The overall objective of this study was to examine the impacts of savings and credit practices and how they affect borrower's investment decisions in affordable, faster, secure, transparent, and convenient financial services manner in Iringa hope joint SACCOS in Southern Highland zone of Iringa, Kilolo, Mufindi District in Iringa region and Wanging’ombe District in Njombe Region. Using surveyed data of a sample of 370 individual members from the study area, the study employed multiple regression model and descriptive statistics. The study findings revealed that most of the SACCOs members were eager to join financial services as an opportunity for the present and future investment and continue with services to benefit from financial products at an increasing rate due to strongly affordable, faster, secure, transparent, and convenient financial services. It also revealed that financial inclusion had a direct and significant impact on economic development of marginalized people. Furthermore, IHJS members were in favor of utilizing mobile money technology in possibility of enhancing more being included in financial sector in order to accelerate investment opportunities, hence financial inclusion is affected positively. Women are engaged in financial sector hence being considered as an important in financial inclusions issues since women are engaged more in investment activities. Finally, the findings revealed that women have of being included in financial sector and use the fund to invest in different economic activities compared to men who are reluctant to run towards the opportunity.

| Published in | International Journal of Finance and Banking Research (Volume 11, Issue 1) |

| DOI | 10.11648/j.ijfbr.20251101.11 |

| Page(s) | 1-11 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2025. Published by Science Publishing Group |

Credit, Financial Products, Investment, Microfinance, Opportunity, Saving

Model | Unstandardized Coefficients | Standardized Coefficients | T | Sig. | |

|---|---|---|---|---|---|

B | Std. Error | Beta | |||

(Constant) | .400 | .096 | 4.152 | .000 | |

Financial services improved living standards | .015 | .012 | .046 | 3.295 | .001 |

Loans facilitate income growth | .020 | .020 | .035 | 1.017 | .031 |

Savings in financial services is beneficial | .024 | .010 | .087 | 2.422 | .016 |

