Abstract

This study investigates the mediating role of the culture of resource utilization in the relationship between financial literacy and the viability of micro and small enterprises in Ethiopia the case of hawasa city. The research was motivated by persistent challenges in micro and small enterprises sustainability, often linked to poor financial management and inefficient resource use, despite numerous policy supports. The purpose of this study is to examine how financial literacy influences micro and small enterprises viability both directly and indirectly through cultural practices related to resource utilization concurrent explanatory research design was employed, utilizing Structural Equation Modeling for analysis. The study began with Exploratory Factor Analysis to identify valid constructs and followed with Confirmatory Factor Analysis to test the hypothesized model. Data were collected through surveys and supported by qualitative insights from focus group discussions and key informant interviews. Initial model testing showed poor fit, prompting modifications. The revised model exhibited strong goodness-of-fit indicators (CMIN/DF = 1.85, RMSEA = 0.045, CFI = 0.97), validating the proposed relationships. Findings revealed that financial literacy has a significant positive direct effect on MSE viability (β = 1.369, p < 0.001) and also influences it indirectly through culture of resource utilization (indirect effect = 13.88). The total effect (15.249) indicates a partial mediation, highlighting the critical role of culture in enhancing the impact of financial knowledge. The study concludes that while financial literacy is vital, its full benefit is realized when coupled with efficient resource management culture. It recommends integrating financial literacy training with behavioral and cultural change programs targeting resource use norms in micro and small enterprises Owners.

Keywords

Financial Literacy, Resource Utilization Culture, Enterprise Viability, Structural Equation Modeling

1. Background of the Study

Financial literacy, defined as "the ability to process economic information and make informed decisions about financial planning wealth accumulation, debt, and pensions"

| [1] | Agarwalla, S. K., Barua, S. K., Jacob, J., & Varma, J. R. (2013). Financial literacy among working young in urban India. Indian Institute of Management Ahmedabad. |

| [2] | Anane, G. K., Cobblah, C., & Afari, E. O. (2023). Financial literacy and its determinants: Evidence from micro and small enterprises in Ghana. Cogent Economics & Finance, 11(1), 2175482. |

| [3] | Ardic, O. P., Heimann, M., & Mylenko, N. (2011). Access to financial services and the financial inclusion agenda around the world: A cross-country analysis with a new data set. The World Bank. |

| [20] | Huang, J., Nam, Y., & Sherraden, M. (2013). Financial knowledge and child development account participation. Journal of Consumer Affairs, 47(3), 481-503. |

| [22] | Jariwala, H. V. (2013). To study the level of financial literacy and its impact on investment decision – An in-depth analysis of investors in Gujarat state. Journal of Arts, Science & Commerce, 4(1), 27-36. |

| [30] | Lusardi, A., & Mitchell, O. S. (2014). The economic importance of financial literacy: Theory and evidence. Journal of Economic Literature, 52(1), 5-44. |

| [46] | van Rooij, M., Lusardi, A., & Alessie, R. (2009). Financial literacy and stock market participation. Journal of Financial Economics, 101(2), 449-472. |

| [50] | Yu, K. M., Wu, A. M., Chan, W. S., & Chou, K. L. (2015). Gender differences in financial literacy among Hong Kong workers. Educational Gerontology, 41(4), 279-292. |

[1-3, 20, 22, 30, 46, 50]

. Adequate financial literacy enables entrepreneurs to make well-informed decisions regarding budgeting, saving, investing, credit use, and long-term financial planning

| [1] | Agarwalla, S. K., Barua, S. K., Jacob, J., & Varma, J. R. (2013). Financial literacy among working young in urban India. Indian Institute of Management Ahmedabad. |

| [5] | Atkinson, A., & Messy, F.-A. (2012). Measuring financial literacy: Results of the OECD / International Network on Financial Education (INFE) pilot study. OECD Publishing. |

| [20] | Huang, J., Nam, Y., & Sherraden, M. (2013). Financial knowledge and child development account participation. Journal of Consumer Affairs, 47(3), 481-503. |

| [28] | Lusardi, A., & Mitchell, O. S. (2006). Financial literacy and planning: Implications for retirement wellbeing. National Bureau of Economic Research Working Paper No. 17078. |

| [29] | Lusardi, A., & Mitchell, O. S. (2011). Financial literacy and planning: Implications for retirement wellbeing. In A. Lusardi & O. S. Mitchell (Eds.), Financial literacy: Implications for retirement security and the financial marketplace (pp. 17-39). Oxford University Press. |

[1, 5, 20, 28, 29]

, all of which are essential for business survival and growth. Despite its importance, studies suggest that many SME owners in developing economies exhibit low levels of financial literacy, which impairs their decision-making capabilities

| [4] | Atkinson, A., & Messy, F.-A. (2011). Assessing financial literacy in 12 countries: An OECD/INFE international pilot exercise. Journal of Pension Economics & Finance, 10(4), 657-665. |

| [22] | Jariwala, H. V. (2013). To study the level of financial literacy and its impact on investment decision – An in-depth analysis of investors in Gujarat state. Journal of Arts, Science & Commerce, 4(1), 27-36. |

| [25] | Klapper, L., Lusardi, A., & Panos, G. A. (2012). Financial literacy and the financial crisis. National Bureau of Economic Research Working Paper No. 17930. |

[4, 22, 25]

.

The ability to manage personal finances has become increasingly important in today's world. The global marketplace is increasingly risky and can be unpredictable

| [9] | Bucher-Koenen, T., Lusardi, A., & Alessie, R. (2016). Financial literacy and retirement planning in Germany. In A. Lusardi (Ed.), Financial literacy: Implications for retirement security and the financial marketplace (pp. 101-122). Oxford University Press. |

[9]

. It also affects the nations and the societies as negatively or positively and it is emerging as one of its main implications is the rising costs of goods and services and it pushes people able to make well-informed financial decisions

| [26] | Kumari, S. (2016). Financial literacy: A review. International Journal of Applied Research, 2(4), 663-666. |

| [27] | Lusardi, A. (2011). Americans' financial capability. National Bureau of Economic Research Working Paper No. 17103. |

[26, 27]

. The Ethiopian government has identified SMEs as key components of its industrialization and poverty reduction strategies

| [45] | United Nations Development Programme (UNDP). (2019). Ethiopia's private sector: A catalyst for sustainable development. UNDP Ethiopia. |

[45]

. Despite this recognition, SMEs in Ethiopia face unique challenges that impede their growth and sustainability. A significant issue is the "missing middle" phenomenon, where SMEs are too large for microfinance institutions but too small for commercial banks, resulting in limited access to appropriate financial services

| [49] | World Bank. (2015). Ethiopia: Micro, small and medium enterprise sector diagnostic. The World Bank Group. |

[49]

. Additionally, factors such as political instability, corruption, and inadequate infrastructure have been identified as critical barriers to SME development in Ethiopia

| [42] | Shitaye, A. (2022). Barriers to micro and small enterprises development in Ethiopia: A systematic review. Addis Ababa University. |

[42]

.

