Abstract

Fraud in financial statements can have an impact on the accuracy and reliability of the use of financial statements, including affecting the amount of tax, fines paid, and the audit process. This study aims to analyze the effect of pressure, arrogance and collusion on financial statement fraud and the role of income tax rates as a moderating variable in non-financial companies listed on the Indonesia Stock Exchange in 2020-2022. The data in this study consisted of 207 research observations determined using purposive sampling method. Data collection was conducted through document analysis, using annual financial reports and annual reports. The analytical technique employed was regression analysis, moderated by Eviews. The study commenced with a descriptive statistical analysis, followed by an examination of the classical assumptions, including multicollinearity and heteroskedasticity. Finally, an analysis of moderated regression was conducted. The results of the regression analysis indicated that pressure, arrogance, and collusion were found to influence financial statement fraud. The moderated regression analysis demonstrated that the income tax rate was capable of moderating the influence of pressure, arrogance, and collusion on financial statement fraud. The theoretical implications of this study offer a novel perspective on the moderating effect of income tax rates on the relationship between pressure, arrogance and collusion and financial statement fraud. This study is of practical value and provides information that can inform decision-making for stakeholders.

Keywords

Pressure, Arrogance, Collusion, Fraudulent Financial Statements, Income Tax Rate

1. Introduction

Financial reports are currently one of the company's communication tools for financial data or activities carried out by companies aimed at users of financial information, whether from top managers to subordinates or parties outside the company, which are used to inform all activities carried out. in a certain period. As stated by Purba

| [22] | Purba, B. P. (2015). Fraud dan Korupsi Pencegahan, Pendeteksian, dan Pemberantasannya (Cetakan Pe). Lestari Kiranatama. |

[22]

, increasingly tight business competition often encourages management or certain parties in companies or organizations to deliberately manipulate financial reports or not fully disclose important information that should be reported, which results in actions cheating.

Priantara

| [21] | Priantara, D. (2020). Fraud Auditing & Investigation. |

[21]

states that fraud is an act of intentionally deceiving or deceiving to take or lose someone else's money, property, or legitimate rights. Fraud that can have a long-term impact on a company is fraudulent financial statements. According to Arens et al in Rahmatika

| [23] | Rahmatika, D. N. (2020). Fraud Auditing Kajian Teoritis dan Empiris (Penerbit: Deepublish). |

[23]

, stating that fraudulent financial statements are errors in presentation or omission of amounts done intentionally which can deceive report users. There are many reasons why management commits this act of fraud, including the conflict of interest that occurs between agents and investors who are considered principals. This is what can cause fraudulent financial statements to occur Dinata

| [10] | I Made Nova Dinata, Ni Nyoman Ayu Suryandari, I.. B. M. (n.d.). Analisis Fraud Diamond Dalam Mendeteksi Financial Statement Fraud. E-Journal Unmas, Vol 1 No 1. |

[10]

.

Based on a survey by the Association of Certified Fraud Examiners Global (ACFE) regarding the fraud category, it shows that fraud cases in the form of misuse of assets have the highest frequency of cases, namely 86%, followed by corruption at 50%, and the smallest frequency of cases is fraudulent financial statement. by 9%. Even though fraudulent financial statement has the lowest frequency of cases, the average impact of total losses is ranked highest at $593,000, followed by corruption at $150,000, and asset misuse at $100,000 ACFE Global

| [1] | Association of Certified Fraud Examiners (ACFE). (2022). Occupational Fraud 2022: A Report to the nations. Association of Certified Fraud Examiners, 1–96. |

[1]

.

Several reasons cause management to be motivated to act in the form of financial reports, one of which is caused by different goals from investors' goals, where investors want to improve company performance so company management will try to make this happen so that investors continue to invest in the company even though they act. Circumstances (Meidijati & Amin

| [16] | Meidijati, & Amin, M. N. (2022). Detecting Fraudulent Financial Reporting Through Hexagon Fraud Model: Moderating Role of Income Tax Rate. International Journal of Social and Management Studies (IJOSMAS), 3(2), 311–322. http://www.ijosmas.org |

[16]

. In the case of situations that occur within companies, this is usually caused by pressure, arogance and collusion. According to Betri

| [2] | Betri Sirajuddin. (2020). Akuntansi Forensik dan Audit Investiasi (Edisi dua). |

[2]

, pressure is an incentive or pressure or need that can encourage someone to commit fraud due to lifestyle demands, helplessness in financial matters, and dissatisfaction with work. Several previous studies regarding pressure as a proxy for financial targets were carried out by Ozcelik, Demetriades & Owusu-agyei, Ratmono, Octaviani & Sagala, Wicaksono & Suryandari, Yarana, Yusrianti et al which stated that pressure has an effect on fraudulent financial statements

| [6] | Demetriades, P., & Owusu-agyei, S. (2022). Fraudulent fi nancial reporting : an application of fraud diamond to Toshiba’s accounting scandal. 29(2), 729–763. https://doi.org/10.1108/JFC-05-2021-0108 |

| [18] | Octaviani, K., & Sagala, E. (2021). The Influence Of Fraud Hexagon Elements On Fraudulent Financial Reporting At The Banking Companies Listed On The Indonesian Stock Exchange Periode 2018-2020. 18(6), 2273–2282. |

| [20] | Ozcelik, H. (2020). An Analysis of Fraudulent Financial Reporting Using the Fraud Diamond Theory Perspective: An Empirical Study on the Manufacturing Sector Companies Listed on the Borsa Istanbul. In S. Grima, E. Boztepe, & P. J. Baldacchino (Eds.), Contemporary Issues in Audit Management and Forensic Accounting (Vol. 102, pp. 131–153). Emerald Publishing Limited. https://doi.org/10.1108/S1569-375920200000102012 |

| [24] | Ratmono, D., Darsono, D., & Cahyonowati, N. (2020). Financial Statement Fraud Detection With Beneish M-Score and Dechow F-Score Model: An Empirical Analysis of Fraud Pentagon Theory in Indonesia. International Journal of Financial Research, 11(6), 154. https://doi.org/10.5430/ijfr.v11n6p154 |

| [30] | Wicaksono, A., & Suryandari, D. (2021). Accounting Analysis Journal The Analysis of Fraudulent Financial Reports Through Fraud Hexagon on Public Mining Companies. Accounting Analysis Journal, 10(3), 220–228. https://doi.org/10.15294/aaj.v10i3.54999 |

| [31] | Yarana, C. (2023). Factors Influencing Financial Statement Fraud: An Analysis of the Fraud Diamond Theory from Evidence of Thai Listed Companies. WSEAS Transactions on Business and Economics, 20, 1659–1672. https://doi.org/10.37394/23207.2023.20.147 |

| [34] | Yusrianti, H., Ghozali, I., Yuyetta, E., Aryanto, & Meirawati, E. (2020). Financial statement fraud risk factors of fraud triangle: Evidence from Indonesia. International Journal of Financial Research, 11(4), 36–51. https://doi.org/10.5430/ijfr.v11n4p36 |

[6, 18, 20, 24, 30, 31, 34]

.

