Financial Inclusion in Iringa Hope Joint SACCOS in Southern Highland Zone. J. World Econ. Res. 2025, 14(1), 26-33. doi: 10.11648/j.jwer.20251401.13

AMA Style

Ugulumu ES, Nyankweli E, Lyanga T. Impact of Resources Policy for Enhancing Financial Inclusion in Iringa Hope Joint SACCOS in Southern Highland Zone. J World Econ Res. 2025;14(1):26-33. doi: 10.11648/j.jwer.20251401.13

@article{10.11648/j.jwer.20251401.13,

author = {Enock Stanley Ugulumu and Emmanuel Nyankweli and Timothy Lyanga},

title = {Impact of Resources Policy for Enhancing Financial Inclusion in Iringa Hope Joint SACCOS in Southern Highland Zone

},

journal = {Journal of World Economic Research},

volume = {14},

number = {1},

pages = {26-33},

doi = {10.11648/j.jwer.20251401.13},

url = {https://doi.org/10.11648/j.jwer.20251401.13},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.jwer.20251401.13},

abstract = {Financial policy stands as the important directives towards enhancing financial inclusion development in different levels. The higher level of financial inclusion increases the level of official savings, which in turn promotes development. This study examines the impact of resources policy on enhancing financial inclusion in Iringa Hope Joint SACCOS in Southern Highland Zone. The study used binary logistic regression model and a Cross-Sectional Survey Design. The Statistical Package for Social Science (SPSS ver. 20, IBM, USA) was used to perform analysis. The study revealed that, affordable financial services, faster financial services, secure financial services, transparent financial services and convenient financial services increases possibility of financial inclusion if microfinance policy strategies are well organized. As a policy issue, financial inclusion is said to be a major contributor to economic growth, poverty reduction, effectiveness to monetary policy transmission and financial sector stability. The findings also show that importance of leadership is recognized by policy makers, which made leadership as among of the principle for financial inclusion innovativeness. Effective financial inclusion strategies which are most important are national micro finance policy, post office savings bank loans, mobile financial services, agency banking, shared infrastructure network, insurance policy provisions. The practical implications of these study findings provided the useful information to policy makers and microfinance and financial sector management officials during planning process and decision making in the destination. The study recommends that, Policymakers should focus on developing policies considering a sustainable banking services delivery model and need-based products for rural and urban consumers.

},

year = {2025}

}

TY - JOUR T1 - Impact of Resources Policy for Enhancing Financial Inclusion in Iringa Hope Joint SACCOS in Southern Highland Zone AU - Enock Stanley Ugulumu AU - Emmanuel Nyankweli AU - Timothy Lyanga Y1 - 2025/02/17 PY - 2025 N1 - https://doi.org/10.11648/j.jwer.20251401.13 DO - 10.11648/j.jwer.20251401.13 T2 - Journal of World Economic Research JF - Journal of World Economic Research JO - Journal of World Economic Research SP - 26 EP - 33 PB - Science Publishing Group SN - 2328-7748 UR - https://doi.org/10.11648/j.jwer.20251401.13 AB - Financial policy stands as the important directives towards enhancing financial inclusion development in different levels. The higher level of financial inclusion increases the level of official savings, which in turn promotes development. This study examines the impact of resources policy on enhancing financial inclusion in Iringa Hope Joint SACCOS in Southern Highland Zone. The study used binary logistic regression model and a Cross-Sectional Survey Design. The Statistical Package for Social Science (SPSS ver. 20, IBM, USA) was used to perform analysis. The study revealed that, affordable financial services, faster financial services, secure financial services, transparent financial services and convenient financial services increases possibility of financial inclusion if microfinance policy strategies are well organized. As a policy issue, financial inclusion is said to be a major contributor to economic growth, poverty reduction, effectiveness to monetary policy transmission and financial sector stability. The findings also show that importance of leadership is recognized by policy makers, which made leadership as among of the principle for financial inclusion innovativeness. Effective financial inclusion strategies which are most important are national micro finance policy, post office savings bank loans, mobile financial services, agency banking, shared infrastructure network, insurance policy provisions. The practical implications of these study findings provided the useful information to policy makers and microfinance and financial sector management officials during planning process and decision making in the destination. The study recommends that, Policymakers should focus on developing policies considering a sustainable banking services delivery model and need-based products for rural and urban consumers. VL - 14 IS - 1 ER -

Department of Community Economic Development, Open University of Tanzania, Dar Es Salaam, Tanzania

Information