This research study delved into the multifaceted realm of tax compliance within the digital economy context, with a specific focus on the impact of digitalization, the role of taxpayer education programs, and the importance of taxpayer awareness programs. A diverse sample of 278 participants, encompassing individuals engaged in various digital businesses and taxpayers in Ghana, provided valuable insights through structured questionnaires. This study examined the complex area of tax compliance in the context of the digital economy, paying particular attention to the effects of digitalization, the function of taxpayer education initiatives, and the significance of taxpayer awareness campaigns. Through the use of structured questionnaires, a varied sample of 278 participants; including taxpayers in Ghana and those involved in a range of digital businesses, providing insightful answers. The study produced important results by using a robust Structural Equation Modelling (SEM) technique. It was discovered that digitization has a favourable impact on tax compliance, highlighting its capacity to act as a stimulant for improved compliance practices. Additionally, initiatives to raise taxpayer knowledge and education have become essential in encouraging tax compliance in the digital economy. The significance of thorough tax education programs and awareness efforts is shown by these findings. As a result, this study encourages stakeholders to take the initiative and makes suggestions for managers, legislators, academics, and business leaders to use digitalization's revolutionary potential to promote tax compliance. Future scholars are encouraged by this work to go deeper into this dynamic field in order to better understand how the digital economy affects taxation and compliance.

| Published in | International Journal of Business and Economics Research (Volume 14, Issue 1) |

| DOI | 10.11648/j.ijber.20251401.11 |

| Page(s) | 1-25 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2025. Published by Science Publishing Group |

Taxation, Digitalization, Structural Equation Modelling (SEM), Tax Compliance, Digital Economy, Ghana Revenue Authority (GRA)

N | % | ||

|---|---|---|---|

18-25 years | 16 | 5.8 | |

Age | 26-35 years | 113 | 40.6 |

36-45 years | 117 | 42.1 | |

46-55 years | 32 | 11.5 | |

Total | 278 | 100 | |

Male | 179 | 64.4 | |

Gender | Female | 99 | 35.6 |

Total | 278 | 100 | |

Diploma/Certificate | 32 | 11.5 | |

Educational Qualification | Bachelor's Degree | 131 | 47.1 |

Master's Degree | 115 | 41.4 | |

Total | 278 | 100 | |

Employed | 246 | 88.5 | |

Occupation | Self-employed | 16 | 5.8 |

Unemployed | 16 | 5.8 | |

Below GHS 1,000 | 16 | 5.8 | |

GHS 1,001 - GHS 3,000 | 33 | 11.9 | |

Monthly Income (in local currency) | GHS 3,001 - GHS 5,000 | 50 | 18.0 |

GHS 5,001 - GHS 10,000 | 48 | 17.3 | |

Above GHS 10,000 | 131 | 47.1 | |

Total | 278 | 100 | |

E-commerce | 100 | 36.0 | |

Type of Digital Business (if applicable) | Freelancing/Gig Economy | 16 | 5.8 |

Digital Services | 32 | 11.5 | |

Online Retail | 16 | 5.8 | |

Digital Content Creation | 114 | 41.0 | |

Total | 278 | 100 | |

Less than 1 year | 32 | 11.5 | |

1-3 years | 116 | 41.7 | |

Years of Experience in Digital Business (if applicable) | 4-6 years | 49 | 17.6 |

7-10 years | 33 | 11.9 | |

More than 10 years | 48 | 17.3 | |

Total | 278 | 100 | |

Daily | 197 | 70.9 | |

Frequency of Digital Transactions | Weekly | 48 | 17.3 |

Monthly | 17 | 6.1 | |

Occasionally | 16 | 5.8 | |

Total | 278 | 100 | |

Very Familiar | 113 | 40.6 | |

Somewhat Familiar | 17 | 6.1 | |

Familiarity with Digital Tax Reporting a | Neutral | 66 | 23.7 |

Not Very Familiar | 50 | 18.0 | |

Not Familiar at All | 32 | 11.5 | |

Total | 278 | 100 | |

Have you used e-filing for tax reporting? | Yes | 213 | 76.6 |

No | 65 | 23.4 | |

Total | 278 | 100 | |

Have you attended any taxpayer education programs in the past? | Yes | 213 | 76.6 |

No | 65 | 23.4 | |

Total | 278 | 100 | |

Fully Compliant | 49 | 17.6 | |

How would you rate your level of tax compliance in the digital economy? | Mostly Compliant | 116 | 41.7 |

Neutral | 81 | 29.1 | |

Occasionally Compliant | 16 | 5.8 | |

Not Compliant at All | 16 | 5.8 | |

Total | 278 | 100 |

Mean | Std. Deviation | Correlations | Tax compliance | Digitalization | Role of taxpayer education | Role of tax payer awareness | Role of ethical considerations | |

|---|---|---|---|---|---|---|---|---|

Tax compliance | 4.1033 | .62675 | Pearson Correlation | 1 | ||||

Digitalization | 4.0807 | .62183 | Pearson Correlation | .621** | 1 | |||

Role of taxpayer education | 4.1367 | .59771 | Pearson Correlation | .491** | .287** | 1 | ||