Arrogance is a trait that demonstrates superiority and lack of awareness caused by greed and the idea that internal control within the company does not apply personally to them Crowe

| [5] | Crowe, H. (2011). Putting The Freud in Fraud: Why The Fraud Is No Longer Enough. IN Howarth, Crowe. |

[5]

. Research on arrogance as proxied by the number of CEO photos conducted by Khamainy, Octaviani & Sagala, Uciati, Utami, & Mukhibad stated that arrogance has an influence on fraudulent financial statement

| [13] | Khamainy, A. H., Ali, M., & Setiawan, M. A. (2022). Detecting fi nancial statement fraud through new fraud diamond model: the case of Indonesia. 29(3), 925–941. https://doi.org/10.1108/JFC-06-2021-0118 |

| [18] | Octaviani, K., & Sagala, E. (2021). The Influence Of Fraud Hexagon Elements On Fraudulent Financial Reporting At The Banking Companies Listed On The Indonesian Stock Exchange Periode 2018-2020. 18(6), 2273–2282. |

| [27] | Uciati, N., & Mukhibad, H. (2019). Fraudulent Financial Statements at Sharia Banks. 8(3), 198–206. https://doi.org/10.15294/aaj.v8i3.33625 |

| [28] | Utami, E. R. (2019). The Analysis of Fraud Pentagon Theory and Financial Distress for Detecting Fraudulent Financial Reporting in Banking Sector in Indonesia ( Empirical Study of Listed Banking Companies on Indonesia Stock Exchange in 2012-2017 ). 102(Icaf), 60–65. |

[13, 18, 27, 28]

. According to Vousinas

, collusion is an agreement between two or more parties that deceives another party. research on collusion carried out by Jannah & Rasuli and Octaviani & Sagala stated that collusion had an effect on fraudulent financial statements

| [11] | Jannah, V. M., & Rasuli, M. (2021). Pendekatan Vousinas Fraud Hexagon Model dalam Mendeteksi Kecurangan Pelaporan Keuangan. 4(1), 1–16. |

| [18] | Octaviani, K., & Sagala, E. (2021). The Influence Of Fraud Hexagon Elements On Fraudulent Financial Reporting At The Banking Companies Listed On The Indonesian Stock Exchange Periode 2018-2020. 18(6), 2273–2282. |

[11, 18]

.

Based on the results of a survey of fraud cases that have occurred, the phenomenon of fraud cases, especially in financial reports, is no longer foreign to the public. Therefore, this research is very important, it tests the income tax rate as a moderating variable and as a factor that could influence arrogance, collusion, and pressure on fraud. The implementation of low tax rates does not burden taxpayers too much to fulfill their obligations. However, if taxes are too high, people will try to find ways to avoid taxes that are too high Slemrod

. Based on the opinion above, this research will use the income tax rate as a moderating variable with the aim of strengthening the influence of independent variables such as pressure, arrogance, and collusion on fraudulent financial statements. In addition, this research aims to analyze the influence of pressure, arrogance and collusion on fraudulent financial reports moderated by the income tax rate.

2. Literature Review

Agency theory according Jensen & Meckling

| [4] | Company, P., Jensen, C., & Meckling, H. (1976). THEORY OF THE FIRM: MANAGERIAL BEHAVIOR, AGENCY COSTS AND OWNERSHIP STRUCTURE I. Introduction and summary In this paper WC draw on recent progress in the theory of (1) property rights, firm. In addition to tying together elements of the theory of e. 3, 305–360. |

[4]

, stated that agency interactions exist because there is a contract between the principal (owner) and the agent which uses some authority regarding decision making on the agent. Agency theory also shows that a company can be seen as a contractual relationship (loosely defined) between shareholders or shareholders and the company's operational parties. An agency relationship arises when one or more individuals, called principals, employ one or more other individuals, called agents, to carry out all company operational activities on behalf of the principals in their decision-making capacity. A conflict of interest between the agent and the principal can give rise to a person's ability to commit fraud Nanda et al

| [17] | Nanda, A., Kemas M. Husni Thamrin, & Fida Muthia. (2024). Pengaruh Intellectual Capital terhadap Kinerja Perbankan Umum Konvensional di Indonesia. Al-Kharaj: Jurnal Ekonomi, Keuangan & Bisnis Syariah, 6(4), 4192–4216. https://doi.org/10.47467/alkharaj.v6i4.926 |

[17].

Contingency theory argues that the design and control system depend on the organizational context in which the control is implemented Fiedler

| [8] | Fiedler. (1967). A Theory of Leadership Effectiveness. Advance in Experimental Social Psychology. Academic Press. |

[8]

. Meanwhile, Otley

| [19] | Otley., D., T. (1980). The Contingency Theory of Management Accounting: Achievement and Prognosis. In Readings in Accounting for Management Control, 83-1–6. |

[19]

stated that the contingency theory approach emerged from the existence of a basic assumption of universal increase. The accounting system is based on the premise that there is no universally appropriate accounting system that can be applied to all organizations in every situation. Based on the contingency theory used in this research, contingency theory is a perspective for understanding the relationship between research variables which recognizes that this relationship is not something universal or fixed, but rather depends on certain situational factors. This means that the effect of one variable on another variable may vary depending on the context or situation in which the research is conducted yuliani, et al

| [32] | Yuliani, umar hamdan, luk luk fuadah, thamrin K. H. (2021). Investment Opportunity Set, Dan Financing Mix: Penerbit Citrabooks. |

[32]

.

3. Research Hypothesis

3.1. The Effect of Pressure on Fraudulent Financial Statement

Pressure in this research is proxied by financial targets. In agency theory, financial targets set by the company that are too high can cause a conflict of interest between the principal and agent because the principal feels pressured to achieve the specified targets and can ultimately encourage fraudulent financial reporting Demetriades & Owusu-agyei

| [6] | Demetriades, P., & Owusu-agyei, S. (2022). Fraudulent fi nancial reporting : an application of fraud diamond to Toshiba’s accounting scandal. 29(2), 729–763. https://doi.org/10.1108/JFC-05-2021-0108 |

[6]

. When a manager is deemed unable to achieve financial targets, the manager will feel pressured and he will look for any shortcuts to achieve them and it is also possible to manipulate financial reports to cover up deficiencies in achieving the targets that have been set Skousen & Wright

| [3] | Christopher J. Skousen, K. R. S., & Wright, J. (2009). Detecting and predicting financial statement fraud: The effectiveness of the fraud triangle and SAS No. 99. Corporate Governance and Firm Performance. https://doi.org/10.1108/S1569-3732(2009)0000013005 |

[3]

. The size of the target determined by the company to be achieved creates pressure in achieving it and this is what causes the possibility of pressure that influences the conditions in the financial statements. Apart from that, the pressure that can lead to fraudulent actions can be in the form of financial or non-financial pressure Yusrianti et al

| [33] | Yusrianti, H., Ghozali, I., & N. Yuyetta, E. (2020). Asset Misappropriation Tendency: Rationalization, Financial Pressure, and the Role of Opportunity (Study in Indonesian Government Sector). Humanities & Social Sciences Reviews, 8(1), 373–382. https://doi.org/10.18510/hssr.2020.8148 |

[33]

.