Credits provide funds for investment | .026 | .019 | .051 | 1.400 | .002 |

Loans are available to both gender | .671 | .031 | .769 | 21.990 | .000 |

Mobile technology provides reliable access to Markets | Total | |||

|---|---|---|---|---|

Using the technology | Not using the technology | |||

Sex | Male | 84(31.1%) | 0(00.0%) | 84(22.7% |

Female | 186(68.9%) | 100(100.0%) | 286(77.3%) | |

Total | 270(100.0%) | 100(100.0%) | 370(100.0%) | |

Value | Asymp. Sig. (2-sided) | Exact Sig. (2-sided) | Exact Sig. (1-sided) | |

|---|---|---|---|---|

Pearson Chi-Square | 40.249a | .000 | ||

Continuity Correction | 38.495 | .000 | ||

Likelihood Ratio | 61.595 | .000 | ||

Fisher's Exact Test | .000 | .000 | ||

Linear-by-Linear Association | 40.140 | .000 |

Experience and awareness about SACCOS | Total | |||||

|---|---|---|---|---|---|---|

1-5 Years | 6-10 Years | 11-15 Years | 16=< years | |||

Sex | Male | 3(7.5%) | 30(25.6%) | 15(17.6%) | 36(28.1%) | 84(22.7%) |

Female | 37(92.5%) | 87(74.4%) | 70(82.4%) | 92(71.9%) | 286(77.3%) | |

Total | 40(100.0%) | 117(100.0%) | 85(100.0%) | 128(100.0%) | 370(100.0%) | |

Value | Asymp. Sig. (2-sided) | |

|---|---|---|

Pearson Chi-Square | 9.226 | .026 |

Likelihood Ratio | 10.551 | .014 |

Linear-by-Linear Association | 3.556 | .059 |

Sources of capital | Total | ||||

|---|---|---|---|---|---|

Farming, Livestock, Business | Farming, Livestock | Farming, Business | |||

Sex | Male | 13(22.0%) | 28(29.2%) | 43(20.0%) | 84(22.7%) |

Female | 46(78.0%) | 68(70.8%) | 172(80.0%) | 286(77.3%) | |

Total | 59(100.0%) | 96(100.0%) | 215(100.0%) | 370(100.0%) | |

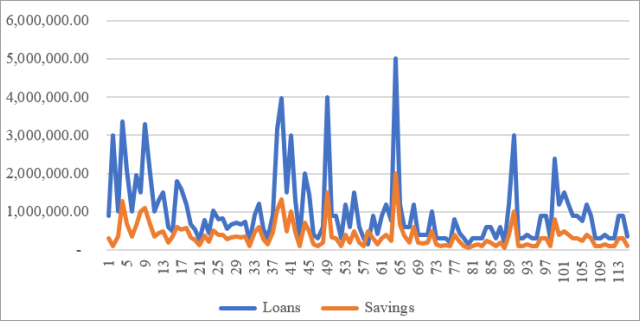

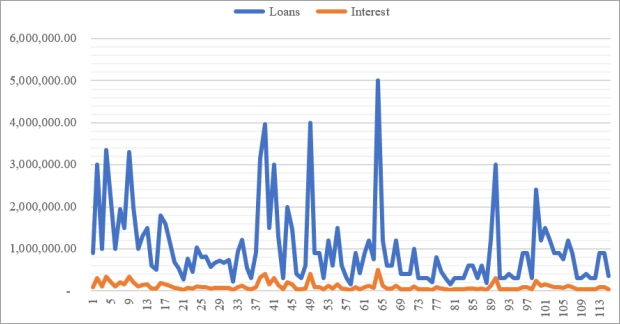

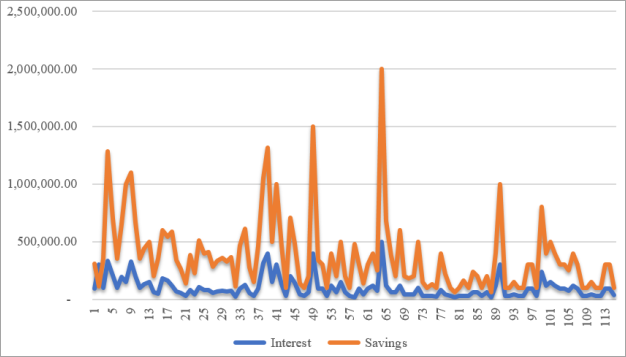

Loans | Savings | Shares | |

|---|---|---|---|

Maximum | 5,000,000.00 | 2,000,000.00 | 70,000.00 |

Minimum | 144,000.00 | 60,000.00 | 50,000.00 |

Mean | 994,594.78 | 374,013.04 | 50,347.83 |

IHJS | Iringa Hope Joint Saccos |

SACCOS | Savings, and Credits Cooperatives Societies |

GDP | Goss Domestic Product |

FI | Financial Inclusion |

ATM | Automated Teller Machine |

SMEs | Small and Medium Enterprises |

| [1] | Adera, A & Abdisa, L. T. (2023). Financial inclusion and women’s economic empowerment: Evidence from Ethiopia," Cogent Economics & Finance, Taylor & Francis Journals, vol. 11(2), pages 2244864-224, |

| [2] | Alicia G. A. (2021) Financial Inclusion Measurement in the Least Developed Countries in Asia and Africa, Journal of the Knowledge Economy |

| [3] | Amoah, A., Korle, K & Asiama, R. (2020). Mobile money as a financial inclusion instrument: what are the determinants? International Journal of Social Economics ahead-of-print. |

| [4] | Balliester, R. T, (2021), “What is financial inclusion? A critical review”, SOAS Department of Economics Working Paper No. 246, London: SOAS University of London. |

| [5] | Bourainy, M, Salah, A and Sherif, M. (2021) Assessing the Impact of Financial Inclusion on Inflation Rate in Developing Countries. Open Journal of Social Sciences, 9, 397-424. |

| [6] | Cnaan, R. A., Moodithaya, M. S & Handy, F. (2012). Financial inclusion: Lessons from rural South India. Journal of Social Policy, 41(1), 183-205. |

| [7] | Cooperative Development Policy, 2002, Printed by the Government Printer Dar Es Salaam-Tanzania. |

| [8] | Demirguc-Kunt, A, Klapper. L, Singer, D., and Ansar, S.. (2022). The Global Findex Database 2021: Financial Inclusion, Digital Payments, and Resilience in the Age of COVID-19. Washington, DC: World Bank. |

| [9] | Eton, M, Mwosi, F, Ejang, M & Poro, S. G. (2021). Financial inclusion: Is it a precursor to agricultural commercialization amongst smallholder farmers in Uganda? A comparative analysis between Lango and Buganda sub-regions. Journal of Economics and International Finance, 13(1): 1-12. |

| [10] | Falaiye, T, Elufioye, O, Awonuga, P, Ibeh, C, Olatoye, F & Mhlongo, N. (2024). financial inclusion through technology: a review of trends in emerging markets. International Journal of Management & Entrepreneurship Research. 6. 368-379. |

| [11] | Falaiye, T, Odeyemi, O, Ajayi-Nifise, A, Daraojimba, R and Mhlongo, N. (2024). A review of microfinancing's role in entrepreneurial growth in African Nations. International Journal of Science and Research Archive. 11. 1376-1387. |

| [12] | Fowowe, B. (2020). The effects of financial inclusion on agricultural productivity in Nigeria. Journal of Economics and Development, 22(1), pp. 61-79. |

| [13] | Hannig, A & Jansen, S., (2010). Financial Inclusion and Financial Stability: Current Policy Issues. SSRN Electronic Journal. |