The concept of financial literacy, however, does not exist in isolation. Cultural norms, values, and belief systems broadly referred to as “culture” also shape financial behavior. Culture is the system of shared beliefs, values, customs, and behaviors that members of a society use to interact with their world and with each other

| [18] | Guiso, L., Sapienza, P., & Zingales, L. (2006). Does culture affect economic outcomes? Journal of Economic Perspectives, 20(2), 23-48. |

| [19] | Hofstede, G. (1980). Culture's consequences: International differences in work-related values. Sage Publications. |

[18, 19]

. It is passed down through generations and influences perspectives on wealth accumulation, debt, risk, and investment. Culture significantly affects trust levels, investment decisions, and financial market participation

| [18] | Guiso, L., Sapienza, P., & Zingales, L. (2006). Does culture affect economic outcomes? Journal of Economic Perspectives, 20(2), 23-48. |

[18]

. Similarly Individuals from cultures that value long-term orientation and financial prudence tend to exhibit higher financial literacy

| [30] | Lusardi, A., & Mitchell, O. S. (2014). The economic importance of financial literacy: Theory and evidence. Journal of Economic Literature, 52(1), 5-44. |

| [38] | Osili, U. O., & Paulson, A. L. (2008). Institutions and financial development: Evidence from international migrants in the United States. The Review of Economics and Statistics, 90(3), 498-517. |

[30, 38]

.

2. Statement of the Problem

Financial products and services have become increasingly diverse and complex over time

| [13] | Erokhin, V. (2017). Financial literacy and its impact on market participation of small farmers in developing countries. Journal of International Business and Economics, 5(1), 35-44. |

| [17] | Fagbemi, F., & Ajibike, B. (2024). Financial inclusion, financial literacy, and small business performance in Nigeria. Journal of African Business, 25(1), 78-96. |

| [35] | Ning, G., Xu, Y., & Liu, Z. (2018). Financial literacy and household financial behavior: Evidence from China. Emerging Markets Finance and Trade, 54(13), 2981-3000. |

[13, 17, 35]

. Consumers and business owners face considerable difficulty in selecting suitable and beneficial financial products unless they possess adequate financial knowledge and capability

| [2] | Anane, G. K., Cobblah, C., & Afari, E. O. (2023). Financial literacy and its determinants: Evidence from micro and small enterprises in Ghana. Cogent Economics & Finance, 11(1), 2175482. |

| [11] | Cunliffe, J. (2017). Financial literacy and consumer choice. Palgrave Macmillan. |

| [44] | Sun, T., & Cao, J. (2011). Consumer financial literacy and its impact on consumer financial behavior. Journal of Consumer Affairs, 45(2), 275-293. |

[2, 11, 44]

.

Despite the negative consequences of financial illiteracy on individual financial well-being and overall economic performance

| [3] | Ardic, O. P., Heimann, M., & Mylenko, N. (2011). Access to financial services and the financial inclusion agenda around the world: A cross-country analysis with a new data set. The World Bank. |

| [7] | Beck, T., Demirgüç-Kunt, A., & Martinez Peria, M. S. (2008). Banking services for everyone? Barriers to bank access and use around the world. The World Bank Economic Review, 22(3), 397-430. |

| [10] | Claessens, S. (2006). Access to financial services: A review of the issues and public policy objectives. The World Bank Research Observer, 21(2), 207-240. |

[3, 7, 10]

, limited efforts have been made to comprehensively assess the financial literacy level of the Ethiopian population

| [6] | Baleseng, G. (2015). The state of financial literacy in Botswana. Bank of Botswana Research Bulletin. |

| [14] | Ethiopian Economic Association (EEA). (2015). Report on the Ethiopian economy 2014/15. Ethiopian Economic Association. |

| [15] | Ethiopia’s Micro and Small Enterprises Development (MSED) Policy & Strategy. (2016). Micro and Small Enterprises Development Policy and Strategy. Federal Democratic Republic of Ethiopia. |

| [16] | Ethiopia’s Micro and Small Enterprises Development (MSED) Strategy. (2011). Micro and Small Enterprises Development Strategy. Federal Democratic Republic of Ethiopia. |

| [40] | Rahel, M. (2018). The role of micro and small enterprises in the economic development of Ethiopia: The case of Addis Ababa [Unpublished doctoral dissertation]. Addis Ababa University. |

[6, 14-16, 40]

. Although one study assessed financial literacy among urban residents in Addis Ababa

| [23] | Kebede, S., & Kaur, P. (2017). Financial literacy and its determinants: The case of urban dwellers in Addis Ababa, Ethiopia. Paper presented at the 14th International Conference on Business Excellence. |

[23]

, its focus was geographically limited. Business operators in general and micro and small enterprise (MSE) owners in particular have received limited scholarly attention regarding financial literacy, despite their central role in economic development

| [15] | Ethiopia’s Micro and Small Enterprises Development (MSED) Policy & Strategy. (2016). Micro and Small Enterprises Development Policy and Strategy. Federal Democratic Republic of Ethiopia. |

| [34] | Meressa, H. A. (2020). Growth of micro and small scale enterprises and its driving factors: Empirical evidence from entrepreneurs in Hawassa city, Ethiopia. Journal of Innovation and Entrepreneurship, 9(1), 1-22. |

[15, 34]

.

3. Research Objectives

3.1. General Objective

To investigate the effect of financial literacy on the viability of Micro and Small Enterprises (MSEs) in Hawassa City, with specific focus on the mediating role of community culture in financial resource utilization.

3.2. Specific Objectives

1) To assess the financial literacy levels of MSE owners in study area.

2) To examine the relationship between financial literacy and the viability of MSEs.