Based on the description explained, the hypothesis in this research is:

H3: Pressure effects on fraudulent financial statements.

3.2. The Effect of Arrogance on Fraudulent Financial Statement

Arrogance can be a factor that triggers the possibility of conditions occurring in reports, especially photos and information related to the CEO's track record that are displayed annually in reports can present the level of arrogance and superiority that the CEO has Saputri & Sari

| [25] | Saputri, S. B., & Sari, S. P. (2023). Fraudulent financial reporting using the testing of the hexagon fraud theory in manufacturing on the Indonesian Sharia Stock Index (ISSI). International Journal of Latest Research in Humanities and Social Science (IJLRHSS), 06(05), 297–306. |

[25]

. Someone tends to show everyone the status and position they have in the company, this is because they do not want to lose the status or position, they have occupied Wicaksono & Suryandari

| [30] | Wicaksono, A., & Suryandari, D. (2021). Accounting Analysis Journal The Analysis of Fraudulent Financial Reports Through Fraud Hexagon on Public Mining Companies. Accounting Analysis Journal, 10(3), 220–228. https://doi.org/10.15294/aaj.v10i3.54999 |

[30]

. A CEO who tends to be more satisfied if he shows his position to everyone so that his position can be taken into consideration and their sense of arrogance and superiority assumes that any policy cannot be bound because of the position he has Uciati & Mukhibad

.

Based on the description above, the following hypothesis is obtained:

H2: Arrogance effects on fraudulent financial Statements.

3.3. The Effect of Collusion on Fraudulent Financial Statement

Collusion refers to a fraudulent or compact agreement or agreement between two or more people. In this research, collusion is seen from cooperation with the government Vousinas

. Judging from agency theory, collaborating with government projects can result in financial losses. The greater the scale of government project collaboration between the company and the government, the greater the financial income the company receives, so that it can encourage agents (management) to take advantage by manipulating actual financial reports Lionardi & Suhartono

| [15] | Lionardi, M., & Suhartono, S. (2022). Pendeteksian Kemungkinan Terjadinya Fraudulent Financial Statement menggunakan Fraud Hexagon. Moneter - Jurnal Akuntansi Dan Keuangan, 9(1), 29–38. https://doi.org/10.31294/moneter.v9i1.12496 |

[15]

. The parties involved in collusion can be employees, a group of individuals spanning several organizations and jurisdictions or members of criminal organizations or special collectives Octaviani & Sagala

| [18] | Octaviani, K., & Sagala, E. (2021). The Influence Of Fraud Hexagon Elements On Fraudulent Financial Reporting At The Banking Companies Listed On The Indonesian Stock Exchange Periode 2018-2020. 18(6), 2273–2282. |

[18]

. Political relations can make borrowing easier, which can lead to an increase in the value of debt in the company. If the more loan funds a company receives, the more difficult it will be for the company to fulfill its debt repayment obligations, and this can result in the company being in a financial crisis.

Based on the explanation above, the hypothesis that can be carried out in these studies are:

H3: The collusion effects on fraudulent financial statements.

3.4. The Moderating Effect of Income Tax Rates Pressure, Arrogance, and Collusion in Fraudulent Financial Statements

The income tax rate that applies in a country can strengthen the occurrence of fraud, especially in financial reporting, and public companies that use income tax rates that are lower than the generally applicable rates will result in fraud in financial reporting. Meidijati & Amin

| [16] | Meidijati, & Amin, M. N. (2022). Detecting Fraudulent Financial Reporting Through Hexagon Fraud Model: Moderating Role of Income Tax Rate. International Journal of Social and Management Studies (IJOSMAS), 3(2), 311–322. http://www.ijosmas.org |

[16]

, also stated that High income taxes will lead to increasingly high and aggressive tax avoidance practices. Slemrod

explains that tax evasion is a taxpayer's action to avoid or reduce the amount of tax owed by using illegal financial engineering techniques such as committing fraud. Changes in tax rates can be exploited by management to gain profits and end up causing fraud in financial reports. Contingency theory states that there is no single approach to understanding the relationship between income tax rate and fraud which is used optimally to determine tax rates to minimize fraud. Instead, the best approach depends on the specific context and situation Kharie & Darwis

| [14] | Kharie, S. M., & Darwis, H. (2020). Moderation of Internal Control System in the Relationship Between Internal Auditor Competence and Organizational Justice of Fraud Prevention. Nominal: Barometer Riset Akuntansi Dan Manajemen, 9(1), 85–108. https://doi.org/10.21831/nominal.v9i1.30059 |

[14]

. Therefore, contingency theory suggests that optimal tax determination to minimize fraud must consider contextual factors such as economic conditions, tax system corporate culture, and the effectiveness of law enforcement. There is no one tax rate that fits all situations, an approach that is appropriate to the context or situation can be more effective in preventing fraud.

Based on the explanation above, the following hypothesis is obtained:

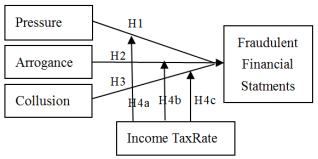

H4a: The income tax rates strengthen the influence of the pressure on the fraudulent financial statements.

H4b: The income tax rates strengthen the influence of arrogance on the fraudulent financial statements.

H4c: The income tax rates strengthen the influence of collusion on fraudulent financial statements.

Figure 1. Research Model.

4. Research Methods

This research uses a quantitative descriptive approach. This research uses a population of non-financial companies listed on the Indonesian Stock Exchange for the 2020-2022 period with a total sample of 69 companies and 207 observations accessed via www.idx.co.id. In taking samples using the purposive sampling method. The data collection technique used in this research is documentation. Data analysis used Eviews. The analysis technique used in this research was Moderated Regression Analysis (MRA). The tests carried out in the research were descriptive statistics, classical assumption tests including multicollinearity tests and heteroscedasticity tests, then R-Square tests and hypothesis tests were carried out. The equation model in this research is as follows.

Yit=α+β1pressureit+β2aroganceit+β3collusionit++β7itr+β1pressureit*itr+β2aroganceit*itr+β3collusionit*itr+e

5. Research Results

5.1. Descriptive Statistical

Descriptive statistical analysis is used to represent variable data that has been processed. The results of data processing for this research variable are presented in

table 1 as follows:

Table 1. Descriptive Statistic.

| M_SCORE | PRESSURE | ARROGANCE | COLLUSION | INCOME_TAX_RATE |

Mean | -1.286649 | 0.117184 | 0.603865 | 0.159420 | 0.316969 |

Med | -1.817964 | 0.063190 | 1.000000 | 0.000000 | 0.207989 |

Max | 15.42642 | 1.062489 | 1.000000 | 1.000000 | 6.758790 |

Min | -5.031414 | -0.275073 | 0.000000 | 0.000000 | 0.002017 |

Std.Dev. | 2.336466 | 0.178533 | 0.490279 | 0.366955 | 0.707962 |

Obs | 207 | 207 | 207 | 207 | 207 |

Source: Data Processed (Eviews, 2024)

Based on the results of descriptive statistical tests, the mean m-score (Y) value is -1,286, minimum -5,031, maximum 15,426. pressure (X1) shows a mean value of 0.117, minimum -0.275, maximum 1.062. arrogance (X2) shows a mean value of 0.603, a minimum of 0 and a maximum of 1. Collusion (X3) shows a mean value of 0.159, a minimum of 0 and a maximum of 1. Meanwhile, the income tax rate (Z) shows a mean value of 0.316, a minimum of 0.002 and a maximum of 6.758.