Role of tax payer awareness | 4.1527 | .64554 | Pearson Correlation | .261** | .234** | .669** | 1 | |

Role of ethical considerations | 4.1706 | .58327 | Pearson Correlation | .242** | .158** | .478** | .587** | 1 |

CONSTRUCTS | ITEMS | FL | CA | CR | AVE |

|---|---|---|---|---|---|

DIG1 | 0.886 | 0.920 | 0.988 | 0.703 | |

DIG2 | 0.895 | ||||

Digitalization | DIG3 | 0.871 | |||

DIG4 | 0.872 | ||||

DIG5 | 0.761 | ||||

DIG6 | 0.731 | ||||

TC1 | 0.772 | 0.914 | 0.960 | 0.642 | |

TC2 | 0.713 | ||||

Tax Compliance | TC3 | 0.821 | |||

TC4 | 0.787 | ||||

TC5 | 0.882 | ||||

TC6 | 0.793 | ||||

TC7 | 0.831 | ||||

TPA1 | 0.841 | 0.937 | 0.941 | 0.726 | |

TPA2 | 0.815 | ||||

Taxpayer Awareness | TPA3 | 0.908 | |||

TPA4 | 0.887 | ||||

TPA5 | 0.912 | ||||

TPA6 | 0.828 | ||||

TPA7 | 0.766 | ||||

TPE1 | 0.736 | 0.888 | 0.889 | 0.599 | |

Taxpayer Education | TPE2 | 0.755 | |||

TPE3 | 0.811 | ||||

TPE4 | 0.840 | ||||

TPE5 | 0.815 | ||||

TPE6 | 0.743 | ||||

TPE7 | 0.707 |

DIG | TC | TPA | |

|---|---|---|---|

TC | 0.597 | ||

TPA | 0.241 | 0.269 | |

TPE | 0.268 | 0.589 | 0.557 |

DIG | TC | TPA | TPE | |

|---|---|---|---|---|

DIG | 0.845 | |||

TC | 0.552 | 0.811 | ||

TPA | 0.223 | 0.252 | 0.853 | |

TPE | 0.248 | 0.534 | 0.507 | 0.835 |

DIG | TC | TPA | TPE | |

|---|---|---|---|---|

DIG1 | 0.855 | 0.430 | 0.253 | 0.198 |

DIG2 | 0.853 | 0.395 | 0.261 | 0.201 |

DIG3 | 0.863 | 0.407 | 0.177 | 0.178 |

DIG4 | 0.855 | 0.546 | 0.192 | 0.270 |

DIG5 | 0.819 | 0.453 | 0.151 | 0.186 |

DIG6 | 0.825 | 0.525 | 0.120 | 0.206 |

TC1 | 0.539 | 0.838 | 0.195 | 0.350 |

TC2 | 0.508 | 0.810 | 0.158 | 0.378 |

TC3 | 0.484 | 0.878 | 0.190 | 0.381 |

TC4 | 0.468 | 0.858 | 0.168 | 0.343 |

TC6 | 0.313 | 0.726 | 0.228 | 0.515 |

TC7 | 0.368 | 0.746 | 0.276 | 0.606 |

TPA1 | 0.199 | 0.228 | 0.856 | 0.490 |

TPA2 | 0.235 | 0.221 | 0.829 | 0.434 |

TPA3 | 0.184 | 0.204 | 0.913 | 0.453 |

TPA4 | 0.157 | 0.186 | 0.886 | 0.422 |

TPA5 | 0.226 | 0.242 | 0.911 | 0.474 |

TPA6 | 0.136 | 0.165 | 0.810 | 0.356 |

TPA7 | 0.171 | 0.234 | 0.753 | 0.369 |

TPE1 | 0.230 | 0.485 | 0.305 | 0.817 |

TPE2 | 0.218 | 0.467 | 0.378 | 0.833 |

TPE3 | 0.206 | 0.438 | 0.445 | 0.867 |

TPE4 | 0.184 | 0.442 | 0.509 | 0.850 |

TPE5 | 0.193 | 0.384 | 0.503 | 0.806 |

VIF | |

|---|---|

DIG1 | 4.157 |

DIG2 | 3.634 |

DIG3 | 3.386 |

DIG4 | 2.635 |

DIG5 | 2.327 |

DIG6 | 2.338 |

TC1 | 2.892 |

TC2 | 2.726 |

TC3 | 3.305 |

TC4 | 2.988 |

TC6 | 1.899 |

TC7 | 1.905 |

TPA1 | 3.177 |

TPA2 | 2.964 |

TPA3 | 3.029 |

TPA4 | 4.331 |

TPA5 | 2.388 |

TPA6 | 2.585 |

TPA7 | 1.998 |