3) To evaluate the mediating role of community culture in the relationship between financial literacy and the viability of micro and small enterprises.

4. Research Hypotheses

Based on the existing literatures the researchers developed the following testable hypothesis.

Ha1: Financial literacy has a positive and significant effect on the viability of MSEs.

Ha2: Community culture of resource utilization has significant positive effect on financial literacy level of MSEs.

Ha3: Community culture mediates the relationship between financial literacy and the viability of MSEs.

5. Conceptual Literature Review

The concept of literacy has evolved beyond the traditional notion of reading and writing and now reflects mastery or competence in a specific domain. Financial literacy therefore does not imply formal education in finance but rather the ability to effectively manage financial resources

| [43] | Spang, L. (2015). The definition of literacy. Reading Today, 32(4), 22-23. |

[43]

.

Financial literacy has been defined in multiple ways. Some scholars conceptualize it in terms of financial knowledge and awareness

| [5] | Atkinson, A., & Messy, F.-A. (2012). Measuring financial literacy: Results of the OECD / International Network on Financial Education (INFE) pilot study. OECD Publishing. |

| [8] | Bucher-Koenen, T., Lusardi, A., Alessie, R., & Van Rooij, M. (2017). How financially literate are women? An overview and new insights. Journal of Consumer Affairs, 51(2), 255-283. |

[5, 8]

, others emphasize the ability to apply financial knowledge

| [39] | Potrich, A. C. G., Vieira, K. M., & Kirch, G. (2015). Determinants of financial literacy: Analysis of the influence of socioeconomic and demographic variables. Revista Contabilidade & Finanças, 26(69), 362-377. |

[39]

, while additional perspectives incorporate financial knowledge, behavior, and attitudes

| [21] | International Network on Financial Education (INFE). (2011). Measuring financial literacy: Core questionnaire in measuring financial literacy: OECD/INFE pilot study. OECD. |

[21]

. Financial literacy extends beyond basic financial knowledge and includes the competence and confidence to make responsible financial decisions

| [39] | Potrich, A. C. G., Vieira, K. M., & Kirch, G. (2015). Determinants of financial literacy: Analysis of the influence of socioeconomic and demographic variables. Revista Contabilidade & Finanças, 26(69), 362-377. |

| [41] | Remund, D. L. (2010). Financial literacy explicated: The case for a clearer definition in an increasingly complex economy. Journal of Consumer Affairs, 44(2), 276-295. |

[39, 41]

.

Financial literacy definitions are commonly grouped into four categories: knowledge of financial concepts, ability to manage finances, skill in financial decision-making, and confidence in future financial planning

| [24] | Kimiyaghalam, F., & Safari, M. (2015). Review papers on definition of financial literacy and its measurement. International Journal of Management, Accounting and Economics, 2(6), 545-554. |

[24]

. A widely accepted definition describes financial literacy as a combination of knowledge, attitudes, and behaviors required to make sound financial decisions and achieve individual financial well-being

| [37] | Organisation for Economic Co-operation and Development (OECD). (2018). OECD/INFE toolkit for measuring financial literacy and financial inclusion. OECD Publishing. |

[37]

. This definition highlights financial knowledge, financial behavior, and financial attitude as the three core dimensions of financial literacy, a framework widely adopted in empirical research

| [5] | Atkinson, A., & Messy, F.-A. (2012). Measuring financial literacy: Results of the OECD / International Network on Financial Education (INFE) pilot study. OECD Publishing. |

[5]

.

5.1. Viability of MSEs

The viability of Micro and Small Enterprises refers to their ability to sustain operations and withstand routine business challenges

| [31] | Mamush Tirfe, M. (2022). Determinants of micro and small enterprises viability: The case of Nekemte Town. Journal of Innovation and Entrepreneurship, 11(1), 1-19. |

[31]

. Viability includes covering operating costs, maintaining stable income, and adapting to changes in the business environment

| [47] | Woldie, A., & Aderssa, T. (2021). The viability of micro and small enterprises in Ethiopia: A case study of Adama City. Journal of Small Business and Enterprise Development, 28(5), 745-763. |

[47]

. MSE survival depends on balancing revenues and expenses while responding effectively to market conditions, competition, and customer needs. Long-term viability also requires adaptability, innovation, and resilience to economic and technological changes.

5.2. Community Culture of Resource Utilization and Financial Literacy

Empirical studies directly examining the mediating role of community culture between financial literacy and MSE viability in Ethiopia are limited. However, available evidence suggests that cultural norms strongly influence financial behavior and business outcomes.

A study conducted among MSE operators in Hawassa City and Dale Woreda revealed that financial literacy levels were below average, with cultural practices such as communal celebrations contributing to unplanned expenditures and financial instability

| [12] | Engida, B. (2022). Assessment of financial literacy of micro and small enterprise operators: The case of Hawassa City and Dale Woreda, Sidama Region [Unpublished master's thesis]. Hawassa University. |

[12]

. Another study examining MSE challenges in Hawassa City identified financial constraints and acknowledged the indirect influence of cultural norms on financial decisions and business practices

| [32] | Mathewos Yure, & Kanbiro Orkaido Deyganto. (2024). Challenges and opportunities of micro and small enterprises in Hawassa City, Ethiopia. International Journal of Small and Medium Enterprises, 7(1), 1-18. |

[32]

. These findings suggest that community culture can mediate the effect of financial literacy on MSE viability.

5.3. Financial Literacy and MSE Viability

Global evidence shows that financial literacy significantly improves MSE performance by enhancing cash-flow management, reducing insolvency risk, and supporting business growth

| [30] | Lusardi, A., & Mitchell, O. S. (2014). The economic importance of financial literacy: Theory and evidence. Journal of Economic Literature, 52(1), 5-44. |

[30]

. Studies in Sub-Saharan Africa similarly demonstrate that financial literacy is positively associated with business performance, access to finance, and working-capital management

| [33] | Mensah, E., Asante, G. N., & Osei, K. A. (2021). Financial literacy and small business success in Sub-Saharan Africa: Evidence from Ghana, South Africa, and Uganda. Journal of African Business, 22(4), 512-530. |

| [36] | Ogbuji, C. N., Uche, D. B., & Olamide, K. (2019). Financial literacy and business performance of MSEs in Sub-Saharan Africa: A study of Nigeria and Kenya. Journal of Entrepreneurship in Emerging Economies, 11(3), 342-358. |

[33, 36]

. Ethiopian studies also confirm that financially literate MSE owners demonstrate stronger financial control, better investment decisions, and higher enterprise sustainability

| [48] | Wondimu, G., & Teshome, E. (2020). The impact of financial literacy on MSE performance in Ethiopia: A case study of Addis Ababa. Ethiopian Journal of Business and Economics, 10(2), 155-176. |

[48]

.