5.2. Classical Assumptions Test

Gujarati

| [9] | Gujarati, D. N. & D. C. P. (2015). Dasar-Dasar Ekonometrika (Edisi 5). Salemba Empat. |

[9]

, stated that in panel data regression not all classical assumption tests were carried out for certain reasons, so in this study the only classical assumption tests carried out were the multicollinearity test and heteroscedasticity test.

5.2.1. Multicollinearity Test

Multicollinearity test is presented in the

table 2.

Table 2. Multicollinearity test.

| PRESSURE | ARROGANCE | COLLUSION |

PRESSURE | 1.000000 | -0.040912 | -0.177829 |

ARROGANCE | -0.040912 | 1.000000 | 0.082902 |

COLLUSION | -0.177829 | 0.082902 | 1.000000 |

Source: Processed result, 2024

In

table 2 presented, this shows that the regression model used is free from multicollinearity because the correlation value of the independent variables is <10.

5.2.2. Heteroscedasticity Test

The heteroscedasticity test is presented in the

table 3.

Table 3. Heteroscedasticity test.

Variable | Coefficient | Std. Error | t-Statistic | Prob. |

C | 1.066425 | 0.174828 | 6.099868 | 0.0000 |

PRESSURE | -0.942874 | 0.777775 | -1.212272 | 0.2275 |

ARROGANCE | -0.082695 | 0.146538 | -0.564324 | 0.5735 |

COLLUSION | -0.205801 | 0.326997 | -0.629367 | 0.5302 |

Source: Data Processed, Eviews, 2024

Based on the Glesjer test results presented in

table 3, the probability value for each independent variable is > 0.05, which means the model used avoids symptoms of heteroscedasticity.

5.3. Hypothesis Test

This research uses moderated regression analysis (MRA) because this research uses moderating variables so that the panel data regression equation for the moderator variable using the MRA equation is presented in

table 4.

Based on the results of the tests carried out, it shows that the pressure variable has a P-value of 0.000 < 0.05. This shows that H1 is accepted. The test results in

table 4 show that the arrogance variable has a P-value of 0.0021 < 0.05. This shows that H2 is accepted. The third variable, collusion, has a P-value of 0.0069 < 0.05, which means H3 is accepted. Based on

table 4 regarding income tax rates as a pressure moderating variable, it shows a P-value of 0.0002 < 0.05. This shows that H4a is accepted.

In accordance with the results of the regression carried out, it shows that the income tax rate as a moderating variable for arrogance has a P-value of 0.0172 < 0.05. This means that H4b is accepted. The results of the regression test in

table 4 regarding income tax rates as a moderating variable for collusion show a P-value of 0.0223 < 0.05. which means H4c is accepted.

Table 4. Moderated Regression Analysis (MRA) Test.

Variable | Coefficient | Std. Error | t-Statistic | Prob. |

C | -0.615005 | 0.097683 | -6.295954 | 0.0000 |

PRESSURE | -8.957913 | 0.518215 | -17.28611 | 0.0000 |

ARROGANCE | 0.372242 | 0.118682 | 3.136463 | 0.0021 |

COLLUSION | 0.649873 | 0.236806 | 2.744330 | 0.0069 |

PRESSUREITR | 4.055572 | 1.058085 | 3.832936 | 0.0002 |

ARROGANCEITR | -0.462092 | 0.191454 | -2.413597 | 0.0172 |

COLLUSIONITR | 0.309970 | 0.134070 | 2.311995 | 0.0223 |

Source: Data Processed, Eviews, 2024

5.4. R-Square Test

The results of the R-square test in this research are presented in

table 5.

Table 5. R-Square Test.

R-squared | 0.880297 |

Adjusted R-squared | 0.813191 |

Source: Data Processed, Eviews, 2024

Based on the results of the regression test carried out, there is an R-Square value of 0.8802. This figure means that the dependent variable (Y), namely fraudulent financial statement, is influenced by independent variables, namely pressure, arrogance, and collusion, which are moderated by the income tax rate, which is 88.02%, while the remaining 11.08% is influenced by other variables in outside this research.

6. Discussion

6.1. The Effect of Pressure on Fraudulent Financial Statement

Based on the results of the tests carried out, it was obtained that the Pvalue was 0.008 < 0.05, this shows that pressure influences the condition of the financial statements. The pressure variable is proxied by financial targets, the high financial targets set by the company can be a pressure to achieve them because it does not rule out the possibility of events occurring to achieve the targets set.

The influence of pressure on financial reports is also in line with agency theory. Agency theory can be a basis for understanding the relationship between pressure due to a set financial target and the occurrence of action conditions. Financial targets set by the company that are too high can cause a conflict of interest between the principal and the agent which ultimately becomes a pressure for action on the condition of the financial statements Demetriades & Owusu-agyei

| [6] | Demetriades, P., & Owusu-agyei, S. (2022). Fraudulent fi nancial reporting : an application of fraud diamond to Toshiba’s accounting scandal. 29(2), 729–763. https://doi.org/10.1108/JFC-05-2021-0108 |

[6]

. According to Skousen

| [3] | Christopher J. Skousen, K. R. S., & Wright, J. (2009). Detecting and predicting financial statement fraud: The effectiveness of the fraud triangle and SAS No. 99. Corporate Governance and Firm Performance. https://doi.org/10.1108/S1569-3732(2009)0000013005 |

[3]

, when managers are deemed unable to achieve financial targets, managers will look for shortcuts to achieve them and do not rule out the possibility of manipulating financial reports to cover up deficiencies in achieving the targets that have been set. In addition, the higher the target set by the company, the greater the pressure experienced by managers because the target will be more difficult to achieve Yusrianti et al

| [34] | Yusrianti, H., Ghozali, I., Yuyetta, E., Aryanto, & Meirawati, E. (2020). Financial statement fraud risk factors of fraud triangle: Evidence from Indonesia. International Journal of Financial Research, 11(4), 36–51. https://doi.org/10.5430/ijfr.v11n4p36 |

[34]

.Therefore, pressure on achieving set targets can become pressure to carry out financial reporting conditions Fathmaningrum & Anggarani

| [7] | Fathmaningrum, E. S., & Anggarani, G. (2021). Fraud Pentagon and Fraudulent Financial Reportin : Evidence from Manufacturing Companies in Indonesia and Malaysia. 22(3). https://doi.org/10.18196/jai.v22i3.12538 |

[7]

.