TPE1 | 2.264 |

TPE2 | 2.469 |

TPE3 | 2.718 |

TPE4 | 2.967 |

TPE5 | 2.487 |

R-square | R-square adjusted | |

|---|---|---|

TC | 0.478 | 0.473 |

Hypothesis | Coefficient | T statistics | P values | Commence |

|---|---|---|---|---|

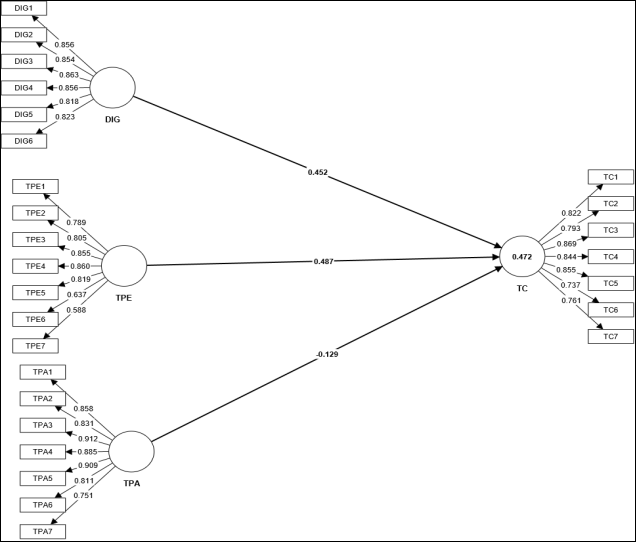

DIG -> TC | 0.452 | 8.544 | 0.000 | Accepted |

TPA -> TC | -0.129 | 2.381 | 0.017 | Accepted |

TPE -> TC | 0.487 | 7.729 | 0.000 | Accepted |

f-square | |

|---|---|

DIG -> TC | 0.370 |

TPA -> TC | 0.010 |

TPE -> TC | 0.298 |

Saturated model | Estimated model | |

|---|---|---|

SRMR | 0.090 | 0.156 |

d_ULS | 4.282 | 12.776 |

d_G | 1.529 | 1.672 |

Chi-square | 2214.165 | 2353.679 |

NFI | 0.724 | 0.707 |

Q²predict | RMSE | MAE | |

|---|---|---|---|

TC | 0.461 | 0.740 | 0.559 |

AI | Artificial Intelligence |

AVE | Average Variance Extracted |

BEPS | Base Erosion and Profit Shifting |

CR | Composite Reliability |

COVID-19 | Corona Virus Pandemic of 2019 |

DAI | Digital Adoption Index |

DIG | Digitalization |

DST | Digital Sales Tax |

EU | European Union |

FL | Factor Loading |

GFI | Goodness-Fit Index |

GOF | Goodness-of-Fit |

GRA | Ghana Revenue Authority |

GST | Goods and Services Tax |

HMRC | Her Majesty Revenue and Custom |

HTMT | Heterotrait-Monotrait Ratio |

ICT | Information and Communication Technology |

IMF | International Monetary Fund |

IT | Information Technology |

MAE | Mean Absolute Error |

MSME | Micro Small and Medium Enterprises |

MTD | Maximum Tolerable Downtime |

OECD | Organisation for Economic Cooperation and Development |

PLS-SEM | Partial Least Square-Structural Equation Modelling |

RMSE | Root Mean Square Error |

SEM | Structural Equation Modelling |

SMEs | Small and Medium Enterprises |

TAM | Technology Acceptance Model |

TC | Tax Compliance |

TPA | Taxpayer Awareness |

TPE | Taxpayer Education |

VAT | Value Added Tax |

| [1] | Wadesango, N., Chibanda, D. M., & Wadesango, V. O. (2020). Assessing the impact of digital economy taxation in revenue generation in Zimbabwe. Academy of Accounting and Financial Studies Journal, 24(3), 1–11. |

| [2] | Saruji, S., & Hamid, N. (2021). Tax Agents’ Acceptance of the Digitalisation of Tax Administration in Malaysia. |

| [3] | Pemerathna, A. H. S. (2017). Economic Impact of Digital Taxation: A Case on Information Communication Technology Industry Sri Lanka. SSRN Electronic Journal, 325–346. |

| [4] | IOTA. (2018). Impact of Digitalization: on the Transformation of Tax Administration (Issue June). |

| [5] |

OECDA. (2018). Tax and Digitalisation. OECD/G20 Base Erosion, 3(10), 5.