| [14] | Ifediora, C, Offor, K. O, Eze, E. F, Takon, S. M, Ageme, A. E, Ibe, G. I and Onwumere, J. U. J. (2022). Financial inclusion and its impact on economic growth: Empirical evidence from sub-Saharan Africa. Cogent Economics & Finance (2022), 10: 2133356 |

| [15] | IMF, (2020) International Monetary Fund working Paper, WP/20/157. |

| [16] | Karerwa, C. (2023). Effect of Financial Inclusion on Agricultural Farm Performance in Rwanda: A case study of COMSS cooperative. International Journal of Research and Innovation in Social Science (IJRISS), 7(12): 641-688. |

| [17] | Kling, G, Pesqué-Cela, V, Tian, L and Luo, D. (2020). A theory of financial inclusion and income inequality, The European Journal of Finance, |

| [18] | Lal, T. (2021). Impact of financial inclusion on economic development of marginalized communities through the mediation of social and economic empowerment. International Journal of Social Economics, 48(12), 1768–1793. |

| [19] | Macha, J. J, Chong, Y & Chen, I. (Spring 2018). "Rural Household's Intention to Use Microfinance in Tanzania". International Journal of Business. 23(2): 199–216. |

| [20] | Martínez, C. H, Hidalgo, X. P and Tuesta, D, (2013) Demand factors that influence financial inclusion in Mexico: analysis of the barriers based on the ENIF survey, 13/37 Working Paper Mexico City. |

| [21] | Mhlanga, D& Dunga, S. (2020). Measuring Financial Inclusion and its Determinants Among the Smallholder Farmers in Zimbabwe: An Empirical Study. Eurasian Journal of Business and Management. 8. 266-281. |

| [22] | Naftaly, M & Thomi, J. (2021). The Determinants of Financial Inclusion. e-Finanse. 17. 50-57. |

| [23] | National Financial Inclusion Council (NFIC), (2023) Evaluation Report on the Implementation of NFIF2 (2018-2023), Dar Es Salaam, Tanzania. |

| [24] | National Microfinance Policy (NMP), (2017). Ministry of Finance and Planning, Dar Es Salaam, United Republic of Tanzania. |

| [25] | Ndanshau, M. O and Njau, F. E. (2021) Empirical Investigation into Demand-Side Determinants of Financial Inclusion in Tanzania. African Journal of Economic Review, 9(1). |

| [26] | Njanike, K & Mpofu, R. T. (2024). Factors Influencing Financial Inclusion for Social Inclusion in Selected African Countries. Insight on Africa, 16(1), 93-112. |

| [27] | Ogbemudia B. I, Wilson, E, Ugwu, C. N & Benjamin I. C. (2024). Investing in Rural Agriculture in the Face of Innovative Financial Services: Does Financial Literacy Matter in Nigeria? Sage Open, 14(2). |

| [28] | Omar, M. A & Inaba, K. (2020). "Does financial inclusion reduce poverty and income inequality in developing countries? A panel data analysis," Journal of Economic Structures, Springer;Pan-Pacific Association of Input-Output Studies (PAPAIOS), vol. 9(1), pages 1-25, |

| [29] | Prahalad, C. K. (2007) The Fortune at the Bottom of the Pyramid: Eradicating Poverty through profits, Pearson Education, Inc. N. J USA. |

| [30] | Pranajaya, E, Alexandri, M. B, Chan, A and Hermanto, B, (2024). Examining the influence of financial inclusion on investment decision: A bibliometric review, Heliyon, 10(3) ISSN 2405-8440. |

| [31] | Raichoudhury, A. (2020). Major Determinants of Financial Inclusion: State-Level Evidences from India, Vision-The Journal of Business Perspective, 24(2): 151-159. |

| [32] | Sharma, U and Changkakati, B. (2022) Dimensions of global financial inclusion and their impact on the achievement of the United Nations Development Goals, Borsa Istanbul Review, Volume 22, Issue 6, Pages 1238-1250, ISSN 2214-8450, |

| [33] | Consultative Group to Assist the Poor (CGAP) annual report (2015) (English). Umbrella Trust Fund Annual Report Washington, D. C.: World Bank Group. |

| [34] | The Global Partnership for Financial Inclusion (GPFI), (2016), China-2016-Priorities-Paper, |

| [35] |

Turvey, C. G, (2017), Inclusive finance and inclusive rural transformation, 10 IFAD research series. World Bank Global Payments Systems Survey:

https://www.worldbank.org/en/topic/financialinclusion/brief/gpss |

| [36] | Were, M & Odongo, M & Israel, C. (2021). Gender disparities in financial inclusion in Tanzania," WIDER Working Paper Series wp-2021-97, World Institute for Development Economic Research (UNU-WIDER). |

| [37] | Yorulmaz, R., (2012) "Financial Inclusion & Economic Development: A Case Study of Turkey and a Cross-country Analysis of European Union". All Theses. 1352. |