The results of this research are consistent with research conducted by Demetriades & Owusu-agyei, Ozcelik, Octaviani & Sagala, Ratmono, Wicaksono & Suryandari, Yarana, Yusrianti et al supporting the influence of pressure proxied by financial targets on the condition of financial statements

| [6] | Demetriades, P., & Owusu-agyei, S. (2022). Fraudulent fi nancial reporting : an application of fraud diamond to Toshiba’s accounting scandal. 29(2), 729–763. https://doi.org/10.1108/JFC-05-2021-0108 |

| [18] | Octaviani, K., & Sagala, E. (2021). The Influence Of Fraud Hexagon Elements On Fraudulent Financial Reporting At The Banking Companies Listed On The Indonesian Stock Exchange Periode 2018-2020. 18(6), 2273–2282. |

| [20] | Ozcelik, H. (2020). An Analysis of Fraudulent Financial Reporting Using the Fraud Diamond Theory Perspective: An Empirical Study on the Manufacturing Sector Companies Listed on the Borsa Istanbul. In S. Grima, E. Boztepe, & P. J. Baldacchino (Eds.), Contemporary Issues in Audit Management and Forensic Accounting (Vol. 102, pp. 131–153). Emerald Publishing Limited. https://doi.org/10.1108/S1569-375920200000102012 |

| [24] | Ratmono, D., Darsono, D., & Cahyonowati, N. (2020). Financial Statement Fraud Detection With Beneish M-Score and Dechow F-Score Model: An Empirical Analysis of Fraud Pentagon Theory in Indonesia. International Journal of Financial Research, 11(6), 154. https://doi.org/10.5430/ijfr.v11n6p154 |

| [30] | Wicaksono, A., & Suryandari, D. (2021). Accounting Analysis Journal The Analysis of Fraudulent Financial Reports Through Fraud Hexagon on Public Mining Companies. Accounting Analysis Journal, 10(3), 220–228. https://doi.org/10.15294/aaj.v10i3.54999 |

| [31] | Yarana, C. (2023). Factors Influencing Financial Statement Fraud: An Analysis of the Fraud Diamond Theory from Evidence of Thai Listed Companies. WSEAS Transactions on Business and Economics, 20, 1659–1672. https://doi.org/10.37394/23207.2023.20.147 |

| [34] | Yusrianti, H., Ghozali, I., Yuyetta, E., Aryanto, & Meirawati, E. (2020). Financial statement fraud risk factors of fraud triangle: Evidence from Indonesia. International Journal of Financial Research, 11(4), 36–51. https://doi.org/10.5430/ijfr.v11n4p36 |

[6, 18, 20, 24, 30, 31, 34]

.

6.2. The Effect of Arrogance on Fraudulent Financial Statement

Based on the results of the tests carried out, it was obtained that the Pvalue was 0.021 <0.05, this shows that arrogance, which is proxied by the number of photos of the CEO, has an influence on financial report fraud. High arrogance can lead to fraud. In this case, the media plays a very important role in strengthening the image of a CEO, especially as a CEO will position himself as someone who has contributed to the company's achievements Khairani et al

| [12] | Khairani, S., Susetyo, D., Yusnaini, Y., & Yusrianti, H. (2024). Fraud Hexagon and Fraudulent Financial Reporting: The Role Of Power Distance. 21(S3), 824–845. www.migrationletters.com |

[12]

. High arrogance can lead to fraud. The nature of arrogance can be seen from the many photos of the CEO displayed. The higher the level of arrogance, the higher the possibility of fraud, because the higher the CEO's position, the more they feel they have a status and position which they think is crucial and important in the company, so that all internal regulations and controls will increase. not applicable Wicaksono & Suryandari

| [30] | Wicaksono, A., & Suryandari, D. (2021). Accounting Analysis Journal The Analysis of Fraudulent Financial Reports Through Fraud Hexagon on Public Mining Companies. Accounting Analysis Journal, 10(3), 220–228. https://doi.org/10.15294/aaj.v10i3.54999 |

[30]

.

This research is consistent with research Khamainy, Octaviani & Sagala, Utami, Uciati & Mukhibad which states that arrogance on the condition on fraudulent financial statements

| [13] | Khamainy, A. H., Ali, M., & Setiawan, M. A. (2022). Detecting fi nancial statement fraud through new fraud diamond model: the case of Indonesia. 29(3), 925–941. https://doi.org/10.1108/JFC-06-2021-0118 |

| [18] | Octaviani, K., & Sagala, E. (2021). The Influence Of Fraud Hexagon Elements On Fraudulent Financial Reporting At The Banking Companies Listed On The Indonesian Stock Exchange Periode 2018-2020. 18(6), 2273–2282. |

| [27] | Uciati, N., & Mukhibad, H. (2019). Fraudulent Financial Statements at Sharia Banks. 8(3), 198–206. https://doi.org/10.15294/aaj.v8i3.33625 |

| [28] | Utami, E. R. (2019). The Analysis of Fraud Pentagon Theory and Financial Distress for Detecting Fraudulent Financial Reporting in Banking Sector in Indonesia ( Empirical Study of Listed Banking Companies on Indonesia Stock Exchange in 2012-2017 ). 102(Icaf), 60–65. |

[13, 18, 27, 28]

.

6.3. The Effect of Collusion on Fraudulent Financial Statement

Based on the results of the tests carried out, it was obtained that the Pvalue was 0.0069 <0.05, this shows that collusion influences fraudulent financial statements. The collusion described regarding cooperation between companies and the government can influence fraudulent financial reporting, because the greater the project collaboration carried out, the higher the company's financial income, which has an impact on increasing the company Lionardi & Suhartono

| [15] | Lionardi, M., & Suhartono, S. (2022). Pendeteksian Kemungkinan Terjadinya Fraudulent Financial Statement menggunakan Fraud Hexagon. Moneter - Jurnal Akuntansi Dan Keuangan, 9(1), 29–38. https://doi.org/10.31294/moneter.v9i1.12496 |

[15]

. The greater the government project collaboration between the company and the government, the greater the financial income the company receives. Companies that collaborate with the government will more easily commit fraudulent acts to fulfill their interests in managing the company without thinking about their responsibilities and obligations, so this is in line with agency theory which explains that there is an inappropriate relationship between the company and the government. government. principal and agent Octaviani & Sagala

| [18] | Octaviani, K., & Sagala, E. (2021). The Influence Of Fraud Hexagon Elements On Fraudulent Financial Reporting At The Banking Companies Listed On The Indonesian Stock Exchange Periode 2018-2020. 18(6), 2273–2282. |

[18]

. Apart from that, cases of collusion are fraudulent activities that are very difficult to avoid and are comprehensive enough to be categorized as fraudulent acts Khairani et al

| [12] | Khairani, S., Susetyo, D., Yusnaini, Y., & Yusrianti, H. (2024). Fraud Hexagon and Fraudulent Financial Reporting: The Role Of Power Distance. 21(S3), 824–845. www.migrationletters.com |

[12]

.

This research is consistent with research conducted by Jannah & Rasuli and Octaviani & Sagala which stated that colluison influences fraudulent financial statement

| [11] | Jannah, V. M., & Rasuli, M. (2021). Pendekatan Vousinas Fraud Hexagon Model dalam Mendeteksi Kecurangan Pelaporan Keuangan. 4(1), 1–16. |

| [18] | Octaviani, K., & Sagala, E. (2021). The Influence Of Fraud Hexagon Elements On Fraudulent Financial Reporting At The Banking Companies Listed On The Indonesian Stock Exchange Periode 2018-2020. 18(6), 2273–2282. |

[11, 18]

.