The study confirms that financial literacy positively affects MSE viability both directly and indirectly through community culture of resource utilization. The mediation analysis indicates partial mediation, with cultural norms significantly amplifying the impact of financial literacy on enterprise viability. These findings highlight the importance of integrating culturally sensitive financial literacy programs into MSE development strategies in Ethiopia.

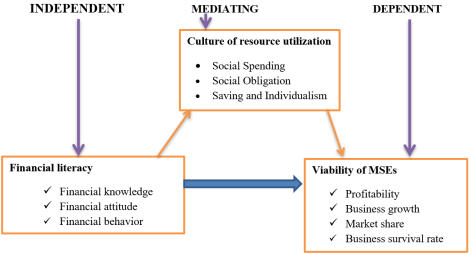

6. Conceptual Framework

For this study, the conceptual framework is developed from the pieces of literature reviewed, and the researchers own conceptualization. The independent variable financial literacy, Mediating variable community financial resource utilization and dependent variable Viability of MSEs. This relationship between the factors is illustrated below in

Figure 1. Below.

Figure 1. Conceptual framework of study.

7. Research Design and Approach

The study employed both concurrent explanatory research designs to explain the relationship between variables understudy therefore, the study employed mixed research approach where both quantitative and qualitative data are collected simultaneously, but the qualitative data collection is specifically aimed at explaining or interpreting the quantitative findings. According to Kothari (2004), there are three research approaches these are; quantitative approaches, qualitative approaches, and mixed of both approaches. This study employed mixed research approach (quantitative and qualitative research approaches). Hence, the research questions and objectives were addressed by cross-sectional survey data since the study was conducted at one point in time and place.

8. Types and Sources of Data

8.1. Data Type

To come up with a clear conclusion about the aforementioned objectives, the researcher employed both quantitative and qualitative data types. While employing quantitative data, the researcher’s rationale is basically to achieve all specific objectives; whereas qualitative data types was used while stating and narrating about the objectives of the study to triangulate the quantitative findings with qualitative opinions. Hence, objectives addressed by quantitative means were also addressed qualitatively, a condition that emphasizes the relevance of employing qualitative and quantitative data types; that in turn is imperative for making the study more accurate and reliable.

8.2. Data Sources

To address the specific objectives of the study data were gathered from both primary and secondary sources. Primary source of data was collected from sample MSE owners, Sub-city Enterprise office experts, and the employee of MSEs. Secondary data, to supplement primary data, were obtained from published and unpublished documents including journals, city administration, and regional enterprises development offices in the area related to the thesis objectives.

8.3. Methods of Data Collection

For data collection, the study employed a structured questionnaire and focus group discussions (FGDs). The questionnaire consisted of Likert-scale items with five response categories ranging from Strongly Disagree to Strongly Agree. The questionnaire was initially prepared in English and subsequently translated into Sidamu Afoo to ensure clarity and ease of understanding for respondents.

The questionnaire items were adapted from established financial literacy measurement instruments developed in prior studies

| [5] | Atkinson, A., & Messy, F.-A. (2012). Measuring financial literacy: Results of the OECD / International Network on Financial Education (INFE) pilot study. OECD Publishing. |

| [21] | International Network on Financial Education (INFE). (2011). Measuring financial literacy: Core questionnaire in measuring financial literacy: OECD/INFE pilot study. OECD. |

| [39] | Potrich, A. C. G., Vieira, K. M., & Kirch, G. (2015). Determinants of financial literacy: Analysis of the influence of socioeconomic and demographic variables. Revista Contabilidade & Finanças, 26(69), 362-377. |

| [37] | Organisation for Economic Co-operation and Development (OECD). (2018). OECD/INFE toolkit for measuring financial literacy and financial inclusion. OECD Publishing. |

[5, 21, 39, 37]

. In addition, context-specific questions relevant to the Ethiopian micro and small enterprise environment were incorporated to enhance contextual validity.

Furthermore, two focus group discussions were conducted, each representing one stratum, with a total of eight participants. Efforts were made to ensure diversity in gender, age, and educational background among participants. The FGDs were used to complement quantitative findings and provide deeper insights into cultural and behavioral aspects influencing financial resource utilization.

9. Result and Discussion

9.1. Data Cleaning and Editing

Before analysis, data collected from selected respondents was edited, coded, and entered into SPSS version 27 and Microsoft excel 2010. Totally 191 questionnaires containing six pages have been distributed to the selected respondents and a Maximum effort has been placed to collect back correctly filled questionnaires.

The respondents are requested to fill out the entire questions of the questionnaires and give them back within a week. The presence of the cell phone address of the researcher on the questionnaire helps the respondents to ask any unclear questions to make it brief in case of miss understanding. Before handing them the questionnaire, respondents were kindly, requested if they have some time to fill the questionnaire responsibly. However, all the respondents were willing to fill out the questionnaire and agreed to participate in this research. Accordingly, there were no Non-response rate has been recorded.

Generally, all questionnaires were returned properly and none of the respondents failed to return the questionnaire. The collected questionnaires from the respondents were, filled following the instructions specified on the top of the questions, therefore; the entire sections of the questionnaires were filled properly there is no incomplete, missing, or selecting multiple answers among the given alternatives.

Descriptive Statics of Financial Literacy

Generally, the finding of the study revealed that study indicates that MSE owners in hawasa city administration possess a moderate to good level of financial literacy, with positive financial attitudes and knowledge. However, there is a need to enhance financial behaviors to further improve their financial management practices. These findings underscore the importance of targeted financial literacy programs to support MSE owners in developing comprehensive financial skills.

Table 1. Descriptive statics of financial literacy.

Descriptive Statistics |

| N | Minimum | Maximum | Mean | Std. Deviation |

FAT | 191 | 2.40 | 4.20 | 3.5173 | .59335 |

FBH | 191 | 2.77 | 3.62 | 3.1301 | .27184 |

FKNO | 191 | 2.44 | 4.33 | 3.1990 | .62759 |

Valid N (listwise) | 191 | | | | |

Source own survey 2025

Regression Weights: (Group number 1 - Default model)

Table 2. Regression Weights.