https://www.oecd.org/going-digital/tax-and-digitalisation.pdf |

| [6] | Lugli, E., & Bertacchini, F. (2022). Audit quality and digitalization: some insights from the Italian context. Meditari Accountancy Research, 1981. |

| [7] | Ihnatišinová, D. (2021). Digitalization of tax administration communication under the effect of global megatrends of the digital age. SHS Web of Conferences, 92(2021), 02022. |

| [8] | Jacobs, B. (2018). Digitalization and Taxation. Digital Revolutions in Public Finance, Mirrlees, 121. |

| [9] | Fanea-Ivanovici, M., Muşetescu, R.-C., Pană, M.-C., & Voicu, C. (2019). Fighting Corruption and Enhancing Tax Compliance through Digitization: Achieving Sustainable Development in Romania. Sustainability, 11(5), 1480. |

| [10] | Sadiq, M. (2021). Impact of making tax digital on small businesses. Journal of Accounting and Taxation, 13(4), 304–316. |

| [11] | Erin. (2021). The Effectiveness of Tax Administration Digitalization to Reduce Compliance Cost Taxpayers of Micro Small, and Medium Enterprises. Budapest International Research and Critics Institute - Journal (BIRCI-Journal), 4(4), 7508–7515. |

| [12] | Gangodawilage, D. (2021). Use of Technology to Manage Tax Compliance Behavior of Entrepreneurs in the Digital Economy. International Journal of Scientific and Research Publications (IJSRP), 11(3), 366–371. |

| [13] | Hadzhieva, E. (2019). Impact of Digitalisation on International Tax Matters - Challenges and Remedies. Policy Department for Economic, Scientific and Quality of Life Policies, February, 85. |

| [14] | Strango, C. (2021). "Does Digitalisation in Public Services Reduce Tax Evasion?" Economic Research Guardian, Weissberg Publishing, Vol. 11(2), pages 221-235. |

| [15] | Sentanu, I. N. W., & Budiartha, K. (2019). Effect of taxation modernization on tax compliance. International Research Journal of Management, IT and Social Sciences, 6(4), 207–213. |

| [16] | Mpofu, F. Y. & Moloi, T. (2022). Direct Digital Services Taxes in Africa and the Canons of Taxation. Laws, Vol. 11(4), pp 57. |

| [17] | Yamen, A., Coskun, A., & Mersni, H. (2022a). Digitalization and tax evasion: the moderation effect of corruption. Economic Research-Ekonomska Istrazivanja, 0(0), 1–24. |

| [18] | Hendayana, Y., Mulyadi, H., Reyta, F., & Halim, R. A. (2021). How Perception use of e-Filling Technology Enhance Knowledge of Indonesian Disability Taxpayers and Impact Tax Compliance. Budapest International Research and Critics Institute (BIRCI-Journal): Humanities and Social Sciences, 4(2), 1687–1696. |

| [19] | Paoki, A. G. F., Yusha, J. D., Kale, S. E., & Mangoting, Y. (2021). The Effect Of Information Technology And Perceived Risk In Anticipating Tax Evasion. Jurnal Reviu Akuntansi Dan Keuangan, 11(2), 238–249. |

| [20] | Musimenta, D., Nkundabanyanga, S., Muhwezi, M., Akankunda, B., & Nalukenge, I. (2017). Tax compliance of small and medium enterprises: a developing country perspective. Journal of Financial Regulation and Compliance, 25(2), 149-175. |

| [21] | Carsamer, E. and Abbam, A. (2020). Religion and tax compliance among smes in Ghana. Journal of Financial Crime, 30(3), 759-775. |

| [22] | Koranteng, E., Osei-Bonsu, E., Ameyaw, F., Ameyaw, B., Agyeman, J., & Dankwa, R. (2017). The effects of compliance and growth opinions on smes compliance decisions: an empirical evidence from Ghana. Open Journal of Business and Management, 05(02), 230-243. |

| [23] | Nartey, E. (2023). Tax compliance of small and medium sized enterprises in Ghana. International Journal of Sociology and Social Policy, 43(11/12), 1063-1083. |

| [24] | Agyekum, C. (2023). Determinants of the tax compliance and fairness perceptions of taxpayers on the online tax system. a case of Ghana. |

| [25] | Amponsah, S. and Adu, K. (2017). Socio-demographics of tax stamp compliance in upper denkyira east municipal and upper denkyira west district in Ghana. International Journal of Law and Management, 59(6), 1315-1330. |

| [26] | Baba, S. (2022). The effects of economic factors on tax compliance by small and medium enterprises of tamale metropolis in Ghana. Asian Journal of Economics Business and Accounting, 44-53. |

| [27] | Bruce-Twum, E. (2023). Smes tax compliance behaviour in emerging economies: do tax compliance costs matter? evidence from Ghana. JAEPP, 24(2). |

| [28] | Peprah, J., Andoh, F., Avorkpo, E., Dafor, K., Afful, B., & Obeng, C. (2022). Compliance burden and tax gap among micro and small businesses: evidence from Ghana. Sage Open, 12(4), 215824402211269. |