6.4. The Moderating Effect of Income Tax Rates Pressure, Arrogance, and Collusion in Fraudulent Financial Statements

Based on the results of the moderated regression analysis test which was carried out to find out whether variable Z was able to moderate the relationship between the independent variable and the dependent variable. The results of the moderation test are concluded as follows:

1) The income tax rates strengthen influence of the pressure on the fraudulent financial statements.

Based on the results of the tests carried out, it shows that the pressure moderated by the income tax rate has a P value of 0.0002 <0.05. From these results it is concluded that income tax rates can moderate the influence of income tax rates on fraudulent financial statements. Income tax rates can strengthen the influence of pressure on fraudulent financial statements, this is because income tax rates are a factor in a company's obligations that must be fulfilled and can encourage fraudulent financial statements. One of the reasons why income tax rates can strengthen the influence of pressure on fraudulent financial statement is because the pressure that triggers fraudulent financial statement tends to be related to company performance targets, market expectations and other factors.

The theory that supports the income tax rate is the contingency theory, where the contingency theory explains that there is no single approach to understanding the relationship between the income tax rate and the pressure in the occurrence of fraudulent financial statements, the best approach is an approach that is appropriate to the context and situation Kharie & Darwis

| [14] | Kharie, S. M., & Darwis, H. (2020). Moderation of Internal Control System in the Relationship Between Internal Auditor Competence and Organizational Justice of Fraud Prevention. Nominal: Barometer Riset Akuntansi Dan Manajemen, 9(1), 85–108. https://doi.org/10.21831/nominal.v9i1.30059 |

[14]

. Therefore, contingency theory suggests that when setting tax rates, contextual factors such as economic conditions, corporate culture tax system and the effectiveness of law enforcement must be considered. There is no one tax rate that is suitable for all situations, and it is an approach that is appropriate to the context or situation that can be more effective in strengthening or influencing fraudulent actions.

2) The income tax rates strengthen influence of the arrogance on the fraudulent financial statements.

Based on the results of the tests carried out, it shows that arrogance moderated by the income tax rate has a P value of 0.0172 <0.05. From these results it is concluded that income tax rates can moderate the influence of arrogance on fraudulent financial statements. Income tax rates can strengthen the influence of arrogance on fraudulent financial statements, this is because the provisions on income tax rates can be a concern so that a CEO has a status and position which he thinks is crucial and important in the company under any assumptions. internal rules and controls do not apply to him. This is what gives rise to an arrogane attitude which is supported by income tax rates which can lead to fraudulent financial statement.

The theory that supports the income tax rate is the contingency theory, where the contingency theory explains that there is no single approach to understanding the relationship between the income tax rate and the pressure in the occurrence of fraudulent financial statements, the best approach is an approach that is appropriate to the context and situation Kharie & Darwis

| [14] | Kharie, S. M., & Darwis, H. (2020). Moderation of Internal Control System in the Relationship Between Internal Auditor Competence and Organizational Justice of Fraud Prevention. Nominal: Barometer Riset Akuntansi Dan Manajemen, 9(1), 85–108. https://doi.org/10.21831/nominal.v9i1.30059 |

[14]

. Therefore, contingency theory suggests that when setting tax rates, contextual factors such as economic conditions, corporate culture tax system and the effectiveness of law enforcement must be considered. There is no one tax rate that is suitable for all situations, and it is an approach that is appropriate to the context or situation that can be more effective in strengthening or influencing fraudulent actions.

3) The income tax rates strengthen the influence of collusion on fraudulent financial statements.

Based on the results of the tests carried out, it shows that collusion moderated by the income tax rate has a P value of 0.0223 <0.05. From these results it is concluded that income tax rates can moderate the effect of collusion on fraudulent financial statements. Income tax rates can strengthen the influence of collusion on fraudulent financial statement, this is partly because income tax rates have been determined in regulations and the presence of high tax rates can reduce company profits, resulting in companies having little funds and committing fraudulent acts. When the tax rate is low, management or shareholders will be more motivated to commit collusion aimed at increasing company profits. Thus, the influence of income tax rates on collusion can occur, but this depends on contextual factors such as company policy and the company environment.

The theory that supports the income tax rate is the contin-gency theory, where the contingency theory explains that there is no single approach to understanding the relationship between the income tax rate and the pressure in the occurrence of fraudulent financial statements, the best approach is an approach that is appropriate to the context and Kharie & Darwis

| [14] | Kharie, S. M., & Darwis, H. (2020). Moderation of Internal Control System in the Relationship Between Internal Auditor Competence and Organizational Justice of Fraud Prevention. Nominal: Barometer Riset Akuntansi Dan Manajemen, 9(1), 85–108. https://doi.org/10.21831/nominal.v9i1.30059 |

[14]

. Therefore, contingency theory suggests that when setting tax rates, contextual factors such as economic conditions, corporate culture tax system and the effectiveness of law enforcement must be considered. There is no one tax rate that is suitable for all situations, and it is an approach that is appropriate to the context or situation that can be more effective in strengthening or influencing fraudulent actions.

7. Conclusions

Based on the results and discussions previously presented in this research, it can be concluded that pressure, arrogance, and collusion have an influence on fraudulent financial statements. The pressure variable which is proxied by financial targets shows that the high financial targets set by the company can create pressure to achieve them, therefore it does not rule out the possibility that fraud will occur in achieving the targets that have been set.

Moreover, the arrogance which is proxied by the number of photos of the CEO, influences fraudulent financial statement because large or small numbers of CEO photos that appear in a company's annual report indicate an attitude of arrogance that thinks the rules or controls do not apply to it.

Furthermore, collusion also influences fraudulent financial statements. Collaboration described in the form of cooperation between companies and the government can influence fraudulent financial statement, because the greater the project collaboration carried out, the higher the company's financial income, which can encourage management to take advantage which results in fraudulent acts.

Meanwhile, the income tax rate can moderate pressure, arrogance, and collusion in influencing fraudulent financial statements. This is because the income tax rate is a fiscal policy set by the government to determine the amount of tax that must be paid by individuals or companies so that the income tax rate can cause fraudulent financial statements.

8. Limitations and Sugesstion

This research has a coefficient of determination (R2) of 88.02%, while the remaining 11.08% is influenced by other variables outside this research. Future researchers should add other variables, so that the range of variables tested is wider and the results obtained are better and more accurate. There are variables that are quite difficult to measure because of limitations in measurement, such as vanity. For future research, if we use the arrogance variable, it is hoped that we can use other measurements to make it more accurate and in-depth. And it is recommended for further research to add a research period to compare the influence of the variables used on fraudulent financial statements.

9. Implications of Research Results

The result of this research implies it can theoretically, this research provides a new perspective regarding pressure, arrogance and collusion regarding fraudulent financial statements moderated by the income tax rate. then this research also supports agency theory on the independent variable and contingency theory on the moderating variable. This research contributes to theory development, becomes a basis for further research and expands literature.

Another practically, this research can be useful in providing information for stakeholders such as investors to be able to avoid losses that may occur as well as material for consideration in terms of decision making through information conveyed through the entity's financial reports, then it can be useful for practitioners such as auditors and accountants as a preventive measure in detecting fraudulent financial statement.