VARIABLES | Estimate | S. E. | C. R. | P | Label |

CRUTI | <--- | FLIT | 4.618 | 1.923 | 2.4 | *** | par_8 |

VIAB | <--- | CRUTI | 3.006 | 1.03 | 1.018 | *** | par_9 |

VIAB | <--- | FLIT | 1.369 | 0.416 | 3.292 | *** | par_10 |

FAT | <--- | FLIT | 1 | | | | |

FKNO | <--- | FLIT | 3.548 | 0.961 | 3.692 | *** | par_1 |

FB2 | <--- | FLIT | 1.914 | 0.47 | 4.073 | *** | par_2 |

CSV | <--- | CRUTI | 1 | | | | |

CPP | <--- | CRUTI | 0.981 | 0.098 | 10.01 | *** | par_3 |

TPRO | <--- | VIAB | 0.84 | | | | |

SURV | <--- | VIAB | 0.797 | 0.008 | 99.63 | *** | par_4 |

BGRO | <--- | VIAB | 0.991 | 0.131 | 7.57 | *** | par_5 |

MSHA | <--- | VIAB | 0.873 | 0.16 | 2.56 | *** | par_6 |

CCOL | <--- | CRUTI | 0.402 | 0.051 | 7.861 | *** | par_7 |

Source Own survey, 2025

As it is indicated in the regression weight of each variable loading we can realize the model supports a hierarchical influence where financial literacy influences culture of resource utilization and Micro and small enterprise viability directly further influences Micro and small enterprise viability and several other variables, suggesting it acts as a mediator. Micro and small enterprise viability then influences outcome variables, indicating its role as a key predictor of downstream effects. The significance and magnitude of estimates suggest the model fits the data well and the paths are meaningful.

Summary of Good ness of fit test

Table 3. Summary of Good ness of fit test.

Fit Index | Fit Value | Interpretation |

CMIN/DF | 1.85 | Good fit |

CFI | 0.97 | Excellent fit |

AGFI | 0.92 | Good fit |

GFI | 0.93 | Good fit |

NFI | 0.95 | Good fit |

RMSEA | 0.045 | Excellent fit |

Source Own survey, 2025

The fit indices collectively indicate that the model has a strong fit to the data, supporting the theory that financial literacy positively affects the viability of micro and small enterprises, both directly and indirectly through the culture of resource utilization. This implies the result support the theoretical framework provided as Financial Literacy (FLIT): Posited as a key driver enabling entrepreneurs to make informed financial decisions, improving enterprise viability. Culture of Resource Utilization (CRUTI): Acts as a mediator, reflecting how efficiently resources are managed and utilized, which is critical in small enterprises. Viability (VIAB): The outcome variable representing the sustainability and success of micro and small enterprises. The model’s strong fit supports the mediated relationship where financial literacy enhances resource utilization culture, which in turn improves enterprise viability. This aligns with prior research emphasizing the role of both knowledge and organizational culture in business success. The model captures both direct and indirect effects of financial literacy on viability of micro and small enterprises.

Direct effect= 1.369, Indirect effect = γ1×β1=4.618×3.006=13.88 Total effect = Direct effect + Indirect effect = 1.369+13.88 =15.249

9.2. Mathematical Model of Equation

VIAB=β+1.369*FLIT+3.006(4.618FLIT)+e

VIAB=β+(1.369+13.88)FLIT+e=β+15.249FLIT+e

The large indirect effect compared to the direct effect suggests that the mediator (CRUTI) plays a substantial role in explaining the influence of financial literacy on viability. The direct path from FLIT to VIAB is significant (estimate = 1.369, p < 0.001), the indirect path through CRUTI is also significant because FLIT significantly predicts CRUTI (4.618, p < 0.001), CRUTI significantly predicts VIAB (3.006, p < 0.001).

Therefore, the model shows there is partial Mediation because the independent variable financial literacy affects the dependent variable micro and small enterprises viability through the mediator culture of resource utilization and the direct path from financial literacy to micro and small enterprises viability.

Participants of focus group discussion and key informants supports the mediation role of financial resource utilization trend of micro and small enterprises in between financial literacy and viability of micro and small enterprises as the culture of community wich gives faour to accept and manage gusts in unplanned manner and the members of community has culture of accommodating all costs at the expense of MSEs owner or other person of guests destination was the major issue of mismanagement of business enterprise.

9.3. Hypothesis Test

Based on the structural equation modeling results presented above, the result of hypothesis test was explained as follows.

Hypothesis 1: Financial literacy has a positive and significant effect on the viability of MSEs.

The direct path from Financial Literacy (FLIT) to Viability (VIAB) shows a statistically significant positive effect (estimate = 1.369, p < 0.001). This indicates that higher levels of financial literacy among MSE owners are associated with improved business viability. The positive coefficient confirms that financial literacy directly contributes to better business outcomes.

MSE owners with higher financial literacy demonstrate stronger capabilities in financial decision-making, risk management, and implementation of effective financial strategies. These competencies translate into improved performance indicators such as profitability, sustainability, market share, and survival rates. This finding is consistent with previous empirical evidence indicating that financial literacy positively influences business performance

| [30] | Lusardi, A., & Mitchell, O. S. (2014). The economic importance of financial literacy: Theory and evidence. Journal of Economic Literature, 52(1), 5-44. |

[30]

. Supported.

Hypothesis 2: Community culture of resource utilization has significant positive effect on financial literacy level of MSEs.

The path from Financial Literacy (FLIT) to Culture of Resource Utilization (CRUTI) reveals a significant positive relationship (estimate = 4.618, p < 0.001). This result indicates that financial literacy significantly predicts and influences the culture of resource utilization within micro and small enterprises.

MSE owners with higher financial literacy are more likely to cultivate positive resource utilization practices in their businesses. Financial knowledge shapes attitudes and behaviors related to budgeting, cost control, and efficient allocation of resources, thereby fostering organizational cultures that emphasize efficiency and sustainability. Hypothesis was supported.

Hypothesis 3: Community culture mediates the relationship between financial literacy and the viability of MSEs.