| [29] | Ababio, A. and Mangueye, A. (2021). State legitimacy and tax compliance among small and medium scale enterprises: a case study of dodowa district, Ghana. Journal of Financial Crime, 28(3), 858-869. |

| [30] | Malik, R., Mulyatini, N., Akbar, D., & Rizkia, T. (2023). How digital tax socialization moderates e-filling against individual taxpayer compliance. E-Jurnal Akuntansi, 33(3), 715. |

| [31] | Hermawan, P. (2022). A study of trust base voluntary tax compliance through tax administration digital transformation in Indonesia. International Journal of Current Science Research and Review, 05(08). |

| [32] | Oppong, F. (2021). An analysis of the impact of jurisdictional fragmentation on property taxes in Ghana. Journal of Financial Management of Property and Construction, 26(2), 219-235. |

| [33] | Ntiamoah, J., Asare, J., Arhenful, P., & Owusu-Mensah, M. (2023). Taxing in a pandemic: an assessment of the impact of covid-19 pandemic on tax revenues and revenues of small and medium enterprises in Ghana. |

| [34] | Jolodar, S., Ahmadi, M., & Imankhan, N. (2019). Presenting the model of tax compliance: the role of social-psychological factors. Asia-Pacific Management Accounting Journal, 14(2), 139-160. |

| [35] | Deloitte. (2015). Digital inclusion and mobile sector taxation in Ghana. February, 5 & 19. |

| [36] | Knebelmann, J. (2022). Digitalisation of property taxation in developing countries Recent advances and remaining challenges. June. |

| [37] | Bellon, M., Dabla-Norris, E., Khalid, S., & Lima, F. (2022). Digitalization to improve tax compliance: Evidence from VAT e-Invoicing in Peru. Journal of Public Economics, 210, 104661. |

| [38] | Ouedraogo, R. & Sy, A. (2020). Can Digitalization Help Deter Corruption in Africa? IMF Working Paper No. 20/68. SSRN: |

| [39] | Bassongui, N. (2023). Impacts of Tax Digitalisation on Tax Revenues in Sub-Saharan Africa: A Systematic Review. 1–10. Research Square. |

| [40] | Etim, R. S., Jeremiah, M. S., & B. S. Dan, P. (2020a). Tax Compliance and Digitalization of Nigerian Economy: The Empirical Review. American International Journal of Social Science, 9(2). |

| [41] | Fossung, M. F., & Chi, N. W. (2022). An Assessment of Tax Digitalisation and Tax Compliance Relationship in Cameroon: The Mediating Role of Behavioural Intentions. Journal of Finance and Accounting, 10(1), 30. |

| [42] | Gangodawilage, D., Madurapperuma, W. & Aluthge, C. (2021). Use of Technology to Manage Tax Compliance Behavior of Entrepreneurs in the Digital Economy. International Journal of Scientific and Research Publications, Volume 11, Issue 3, March 2021 366-370. ISSN 2250-3153, |

| [43] | Hamza, P. A., Qader, K. S., Gardi, B., Hamad, H. A., & Anwar, G. (2021). Analysis the impact of Information technology on Efficient tax Management. International Journal of Advanced Engineering, Management and Science, 7(9), 31–41. |

| [44] | Gangl, K., & Torgler, B. (2020). How to Achieve Tax Compliance by the Wealthy: A Review of the Literature and Agenda for Policy. Social Issues and Policy Review, 14(1), 108–151. |

| [45] | Shakkour, A. S. K., Almohtaseb, A. A., Matahen, R. K., & Sahkkour, N. A. S. (2021). Factors influencing the value added tax compliance in small and medium enterprises in Jordan. Management Science Letters, 11, 1317–1330. |

| [46] | Abina, S., Amaning, N., Osei Anim, R., Kyere, A., & Kwakye, G. (2021). Tax Compliance among Ghanaian SMEs: How impactful is Taxpayer Education? International Journal of Academic Research in Accounting, Finance and Management Sciences, 10(4), 40–58. |

| [47] | Bornman, M., & Ramutumbu, P. (2019). A conceptual framework of tax knowledge. Meditari Accountancy Research, 27(6), 823–839. |

| [48] | Torgler, B., Schaffner, M., & Macintyre, A. (2007). Tax Compliance, Tax Compliance, Tax Morale and Government Quality. Andrew Young School of Policy Studies, December, 07–27. |

| [49] | Pandita, S., Garg, A., Kumar, S., Das, S. and Gaur, M. P. (2024). The Impact of HR Technologies on Digital Library Staff Efficiency and Engagement. Library Progress International. Vol. 44 No. 3, LIB PRO. |

| [50] | Cummings, R. G., Martinez-Vazquez, J., McKee, M., & Torgler, B. (2009). Tax morale affects tax compliance: Evidence from surveys and an artefactual field experiment. Journal of Economic Behavior and Organization, 70(3), 447–457. |