Abbreviations

ACFE | Association of Certified Fraud Examiners |

CEO | Chief Executive Officer |

ITR | Income Tax Rate |

MRA | Moderated Regression Analysis |

Author Contributions

Nur Triyani: Data curation, Investigation, Visualization, Writing – original draft

Hasni Yusrianti: Data curation, Methodology, Supervision, Writing – review & editing

Kemas Muhammad Husni Thamrin: Data curation, Supervision

Conflicts of Interest

The authors declare no conflicts of interest.

References

| [1] |

Association of Certified Fraud Examiners (ACFE). (2022). Occupational Fraud 2022: A Report to the nations. Association of Certified Fraud Examiners, 1–96.

|

| [2] |

Betri Sirajuddin. (2020). Akuntansi Forensik dan Audit Investiasi (Edisi dua).

|

| [3] |

Christopher J. Skousen, K. R. S., & Wright, J. (2009). Detecting and predicting financial statement fraud: The effectiveness of the fraud triangle and SAS No. 99. Corporate Governance and Firm Performance.

https://doi.org/10.1108/S1569-3732(2009)0000013005

|

| [4] |

Company, P., Jensen, C., & Meckling, H. (1976). THEORY OF THE FIRM: MANAGERIAL BEHAVIOR, AGENCY COSTS AND OWNERSHIP STRUCTURE I. Introduction and summary In this paper WC draw on recent progress in the theory of (1) property rights, firm. In addition to tying together elements of the theory of e. 3, 305–360.

|

| [5] |

Crowe, H. (2011). Putting The Freud in Fraud: Why The Fraud Is No Longer Enough. IN Howarth, Crowe.

|

| [6] |

Demetriades, P., & Owusu-agyei, S. (2022). Fraudulent fi nancial reporting : an application of fraud diamond to Toshiba’s accounting scandal. 29(2), 729–763.

https://doi.org/10.1108/JFC-05-2021-0108

|

| [7] |

Fathmaningrum, E. S., & Anggarani, G. (2021). Fraud Pentagon and Fraudulent Financial Reportin : Evidence from Manufacturing Companies in Indonesia and Malaysia. 22(3).

https://doi.org/10.18196/jai.v22i3.12538

|

| [8] |

Fiedler. (1967). A Theory of Leadership Effectiveness. Advance in Experimental Social Psychology. Academic Press.

|

| [9] |

Gujarati, D. N. & D. C. P. (2015). Dasar-Dasar Ekonometrika (Edisi 5). Salemba Empat.

|

| [10] |

I Made Nova Dinata, Ni Nyoman Ayu Suryandari, I.. B. M. (n.d.). Analisis Fraud Diamond Dalam Mendeteksi Financial Statement Fraud. E-Journal Unmas, Vol 1 No 1.

|

| [11] |

Jannah, V. M., & Rasuli, M. (2021). Pendekatan Vousinas Fraud Hexagon Model dalam Mendeteksi Kecurangan Pelaporan Keuangan. 4(1), 1–16.

|

| [12] |

Khairani, S., Susetyo, D., Yusnaini, Y., & Yusrianti, H. (2024). Fraud Hexagon and Fraudulent Financial Reporting: The Role Of Power Distance. 21(S3), 824–845.

www.migrationletters.com

|

| [13] |

Khamainy, A. H., Ali, M., & Setiawan, M. A. (2022). Detecting fi nancial statement fraud through new fraud diamond model: the case of Indonesia. 29(3), 925–941.

https://doi.org/10.1108/JFC-06-2021-0118

|

| [14] |

Kharie, S. M., & Darwis, H. (2020). Moderation of Internal Control System in the Relationship Between Internal Auditor Competence and Organizational Justice of Fraud Prevention. Nominal: Barometer Riset Akuntansi Dan Manajemen, 9(1), 85–108.

https://doi.org/10.21831/nominal.v9i1.30059

|

| [15] |

Lionardi, M., & Suhartono, S. (2022). Pendeteksian Kemungkinan Terjadinya Fraudulent Financial Statement menggunakan Fraud Hexagon. Moneter - Jurnal Akuntansi Dan Keuangan, 9(1), 29–38.

https://doi.org/10.31294/moneter.v9i1.12496

|

| [16] |

Meidijati, & Amin, M. N. (2022). Detecting Fraudulent Financial Reporting Through Hexagon Fraud Model: Moderating Role of Income Tax Rate. International Journal of Social and Management Studies (IJOSMAS), 3(2), 311–322.

http://www.ijosmas.org

|

| [17] |

Nanda, A., Kemas M. Husni Thamrin, & Fida Muthia. (2024). Pengaruh Intellectual Capital terhadap Kinerja Perbankan Umum Konvensional di Indonesia. Al-Kharaj: Jurnal Ekonomi, Keuangan & Bisnis Syariah, 6(4), 4192–4216.

https://doi.org/10.47467/alkharaj.v6i4.926

|

| [18] |

Octaviani, K., & Sagala, E. (2021). The Influence Of Fraud Hexagon Elements On Fraudulent Financial Reporting At The Banking Companies Listed On The Indonesian Stock Exchange Periode 2018-2020. 18(6), 2273–2282.

|

| [19] |

Otley., D., T. (1980). The Contingency Theory of Management Accounting: Achievement and Prognosis. In Readings in Accounting for Management Control, 83-1–6.

|

| [20] |

Ozcelik, H. (2020). An Analysis of Fraudulent Financial Reporting Using the Fraud Diamond Theory Perspective: An Empirical Study on the Manufacturing Sector Companies Listed on the Borsa Istanbul. In S. Grima, E. Boztepe, & P. J. Baldacchino (Eds.), Contemporary Issues in Audit Management and Forensic Accounting (Vol. 102, pp. 131–153). Emerald Publishing Limited.

https://doi.org/10.1108/S1569-375920200000102012

|

| [21] |

Priantara, D. (2020). Fraud Auditing & Investigation.

|

| [22] |

Purba, B. P. (2015). Fraud dan Korupsi Pencegahan, Pendeteksian, dan Pemberantasannya (Cetakan Pe). Lestari Kiranatama.

|

| [23] |

Rahmatika, D. N. (2020). Fraud Auditing Kajian Teoritis dan Empiris (Penerbit: Deepublish).

|

| [24] |

Ratmono, D., Darsono, D., & Cahyonowati, N. (2020). Financial Statement Fraud Detection With Beneish M-Score and Dechow F-Score Model: An Empirical Analysis of Fraud Pentagon Theory in Indonesia. International Journal of Financial Research, 11(6), 154.

https://doi.org/10.5430/ijfr.v11n6p154

|

| [25] |

Saputri, S. B., & Sari, S. P. (2023). Fraudulent financial reporting using the testing of the hexagon fraud theory in manufacturing on the Indonesian Sharia Stock Index (ISSI). International Journal of Latest Research in Humanities and Social Science (IJLRHSS), 06(05), 297–306.

|

| [26] |

Slemrod, J. (2007). Cheating ourselves: The economics of tax evasion. Journal of Economic Perspectives, 21(1), 25–48.