The analysis reveals a significant mediation effect with the following parameters:

Direct effect of FLIT on VIAB = 1.369 (p < 0.001)

Indirect effect through CRUTI = 13.88 (calculated as 4.618 × 3.006)

Total effect = 15.249 (1.369 + 13.88) Result: Supported (Partial Mediation)

The mediation is classified as partial because both the direct path (FLIT → VIAB) and the indirect path through the mediator (FLIT → CRUTI → VIAB) are statistically significant.

The substantial indirect effect (13.88) compared to the direct effect (1.369) indicates that culture of resource utilization plays a crucial mediating role in translating financial literacy into business viability. This suggests that while financial knowledge directly improves business outcomes, its impact is significantly amplified when it leads to the development of positive resource utilization cultures. The finding supports the theoretical framework that cultural factors mediate how financial knowledge translates into business practices and ultimately affects enterprise viability.

The partial mediation nature of the relationship indicates that financial literacy affects business viability both directly through improved decision-making and indirectly by fostering efficient resource utilization cultures. This nuanced understanding highlights the importance of addressing both knowledge gaps and cultural factors when designing interventions to improve MSE performance.

These findings align with prior studies emphasizing the dual importance of financial knowledge and organizational culture in driving business success. For example, financial literacy has been shown to improve decision-making and financial management, which are crucial for small enterprise viability (Huston, 2010). Additionally, the role of resource management culture as a mediator is consistent with research highlighting how internal organizational processes and cultures influence firm performance (Barney, 1991).

10. Summary, Conclusion and Recommendations

This study examined the effect of financial literacy on the viability of Micro and Small Enterprises (MSEs) in Hawassa City, Ethiopia, with particular emphasis on the mediating role of community culture in financial resource utilization. Guided by clearly defined objectives and hypotheses, the findings provide several important insights.

The results indicate that the overall financial literacy level of MSE owners in Hawassa City is relatively low, particularly regarding fundamental concepts such as interest compounding, inflation, and risk diversification. Limited financial knowledge constrains owners’ ability to make informed financial decisions, thereby hindering enterprise growth and sustainability. This finding is consistent with evidence from developing-country contexts

| [30] | Lusardi, A., & Mitchell, O. S. (2014). The economic importance of financial literacy: Theory and evidence. Journal of Economic Literature, 52(1), 5-44. |

[30]

.

Structural equation modeling results confirmed a significant positive direct effect of financial literacy on MSE viability (estimate = 1.369, p < 0.001). Financially literate owners demonstrated stronger financial planning, risk management, and profitability, underscoring the importance of financial knowledge for enterprise sustainability.

Importantly, community culture of resource utilization was identified as a significant mediator. The indirect effect of financial literacy on viability through community culture was substantially larger than the direct effect, highlighting the crucial role cultural norms and values play in shaping how financial knowledge is applied in practice. These findings confirm partial mediation, indicating that financial literacy affects enterprise viability both directly and indirectly through culturally embedded resource utilization practices.

The study further revealed that younger, more educated, and male MSE owners tend to exhibit higher financial literacy levels. Education and prior business experience were positively associated with improved financial decision-making.

Based on these findings, the study recommends the design and implementation of culturally sensitive financial literacy programs, integration of financial education and cultural awareness into entrepreneurship training, and active involvement of community leaders in financial capability initiatives. Future research should extend to rural areas, explore specific cultural dimensions such as religious norms and gender roles, and examine the growing role of digital financial literacy in MSE development.

Overall, the findings emphasize the need for holistic interventions that simultaneously address financial knowledge and cultural context to promote sustainable growth and resilience among Micro and Small Enterprises in Ethiopia.

Abbreviations

CRUT | Culture of Resource Utilization |

MSE | Micro and Small Enterprise |

SEM | Structural Equation Modeling |

Author Contributions

Abel Tirfe: Conceptualization, Writing – original draft, Writing – review & editing, Software

Natnael Million: Writing – review & editing, Methodology, funding acquisition

Conflicts of Interest

There is no conflicts of interest.

References

| [1] |

Agarwalla, S. K., Barua, S. K., Jacob, J., & Varma, J. R. (2013). Financial literacy among working young in urban India. Indian Institute of Management Ahmedabad.

|

| [2] |

Anane, G. K., Cobblah, C., & Afari, E. O. (2023). Financial literacy and its determinants: Evidence from micro and small enterprises in Ghana. Cogent Economics & Finance, 11(1), 2175482.

|

| [3] |

Ardic, O. P., Heimann, M., & Mylenko, N. (2011). Access to financial services and the financial inclusion agenda around the world: A cross-country analysis with a new data set. The World Bank.

|

| [4] |

Atkinson, A., & Messy, F.-A. (2011). Assessing financial literacy in 12 countries: An OECD/INFE international pilot exercise. Journal of Pension Economics & Finance, 10(4), 657-665.

|

| [5] |

Atkinson, A., & Messy, F.-A. (2012). Measuring financial literacy: Results of the OECD / International Network on Financial Education (INFE) pilot study. OECD Publishing.

|

| [6] |

Baleseng, G. (2015). The state of financial literacy in Botswana. Bank of Botswana Research Bulletin.

|

| [7] |

Beck, T., Demirgüç-Kunt, A., & Martinez Peria, M. S. (2008). Banking services for everyone? Barriers to bank access and use around the world. The World Bank Economic Review, 22(3), 397-430.

|

| [8] |

Bucher-Koenen, T., Lusardi, A., Alessie, R., & Van Rooij, M. (2017). How financially literate are women? An overview and new insights. Journal of Consumer Affairs, 51(2), 255-283.

|

| [9] |

Bucher-Koenen, T., Lusardi, A., & Alessie, R. (2016). Financial literacy and retirement planning in Germany. In A. Lusardi (Ed.), Financial literacy: Implications for retirement security and the financial marketplace (pp. 101-122). Oxford University Press.

|

| [10] |

Claessens, S. (2006). Access to financial services: A review of the issues and public policy objectives. The World Bank Research Observer, 21(2), 207-240.

|

| [11] |

Cunliffe, J. (2017). Financial literacy and consumer choice. Palgrave Macmillan.

|

| [12] |

Engida, B. (2022). Assessment of financial literacy of micro and small enterprise operators: The case of Hawassa City and Dale Woreda, Sidama Region [Unpublished master's thesis]. Hawassa University.

|

| [13] |

Erokhin, V. (2017). Financial literacy and its impact on market participation of small farmers in developing countries. Journal of International Business and Economics, 5(1), 35-44.