APA Style

Ugulumu, E. S., Nyankweli, E., Lyanga, T. (2025). Impact of Investment in Financial Services on Financial Inclusion in Iringa Hope Joint SACCOS in Southern Highland Zone of Tanzania. International Journal of Finance and Banking Research, 11(1), 1-11. https://doi.org/10.11648/j.ijfbr.20251101.11

ACS Style

Ugulumu, E. S.; Nyankweli, E.; Lyanga, T. Impact of Investment in Financial Services on Financial Inclusion in Iringa Hope Joint SACCOS in Southern Highland Zone of Tanzania. Int. J. Finance Bank. Res. 2025, 11(1), 1-11. doi: 10.11648/j.ijfbr.20251101.11

@article{10.11648/j.ijfbr.20251101.11,

author = {Enock Stanley Ugulumu and Emmanuel Nyankweli and Timothy Lyanga},

title = {Impact of Investment in Financial Services on Financial Inclusion in Iringa Hope Joint SACCOS in Southern Highland Zone of Tanzania

},

journal = {International Journal of Finance and Banking Research},

volume = {11},

number = {1},

pages = {1-11},

doi = {10.11648/j.ijfbr.20251101.11},

url = {https://doi.org/10.11648/j.ijfbr.20251101.11},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ijfbr.20251101.11},

abstract = {The overall objective of this study was to examine the impacts of savings and credit practices and how they affect borrower's investment decisions in affordable, faster, secure, transparent, and convenient financial services manner in Iringa hope joint SACCOS in Southern Highland zone of Iringa, Kilolo, Mufindi District in Iringa region and Wanging’ombe District in Njombe Region. Using surveyed data of a sample of 370 individual members from the study area, the study employed multiple regression model and descriptive statistics. The study findings revealed that most of the SACCOs members were eager to join financial services as an opportunity for the present and future investment and continue with services to benefit from financial products at an increasing rate due to strongly affordable, faster, secure, transparent, and convenient financial services. It also revealed that financial inclusion had a direct and significant impact on economic development of marginalized people. Furthermore, IHJS members were in favor of utilizing mobile money technology in possibility of enhancing more being included in financial sector in order to accelerate investment opportunities, hence financial inclusion is affected positively. Women are engaged in financial sector hence being considered as an important in financial inclusions issues since women are engaged more in investment activities. Finally, the findings revealed that women have of being included in financial sector and use the fund to invest in different economic activities compared to men who are reluctant to run towards the opportunity.

},

year = {2025}

}

TY - JOUR T1 - Impact of Investment in Financial Services on Financial Inclusion in Iringa Hope Joint SACCOS in Southern Highland Zone of Tanzania AU - Enock Stanley Ugulumu AU - Emmanuel Nyankweli AU - Timothy Lyanga Y1 - 2025/02/17 PY - 2025 N1 - https://doi.org/10.11648/j.ijfbr.20251101.11 DO - 10.11648/j.ijfbr.20251101.11 T2 - International Journal of Finance and Banking Research JF - International Journal of Finance and Banking Research JO - International Journal of Finance and Banking Research SP - 1 EP - 11 PB - Science Publishing Group SN - 2472-2278 UR - https://doi.org/10.11648/j.ijfbr.20251101.11 AB - The overall objective of this study was to examine the impacts of savings and credit practices and how they affect borrower's investment decisions in affordable, faster, secure, transparent, and convenient financial services manner in Iringa hope joint SACCOS in Southern Highland zone of Iringa, Kilolo, Mufindi District in Iringa region and Wanging’ombe District in Njombe Region. Using surveyed data of a sample of 370 individual members from the study area, the study employed multiple regression model and descriptive statistics. The study findings revealed that most of the SACCOs members were eager to join financial services as an opportunity for the present and future investment and continue with services to benefit from financial products at an increasing rate due to strongly affordable, faster, secure, transparent, and convenient financial services. It also revealed that financial inclusion had a direct and significant impact on economic development of marginalized people. Furthermore, IHJS members were in favor of utilizing mobile money technology in possibility of enhancing more being included in financial sector in order to accelerate investment opportunities, hence financial inclusion is affected positively. Women are engaged in financial sector hence being considered as an important in financial inclusions issues since women are engaged more in investment activities. Finally, the findings revealed that women have of being included in financial sector and use the fund to invest in different economic activities compared to men who are reluctant to run towards the opportunity. VL - 11 IS - 1 ER -

Department of Community Economic Development, Open University of Tanzania, Dar Es Salaam, Tanzania

Department of Community Economic Development, Open University of Tanzania, Dar Es Salaam, Tanzania

Department of Community Economic Development, Open University of Tanzania, Dar Es Salaam, Tanzania

Information