| [51] | Le, H. T. H., Tuyet, V. T. B., Hanh, C. T. B., & Do, Q. H. (2020). Factors affecting tax compliance among small-and medium-sized enterprises: Evidence from vietnam. Journal of Asian Finance, Economics and Business, 7(7), 209–217. |

| [52] | Adhiambo, O. J., & Theuri, J. M. (2019). Effect of Taxpayer Awareness and Compliance Cost on Tax Compliance Among Small Scale Traders in Nakuru. International Academic Journal of Economics and Finance, 3(3), 279–295. |

| [53] | Nurkhin, A., Novanty, I., Muhsin, M., & Sumiadji, S. (2018). The Influence of Tax Understanding, Tax Awareness and Tax Amnesty toward Taxpayer Compliance. Jurnal Keuangan Dan Perbankan. |

| [54] | Susuawu, D., Ofori-Boateng, K., & Amoh, J. K. (2020). Does Service Quality Influence Tax Compliance Behaviour of Smes? a New Perspective From Ghana. International Journal of Economics and Financial Issues, 10(November), 50–56. |

| [55] | Frey, B. S. & Torgler, B. (2007). Tax morale and conditional cooperation. Journal of Comparative Economics 35(1) 136–159. ScienceDirect, Elsevier Inc. |

| [56] | Kitsios, E., Jalles, J. T., & Verdier, G. (2022). Tax evasion from cross-border fraud: does digitalization make a difference? Applied Economics Letters. |

| [57] | OECD (2015), Addressing the Tax Challenges of the Digital Economy, Action 1 - 2015 Final Report, OECD/G20 Base Erosion and Profit Shifting Project, OECD Publishing, Paris, |

| [58] | Richardson, G. (2006). Determinants of tax evasion: A cross-country investigation. Journal of International Accounting, Auditing and Taxation. 15(2): 150–69. |

| [59] | Atayah, O. F., & Alshater, M. M. (2021). Audit and tax in the context of emerging technologies: A retrospective analysis, current trends, and future opportunities. International Journal of Digital Accounting Research, 21(November 2020), 95–128. |

| [60] | Commerce, I. chamber of. (2021). ICC BRITACOM report: Digitalisation of tax administrations: A business perspective. Frontiers in Neuroscience, 14(1), 1–13. |

| [61] | Mascagni, G., Mengistu, A. T., & Woldeyes, F. B. (2021). Can ICTs increase tax compliance? Evidence on taxpayer responses to technological innovation in Ethiopia. Journal of Economic Behavior and Organization, 189, 172–193. |

| [62] | Muturi, H. M. (2015). Effects of online tax system on tax compliance among small taxpayers in Meru County, Kenya. Intermational Journal of Economics, Commerce and Management, III (12), 280–297. |

| [63] | Alharbi, S., & Drew, S. (2014). Using the Technology Acceptance Model in Understanding Academics’ Behavioural Intention to Use Learning Management Systems. International Journal of Advanced Computer Science and Applications, 5(1), 143–155. |

| [64] | Davis, F. D. (1989). Perceived Usefulness, Perceived Ease of Use, and User Acceptance of Information Technology. MIS Quarterly. Management Information Systems Research Centre, University of Minnesota. Vol. 13, No. 3, pp. 319-340. JSTOR Collection. |

| [65] | Agbadi, S. B. (2011). Determinants of Tax Compliance: A case study of Vat Flat Rate Scheme Traders in the Accra Metropolis. 1–93. |

| [66] | McGee, R. W. (2013). The ethics of tax evasion: Perspectives in theory and practice. In The Ethics of Tax Evasion: Perspectives in Theory and Practice. |

| [67] | Sadress, N., Bananuka, J., Orobia, L., & Opiso, J. (2019). Antecedents of tax compliance of small business enterprises: a developing country perspective. International Journal of Law and Management, 61(1), 24–44. |

| [68] | Lim, Y. (2011). Tax avoidance, cost of debt and shareholder activism: Evidence from Korea. Journal of Banking and Finance. |

| [69] | Roy, P., & Khan, M. H. (2021). Digitizing Taxation and Premature Formalization in Developing Countries. Development and Change, 52(4), 855–877. |

| [70] | Mpofu, F. Y. (2022). Taxing the Digital Economy through Consumption Taxes (VAT) in African Countries: Possibilities, Constraints and Implications. International Journal of Financial Studies, 10(3). |

| [71] | Alm, J. & Torgler, B., 2006. Culture differences and tax morale in the United States and in Europe. Journal of Economic Psychology 27, 224–246. |

| [72] | de Jong, P. (2011). Design research. In CTBUH Journal. |

| [73] | Grösser, S. N. (2013). Research design. In Contributions to Management Science. |

| [74] | Morgan, D. L. (2014). Pragmatism as a Paradigm for Social Research. Qualitative Inquiry. |