|

| [14] |

Ethiopian Economic Association (EEA). (2015). Report on the Ethiopian economy 2014/15. Ethiopian Economic Association.

|

| [15] |

Ethiopia’s Micro and Small Enterprises Development (MSED) Policy & Strategy. (2016). Micro and Small Enterprises Development Policy and Strategy. Federal Democratic Republic of Ethiopia.

|

| [16] |

Ethiopia’s Micro and Small Enterprises Development (MSED) Strategy. (2011). Micro and Small Enterprises Development Strategy. Federal Democratic Republic of Ethiopia.

|

| [17] |

Fagbemi, F., & Ajibike, B. (2024). Financial inclusion, financial literacy, and small business performance in Nigeria. Journal of African Business, 25(1), 78-96.

|

| [18] |

Guiso, L., Sapienza, P., & Zingales, L. (2006). Does culture affect economic outcomes? Journal of Economic Perspectives, 20(2), 23-48.

|

| [19] |

Hofstede, G. (1980). Culture's consequences: International differences in work-related values. Sage Publications.

|

| [20] |

Huang, J., Nam, Y., & Sherraden, M. (2013). Financial knowledge and child development account participation. Journal of Consumer Affairs, 47(3), 481-503.

|

| [21] |

International Network on Financial Education (INFE). (2011). Measuring financial literacy: Core questionnaire in measuring financial literacy: OECD/INFE pilot study. OECD.

|

| [22] |

Jariwala, H. V. (2013). To study the level of financial literacy and its impact on investment decision – An in-depth analysis of investors in Gujarat state. Journal of Arts, Science & Commerce, 4(1), 27-36.

|

| [23] |

Kebede, S., & Kaur, P. (2017). Financial literacy and its determinants: The case of urban dwellers in Addis Ababa, Ethiopia. Paper presented at the 14th International Conference on Business Excellence.

|

| [24] |

Kimiyaghalam, F., & Safari, M. (2015). Review papers on definition of financial literacy and its measurement. International Journal of Management, Accounting and Economics, 2(6), 545-554.

|

| [25] |

Klapper, L., Lusardi, A., & Panos, G. A. (2012). Financial literacy and the financial crisis. National Bureau of Economic Research Working Paper No. 17930.

|

| [26] |

Kumari, S. (2016). Financial literacy: A review. International Journal of Applied Research, 2(4), 663-666.

|

| [27] |

Lusardi, A. (2011). Americans' financial capability. National Bureau of Economic Research Working Paper No. 17103.

|

| [28] |

Lusardi, A., & Mitchell, O. S. (2006). Financial literacy and planning: Implications for retirement wellbeing. National Bureau of Economic Research Working Paper No. 17078.

|

| [29] |

Lusardi, A., & Mitchell, O. S. (2011). Financial literacy and planning: Implications for retirement wellbeing. In A. Lusardi & O. S. Mitchell (Eds.), Financial literacy: Implications for retirement security and the financial marketplace (pp. 17-39). Oxford University Press.

|

| [30] |

Lusardi, A., & Mitchell, O. S. (2014). The economic importance of financial literacy: Theory and evidence. Journal of Economic Literature, 52(1), 5-44.

|

| [31] |

Mamush Tirfe, M. (2022). Determinants of micro and small enterprises viability: The case of Nekemte Town. Journal of Innovation and Entrepreneurship, 11(1), 1-19.

|

| [32] |

Mathewos Yure, & Kanbiro Orkaido Deyganto. (2024). Challenges and opportunities of micro and small enterprises in Hawassa City, Ethiopia. International Journal of Small and Medium Enterprises, 7(1), 1-18.

|

| [33] |

Mensah, E., Asante, G. N., & Osei, K. A. (2021). Financial literacy and small business success in Sub-Saharan Africa: Evidence from Ghana, South Africa, and Uganda. Journal of African Business, 22(4), 512-530.

|

| [34] |

Meressa, H. A. (2020). Growth of micro and small scale enterprises and its driving factors: Empirical evidence from entrepreneurs in Hawassa city, Ethiopia. Journal of Innovation and Entrepreneurship, 9(1), 1-22.

|

| [35] |

Ning, G., Xu, Y., & Liu, Z. (2018). Financial literacy and household financial behavior: Evidence from China. Emerging Markets Finance and Trade, 54(13), 2981-3000.

|

| [36] |

Ogbuji, C. N., Uche, D. B., & Olamide, K. (2019). Financial literacy and business performance of MSEs in Sub-Saharan Africa: A study of Nigeria and Kenya. Journal of Entrepreneurship in Emerging Economies, 11(3), 342-358.

|

| [37] |

Organisation for Economic Co-operation and Development (OECD). (2018). OECD/INFE toolkit for measuring financial literacy and financial inclusion. OECD Publishing.

|

| [38] |

Osili, U. O., & Paulson, A. L. (2008). Institutions and financial development: Evidence from international migrants in the United States. The Review of Economics and Statistics, 90(3), 498-517.

|

| [39] |

Potrich, A. C. G., Vieira, K. M., & Kirch, G. (2015). Determinants of financial literacy: Analysis of the influence of socioeconomic and demographic variables. Revista Contabilidade & Finanças, 26(69), 362-377.

|

| [40] |

Rahel, M. (2018). The role of micro and small enterprises in the economic development of Ethiopia: The case of Addis Ababa [Unpublished doctoral dissertation]. Addis Ababa University.

|

| [41] |

Remund, D. L. (2010). Financial literacy explicated: The case for a clearer definition in an increasingly complex economy. Journal of Consumer Affairs, 44(2), 276-295.

|

| [42] |

Shitaye, A. (2022). Barriers to micro and small enterprises development in Ethiopia: A systematic review. Addis Ababa University.

|

| [43] |

Spang, L. (2015). The definition of literacy. Reading Today, 32(4), 22-23.

|

| [44] |

Sun, T., & Cao, J. (2011). Consumer financial literacy and its impact on consumer financial behavior. Journal of Consumer Affairs, 45(2), 275-293.

|

| [45] |

United Nations Development Programme (UNDP). (2019). Ethiopia's private sector: A catalyst for sustainable development. UNDP Ethiopia.

|

| [46] |

van Rooij, M., Lusardi, A., & Alessie, R. (2009). Financial literacy and stock market participation. Journal of Financial Economics, 101(2), 449-472.