https://doi.org/10.1257/jep.21.1.25

|

| [27] |

Uciati, N., & Mukhibad, H. (2019). Fraudulent Financial Statements at Sharia Banks. 8(3), 198–206.

https://doi.org/10.15294/aaj.v8i3.33625

|

| [28] |

Utami, E. R. (2019). The Analysis of Fraud Pentagon Theory and Financial Distress for Detecting Fraudulent Financial Reporting in Banking Sector in Indonesia ( Empirical Study of Listed Banking Companies on Indonesia Stock Exchange in 2012-2017 ). 102(Icaf), 60–65.

|

| [29] |

Vousinas, G. L. (2019). Advancing Theory of Fraud: the S. C. O. R. E. Model. Journal of Financial Crime.

https://doi.org/10.1108/JFC-12-2017-0128

|

| [30] |

Wicaksono, A., & Suryandari, D. (2021). Accounting Analysis Journal The Analysis of Fraudulent Financial Reports Through Fraud Hexagon on Public Mining Companies. Accounting Analysis Journal, 10(3), 220–228.

https://doi.org/10.15294/aaj.v10i3.54999

|

| [31] |

Yarana, C. (2023). Factors Influencing Financial Statement Fraud: An Analysis of the Fraud Diamond Theory from Evidence of Thai Listed Companies. WSEAS Transactions on Business and Economics, 20, 1659–1672.

https://doi.org/10.37394/23207.2023.20.147

|

| [32] |

Yuliani, umar hamdan, luk luk fuadah, thamrin K. H. (2021). Investment Opportunity Set, Dan Financing Mix: Penerbit Citrabooks.

|

| [33] |

Yusrianti, H., Ghozali, I., & N. Yuyetta, E. (2020). Asset Misappropriation Tendency: Rationalization, Financial Pressure, and the Role of Opportunity (Study in Indonesian Government Sector). Humanities & Social Sciences Reviews, 8(1), 373–382.

https://doi.org/10.18510/hssr.2020.8148

|

| [34] |

Yusrianti, H., Ghozali, I., Yuyetta, E., Aryanto, & Meirawati, E. (2020). Financial statement fraud risk factors of fraud triangle: Evidence from Indonesia. International Journal of Financial Research, 11(4), 36–51.

https://doi.org/10.5430/ijfr.v11n4p36

|

Cite This Article

-

APA Style

Triyani, N., Yusrianti, H., Thamrin, K. M. H. (2024). Collusion, Arrogance, and Pressure on Fraudulent Financial Statements: The Role of Income Tax Rate (Evidence from Indonesia). International Journal of Economic Behavior and Organization, 12(3), 114-122. https://doi.org/10.11648/j.ijebo.20241203.11

Copy

|

Copy

|

Download

Download

ACS Style

Triyani, N.; Yusrianti, H.; Thamrin, K. M. H. Collusion, Arrogance, and Pressure on Fraudulent Financial Statements: The Role of Income Tax Rate (Evidence from Indonesia). Int. J. Econ. Behav. Organ. 2024, 12(3), 114-122. doi: 10.11648/j.ijebo.20241203.11

Copy

|

Download

AMA Style

Triyani N, Yusrianti H, Thamrin KMH. Collusion, Arrogance, and Pressure on Fraudulent Financial Statements: The Role of Income Tax Rate (Evidence from Indonesia). Int J Econ Behav Organ. 2024;12(3):114-122. doi: 10.11648/j.ijebo.20241203.11

Copy

|

Download

-

@article{10.11648/j.ijebo.20241203.11,

author = {Nur Triyani and Hasni Yusrianti and Kemas Muhammad Husni Thamrin},

title = {Collusion, Arrogance, and Pressure on Fraudulent Financial Statements: The Role of Income Tax Rate (Evidence from Indonesia)

},

journal = {International Journal of Economic Behavior and Organization},

volume = {12},

number = {3},

pages = {114-122},

doi = {10.11648/j.ijebo.20241203.11},

url = {https://doi.org/10.11648/j.ijebo.20241203.11},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ijebo.20241203.11},

abstract = {Fraud in financial statements can have an impact on the accuracy and reliability of the use of financial statements, including affecting the amount of tax, fines paid, and the audit process. This study aims to analyze the effect of pressure, arrogance and collusion on financial statement fraud and the role of income tax rates as a moderating variable in non-financial companies listed on the Indonesia Stock Exchange in 2020-2022. The data in this study consisted of 207 research observations determined using purposive sampling method. Data collection was conducted through document analysis, using annual financial reports and annual reports. The analytical technique employed was regression analysis, moderated by Eviews. The study commenced with a descriptive statistical analysis, followed by an examination of the classical assumptions, including multicollinearity and heteroskedasticity. Finally, an analysis of moderated regression was conducted. The results of the regression analysis indicated that pressure, arrogance, and collusion were found to influence financial statement fraud. The moderated regression analysis demonstrated that the income tax rate was capable of moderating the influence of pressure, arrogance, and collusion on financial statement fraud. The theoretical implications of this study offer a novel perspective on the moderating effect of income tax rates on the relationship between pressure, arrogance and collusion and financial statement fraud. This study is of practical value and provides information that can inform decision-making for stakeholders.

},

year = {2024}

}

Copy

|

Download

-

TY - JOUR

T1 - Collusion, Arrogance, and Pressure on Fraudulent Financial Statements: The Role of Income Tax Rate (Evidence from Indonesia)

AU - Nur Triyani

AU - Hasni Yusrianti

AU - Kemas Muhammad Husni Thamrin

Y1 - 2024/07/02

PY - 2024

N1 - https://doi.org/10.11648/j.ijebo.20241203.11

DO - 10.11648/j.ijebo.20241203.11

T2 - International Journal of Economic Behavior and Organization

JF - International Journal of Economic Behavior and Organization

JO - International Journal of Economic Behavior and Organization

SP - 114

EP - 122

PB - Science Publishing Group

SN - 2328-7616

UR - https://doi.org/10.11648/j.ijebo.20241203.11

AB - Fraud in financial statements can have an impact on the accuracy and reliability of the use of financial statements, including affecting the amount of tax, fines paid, and the audit process. This study aims to analyze the effect of pressure, arrogance and collusion on financial statement fraud and the role of income tax rates as a moderating variable in non-financial companies listed on the Indonesia Stock Exchange in 2020-2022. The data in this study consisted of 207 research observations determined using purposive sampling method. Data collection was conducted through document analysis, using annual financial reports and annual reports. The analytical technique employed was regression analysis, moderated by Eviews. The study commenced with a descriptive statistical analysis, followed by an examination of the classical assumptions, including multicollinearity and heteroskedasticity. Finally, an analysis of moderated regression was conducted. The results of the regression analysis indicated that pressure, arrogance, and collusion were found to influence financial statement fraud. The moderated regression analysis demonstrated that the income tax rate was capable of moderating the influence of pressure, arrogance, and collusion on financial statement fraud. The theoretical implications of this study offer a novel perspective on the moderating effect of income tax rates on the relationship between pressure, arrogance and collusion and financial statement fraud. This study is of practical value and provides information that can inform decision-making for stakeholders.

VL - 12

IS - 3

ER -

Copy

|

Download