| [75] | Yin, R. K. (2003). Case Study Research: Design and Methods. Australasian Emergency Nursing Journal. |

| [76] | Faizi M. F., Dirseciu, P., Robinson, J. R., Freund, H., Bergbau, V. B. B. & Jose Perona, J. (2017). Application of Information Technology in Increasing Effectiveness, Efficiency and Productivity of Companies. Scientific Journal of Unitary Management, vol. 1 no. 1, p. 43, 2017, |

| [77] | Babbie, E. R. (2016). The Practice of Social Research. 14th Edition, Cengage Learning, Belmont. |

| [78] | Creswell, J. W. (2014). Research Design: Qualitative, Quantitative and Mixed Methods Approaches (4th ed.). Thousand Oaks, CA: Sage. |

| [79] | de Vaus, D. (2014). Surveys in social research (6th ed.). Routledge/Taylor & Francis Group. |

| [80] | Fowler Jr., F. J. (2013) Survey Research Methods. Sage Publications, New York. |

| [81] | Sileyew, K. J. (2019). Research Design and Methodology. |

| [82] | Hair, J. F., Risher, J. J., Sarstedt, M. & Ringle, C. M. (2019) When to Use and How to Report the Results of PLS-SEM. European Business Review, 31, 2-24. |

| [83] | Kock, N., & Lynn, G. (2012). Lateral Collinearity and Misleading Results in Variance-Based SEM: An Illustration and Recommendations. Journal of the Association for Information Systems, 13, 546-580. |

| [84] | Asiamah, N., Mensah, H. K., & Oteng-Abayie, E. F. (2017). Do Larger Samples Really Lead to More Precise Estimates? A Simulation Study. 5(January), 9–17. |

| [85] | Ranatunga, R. V. S. P. K., Priyanath, H. M. S., & Megama, R. G. N. (2020). Methods and Rule-Of-Thumbs in The Determination of Minimum Sample Size When Appling Structural Equation. Journal of Social Science Research, 15, 102–109. |

| [86] | Rahman, M. (2023). Sample size determination for survey research and non-probability sampling techniques: a review and set of recommendations. Journal of Entrepreneurship, Business and Economics, 11(1), 42–62. |

| [87] | Krejcie, R. V., & Morgan, D. W., (1970). Determining Sample Size for Research Activities. Educational and Psychological Measurement. |

| [88] | Durrah, O. (2021). How to use Smart PLS software ? Structural Equation Modelling (SEM). March. |

| [89] | Hussain, S., Fangwei, Z., Siddiqi, A. F., Ali, Z., & Shabbir, M. S. (2018). Structural Equation Model for evaluating factors affecting quality of social infrastructure projects. Sustainability (Switzerland), 10(5), 1–25. |

| [90] | Alharbi, R. K., Yahya, S. Bin, & Kassim, S. (2021). Impact of religiosity and branding on SMEs performance: does financial literacy play a role? Journal of Islamic Marketing. |

| [91] | Fornell, C., & Larcker, D. F. (1981). Structural Equation Models with Unobservable Variables and Measurement Error: Algebra and Statistics. Journal of Marketing Research, 18, 382-388. |

| [92] | Wong, K. K. (2013) Partial Least Squares Structural Equation Modeling (PLS-SEM) Techniques Using SmartPLS. Marketing Bulletin, 24, 1-32. |

| [93] | Afthanorhan, W. (2014) Hierarchical Component Using Reflective-Formative Measurement Model in Partial Least Square Structural Equation Modeling (Pls-Sem). International Journal of Mathematics, 2, 33-49. |

| [94] | Sun, S., B. W. Green, R. Bleck, S. G. Benjamin, & G. A. Grell, (2018) Subseasonal forecasting with an icosahedral, vertically quasi-Lagrangian coupled model. Part II: Probabilistic and deterministic forecast skill. Mon. Weather Rev., 146, no. 5, 1619-1639, |

| [95] | Cheah, C. S. L., Wang, C., Ren, H., Zong, X., Hyun Su Cho, H. S. & Xue, X. (2020). COVID-19 Racism and Mental Health in Chinese American Families. PubMed, National Library of Medicine. |

| [96] |

Huang, Y. T. (2021). Causal mediation of Semi-competing Risks. Biometric Methodology. Biometrics - Journal of International Biometric Society.

https://doi.org/10.1111/biom.13518 77, 4, (1170-1174). |

| [97] | Newman, W., Mwandambira, N., Charity, M., & Ongayi, W. (2018). Literature review on the impact of tax knowledge on tax compliance among small medium enterprises in a developing country. Journal of Legal, Ethical and Regulatory Issues, 22(4), 4675. |

APA Style

Zubairu, I., Atiawin, P. A., Iddrisu, A. J. (2025). Examining How Digitalization Affects Tax Compliance in Ghana Using Structural Equation Modelling (SEM). International Journal of Business and Economics Research, 14(1), 1-25. https://doi.org/10.11648/j.ijber.20251401.11