|

| [47] |

Woldie, A., & Aderssa, T. (2021). The viability of micro and small enterprises in Ethiopia: A case study of Adama City. Journal of Small Business and Enterprise Development, 28(5), 745-763.

|

| [48] |

Wondimu, G., & Teshome, E. (2020). The impact of financial literacy on MSE performance in Ethiopia: A case study of Addis Ababa. Ethiopian Journal of Business and Economics, 10(2), 155-176.

|

| [49] |

World Bank. (2015). Ethiopia: Micro, small and medium enterprise sector diagnostic. The World Bank Group.

|

| [50] |

Yu, K. M., Wu, A. M., Chan, W. S., & Chou, K. L. (2015). Gender differences in financial literacy among Hong Kong workers. Educational Gerontology, 41(4), 279-292.

|

Cite This Article

-

APA Style

Tirfe, A., Million, N. (2026). The Effect of Financial Literacy on the Viability of Micro and Small Enterprises: The Mediating Role of Community Culture the Case of Hawassa City, Sidama, Ethiopia. International Journal of Accounting, Finance and Risk Management, 11(1), 80-88. https://doi.org/10.11648/j.ijafrm.20261101.15

Copy

|

Copy

|

Download

Download

ACS Style

Tirfe, A.; Million, N. The Effect of Financial Literacy on the Viability of Micro and Small Enterprises: The Mediating Role of Community Culture the Case of Hawassa City, Sidama, Ethiopia. Int. J. Account. Finance Risk Manag. 2026, 11(1), 80-88. doi: 10.11648/j.ijafrm.20261101.15

Copy

|

Download

AMA Style

Tirfe A, Million N. The Effect of Financial Literacy on the Viability of Micro and Small Enterprises: The Mediating Role of Community Culture the Case of Hawassa City, Sidama, Ethiopia. Int J Account Finance Risk Manag. 2026;11(1):80-88. doi: 10.11648/j.ijafrm.20261101.15

Copy

|

Download

-

@article{10.11648/j.ijafrm.20261101.15,

author = {Abel Tirfe and Natnael Million},

title = {The Effect of Financial Literacy on the Viability of Micro and Small Enterprises: The Mediating Role of Community Culture the Case of Hawassa City, Sidama, Ethiopia},

journal = {International Journal of Accounting, Finance and Risk Management},

volume = {11},

number = {1},

pages = {80-88},

doi = {10.11648/j.ijafrm.20261101.15},

url = {https://doi.org/10.11648/j.ijafrm.20261101.15},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ijafrm.20261101.15},

abstract = {This study investigates the mediating role of the culture of resource utilization in the relationship between financial literacy and the viability of micro and small enterprises in Ethiopia the case of hawasa city. The research was motivated by persistent challenges in micro and small enterprises sustainability, often linked to poor financial management and inefficient resource use, despite numerous policy supports. The purpose of this study is to examine how financial literacy influences micro and small enterprises viability both directly and indirectly through cultural practices related to resource utilization concurrent explanatory research design was employed, utilizing Structural Equation Modeling for analysis. The study began with Exploratory Factor Analysis to identify valid constructs and followed with Confirmatory Factor Analysis to test the hypothesized model. Data were collected through surveys and supported by qualitative insights from focus group discussions and key informant interviews. Initial model testing showed poor fit, prompting modifications. The revised model exhibited strong goodness-of-fit indicators (CMIN/DF = 1.85, RMSEA = 0.045, CFI = 0.97), validating the proposed relationships. Findings revealed that financial literacy has a significant positive direct effect on MSE viability (β = 1.369, p < 0.001) and also influences it indirectly through culture of resource utilization (indirect effect = 13.88). The total effect (15.249) indicates a partial mediation, highlighting the critical role of culture in enhancing the impact of financial knowledge. The study concludes that while financial literacy is vital, its full benefit is realized when coupled with efficient resource management culture. It recommends integrating financial literacy training with behavioral and cultural change programs targeting resource use norms in micro and small enterprises Owners.},

year = {2026}

}

Copy

|

Download

-

TY - JOUR

T1 - The Effect of Financial Literacy on the Viability of Micro and Small Enterprises: The Mediating Role of Community Culture the Case of Hawassa City, Sidama, Ethiopia

AU - Abel Tirfe

AU - Natnael Million

Y1 - 2026/03/26

PY - 2026

N1 - https://doi.org/10.11648/j.ijafrm.20261101.15

DO - 10.11648/j.ijafrm.20261101.15

T2 - International Journal of Accounting, Finance and Risk Management

JF - International Journal of Accounting, Finance and Risk Management

JO - International Journal of Accounting, Finance and Risk Management

SP - 80

EP - 88

PB - Science Publishing Group

SN - 2578-9376

UR - https://doi.org/10.11648/j.ijafrm.20261101.15

AB - This study investigates the mediating role of the culture of resource utilization in the relationship between financial literacy and the viability of micro and small enterprises in Ethiopia the case of hawasa city. The research was motivated by persistent challenges in micro and small enterprises sustainability, often linked to poor financial management and inefficient resource use, despite numerous policy supports. The purpose of this study is to examine how financial literacy influences micro and small enterprises viability both directly and indirectly through cultural practices related to resource utilization concurrent explanatory research design was employed, utilizing Structural Equation Modeling for analysis. The study began with Exploratory Factor Analysis to identify valid constructs and followed with Confirmatory Factor Analysis to test the hypothesized model. Data were collected through surveys and supported by qualitative insights from focus group discussions and key informant interviews. Initial model testing showed poor fit, prompting modifications. The revised model exhibited strong goodness-of-fit indicators (CMIN/DF = 1.85, RMSEA = 0.045, CFI = 0.97), validating the proposed relationships. Findings revealed that financial literacy has a significant positive direct effect on MSE viability (β = 1.369, p < 0.001) and also influences it indirectly through culture of resource utilization (indirect effect = 13.88). The total effect (15.249) indicates a partial mediation, highlighting the critical role of culture in enhancing the impact of financial knowledge. The study concludes that while financial literacy is vital, its full benefit is realized when coupled with efficient resource management culture. It recommends integrating financial literacy training with behavioral and cultural change programs targeting resource use norms in micro and small enterprises Owners.

VL - 11

IS - 1

ER -

Copy

|

Download