ACS Style

Zubairu, I.; Atiawin, P. A.; Iddrisu, A. J. Examining How Digitalization Affects Tax Compliance in Ghana Using Structural Equation Modelling (SEM). Int. J. Bus. Econ. Res. 2025, 14(1), 1-25. doi: 10.11648/j.ijber.20251401.11

AMA Style

Zubairu I, Atiawin PA, Iddrisu AJ. Examining How Digitalization Affects Tax Compliance in Ghana Using Structural Equation Modelling (SEM). Int J Bus Econ Res. 2025;14(1):1-25. doi: 10.11648/j.ijber.20251401.11

@article{10.11648/j.ijber.20251401.11,

author = {Ibrahim Zubairu and Patrick Akeba Atiawin and Ahmed Jamal Iddrisu},

title = {Examining How Digitalization Affects Tax Compliance in Ghana Using Structural Equation Modelling (SEM)

},

journal = {International Journal of Business and Economics Research},

volume = {14},

number = {1},

pages = {1-25},

doi = {10.11648/j.ijber.20251401.11},

url = {https://doi.org/10.11648/j.ijber.20251401.11},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ijber.20251401.11},

abstract = {This research study delved into the multifaceted realm of tax compliance within the digital economy context, with a specific focus on the impact of digitalization, the role of taxpayer education programs, and the importance of taxpayer awareness programs. A diverse sample of 278 participants, encompassing individuals engaged in various digital businesses and taxpayers in Ghana, provided valuable insights through structured questionnaires. This study examined the complex area of tax compliance in the context of the digital economy, paying particular attention to the effects of digitalization, the function of taxpayer education initiatives, and the significance of taxpayer awareness campaigns. Through the use of structured questionnaires, a varied sample of 278 participants; including taxpayers in Ghana and those involved in a range of digital businesses, providing insightful answers. The study produced important results by using a robust Structural Equation Modelling (SEM) technique. It was discovered that digitization has a favourable impact on tax compliance, highlighting its capacity to act as a stimulant for improved compliance practices. Additionally, initiatives to raise taxpayer knowledge and education have become essential in encouraging tax compliance in the digital economy. The significance of thorough tax education programs and awareness efforts is shown by these findings. As a result, this study encourages stakeholders to take the initiative and makes suggestions for managers, legislators, academics, and business leaders to use digitalization's revolutionary potential to promote tax compliance. Future scholars are encouraged by this work to go deeper into this dynamic field in order to better understand how the digital economy affects taxation and compliance.

},

year = {2025}

}

TY - JOUR T1 - Examining How Digitalization Affects Tax Compliance in Ghana Using Structural Equation Modelling (SEM) AU - Ibrahim Zubairu AU - Patrick Akeba Atiawin AU - Ahmed Jamal Iddrisu Y1 - 2025/02/05 PY - 2025 N1 - https://doi.org/10.11648/j.ijber.20251401.11 DO - 10.11648/j.ijber.20251401.11 T2 - International Journal of Business and Economics Research JF - International Journal of Business and Economics Research JO - International Journal of Business and Economics Research SP - 1 EP - 25 PB - Science Publishing Group SN - 2328-756X UR - https://doi.org/10.11648/j.ijber.20251401.11 AB - This research study delved into the multifaceted realm of tax compliance within the digital economy context, with a specific focus on the impact of digitalization, the role of taxpayer education programs, and the importance of taxpayer awareness programs. A diverse sample of 278 participants, encompassing individuals engaged in various digital businesses and taxpayers in Ghana, provided valuable insights through structured questionnaires. This study examined the complex area of tax compliance in the context of the digital economy, paying particular attention to the effects of digitalization, the function of taxpayer education initiatives, and the significance of taxpayer awareness campaigns. Through the use of structured questionnaires, a varied sample of 278 participants; including taxpayers in Ghana and those involved in a range of digital businesses, providing insightful answers. The study produced important results by using a robust Structural Equation Modelling (SEM) technique. It was discovered that digitization has a favourable impact on tax compliance, highlighting its capacity to act as a stimulant for improved compliance practices. Additionally, initiatives to raise taxpayer knowledge and education have become essential in encouraging tax compliance in the digital economy. The significance of thorough tax education programs and awareness efforts is shown by these findings. As a result, this study encourages stakeholders to take the initiative and makes suggestions for managers, legislators, academics, and business leaders to use digitalization's revolutionary potential to promote tax compliance. Future scholars are encouraged by this work to go deeper into this dynamic field in order to better understand how the digital economy affects taxation and compliance. VL - 14 IS - 1 ER -

Department of Accounting and Finance, Accra Technical University, Accra, Ghana

Centre for Global Economic Research, Accra, Ghana

Department of Banking and Finance, University of Professional Studies (UPSA), Accra, Ghana

Information