The author have developed a methodological approach to analyzing the effectiveness of tax regulation of enterprises, which contributes to improving the efficiency of governmental tax regulation in the conditions of digitalization. It has been proved that scientifically substantiated strategic planning of tax revenues contributes to the optimization of limited resources of the territory, which are directed to effective spatial development. It can be actively applied both at the national level and at the level of regions and municipalities. The flexibility of the methodology is justified, which allows taking into account multiple factors affecting the amount of corporate profit tax and the expediency of its application in assessing the effectiveness of governmental tax regulation in the conditions of digitalization of enterprises of most types of economic activity in the region subject to the correct selection of factor characteristics. The relevance of the scientific development of the problem considered by the author increases due to the fact that scientifically based plans are necessary to justify medium- and long-term measures, to develop the strategy of the enterprise as a whole. The practical importance of specific tasks of modeling taxation at the state level, taking into account the financial indicators of enterprises, is emphasized. Rational taxation has been proven to generate revenues to finance public services that improve the investment climate and meet other public goals.

| Published in | International Journal of Accounting, Finance and Risk Management (Volume 10, Issue 2) |

| DOI | 10.11648/j.ijafrm.20251002.11 |

| Page(s) | 86-93 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2025. Published by Science Publishing Group |

Digitalization, Strategic Analysis, Tax Regulation, Enterprise, Efficiency, Multivariate Correlation and Regression Analysis

Company | Taxes, mln. currency units | Costs, mln. currency units | Revenue from the sale of works (services), mln. currency units | The average annual cost of fixed assets, mln. currency units | Number of employees, people | Labor productivity per 1 employee, thousand currency units |

|---|---|---|---|---|---|---|

1 | 25.7 | 58.4 | 61.3 | 52.0 | 75 | 817.3 |

2 | 9.4 | 38.4 | 37.9 | 41.6 | 45 | 842.2 |

3 | 25.7 | 55.9 | 60.0 | 46.8 | 78 | 769.2 |

4 | 28.0 | 65.1 | 64.7 | 46.4 | 59 | 1096.6 |

5 | 25.9 | 58.9 | 60.6 | 47.3 | 79 | 767.1 |

6 | 27.8 | 61.7 | 63.6 | 53.6 | 77 | 826.0 |

7 | 27.2 | 58.8 | 60.6 | 45.9 | 84 | 721.4 |

8 | 23.1 | 49.5 | 52.9 | 46.5 | 67 | 789.6 |

9 | 27.4 | 60.9 | 62.7 | 52.4 | 81 | 774.1 |

10 | 27.7 | 61.6 | 63.4 | 53.0 | 82 | 773.2 |

11 | 27.5 | 59.4 | 61.2 | 46.4 | 85 | 720.0 |

12 | 28.0 | 62.2 | 64.1 | 53.5 | 83 | 772.3 |

13 | 27.7 | 61.5 | 63.4 | 52.9 | 82 | 773.2 |

14 | 22.9 | 46.0 | 50.1 | 53.0 | 66 | 759.1 |

15 | 27.5 | 61.0 | 62.9 | 53.1 | 76 | 827.6 |

16 | 24.9 | 53.6 | 55.8 | 44.9 | 75 | 744.0 |

17 | 28.5 | 63.0 | 65.1 | 49.1 | 86 | 757.0 |

18 | 27.5 | 61.5 | 63.3 | 52.4 | 80 | 791.3 |

19 | 25.1 | 53.7 | 56.4 | 45.4 | 76 | 742.1 |

20 | 25.1 | 55.8 | 56.4 | 45.4 | 76 | 742.1 |

21 | 25.1 | 55.9 | 60.0 | 50.9 | 74 | 810.8 |

22 | 28.5 | 60.2 | 64.2 | 49.1 | 85 | 755.3 |

Correlation matrix of features | ||||||

|---|---|---|---|---|---|---|

Factors | Y | X1 | X2 | X3 | X4 | X5 |

Y | 1.000000 | 0.904868 | 0.951575 | 0.533932 | 0.817665 | -0.06064 |

X1 | 1.000000 | 0.979134 | 0.499247 | 0.702351 | 0.164727 | |

X2 | 1.000000 | 0.560500 | 0.771929 | 0.072302 | ||

X3 | 1.000000 | 0.426937 | -0.02059 | |||

X4 | 1.000000 | -0.57391 | ||||

X5 | 1.000000 | |||||

Vector of average values of features | |||||

|---|---|---|---|---|---|

Y | X1 | X2 | X3 | X4 | X5 |

25.73636 | 57.40909 | 59.57273 | 49.16364 | 75.95454 | 789.6136 |

Parameters | Factors used in the analysis | ||

|---|---|---|---|

X1, X2, X4, X3, X5 | X2, X4, X3, X5 | X2, X3, X4 | |

Free member A0 | -8050.3500 | -9.73002 | -10.9604 |

Coefficients: A1 | -35.492800 | -0.3308500 | - |

A2 | -0.396530 | 0.873635 | 0.504554 |

A3 | 0.461381 | -0.038900 | 0.002838 |

A4 | 0.017201 | 0.056979 | 0.085572 |

A5 | 0.421822 | - | - |

Correlation coefficient (R) | 0.965647 | 0.964738 | 0.960525 |

Coefficient of determination (R2) | 0.932473 | 0.93072 | 0.922608 |

Durbin-Watson Coefficient (Kdw) | 1.586855 | 1.680009 | 1.908740 |

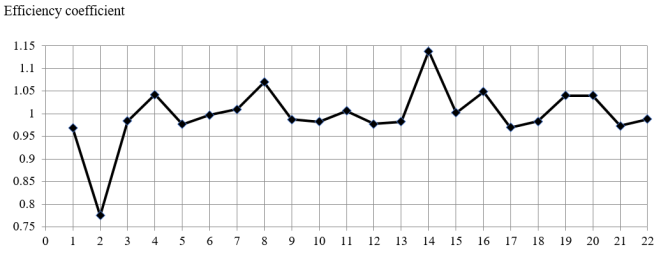

Company No. (condit.) | Profit tax, million currency units | Deviations (N i ACTUAL - N i EST.) | Efficiency coefficient of governmental tax regulation of business operation. K i EGTR | ||

|---|---|---|---|---|---|

Actual H i ACTUAL | Estimated N i EST | absolute, million currency units | relative, % | ||

1 | 25.7 | 26.75280 | -1.052800 | -3.935290 | 0.960647 |

2 | 9.4 | 11.62194 | -2.221940 | -19.118500 | 0.808815 |

3 | 25.7 | 26.81742 | -1.117410 | -4.166750 | 0.958332 |

4 | 28.0 | 26.81264 | 1.187365 | 4.428377 | 1.044284 |

5 | 25.9 | 26.38658 | -0.486580 | -1.844030 | 0.981560 |

6 | 27.8 | 27.72208 | 0.077923 | 0.281086 | 1.002811 |

7 | 27.2 | 26.75901 | 0.440987 | 1.647993 | 1.016480 |

8 | 23.1 | 22.11695 | 0.983046 | 4.444760 | 1.044448 |

9 | 27.4 | 27.47508 | -0.075080 | -0.273270 | 0.997267 |

10 | 27.7 | 27.88867 | -0.18867 | -0.676520 | 0.993235 |

11 | 27.5 | 27.12221 | 0.377787 | 1.392905 | 1.013929 |

12 | 28.0 | 28.33923 | -0.339230 | -1.197030 | 0.988030 |

13 | 27.7 | 27.92565 | -0.225650 | -0.808020 | 0.991920 |

14 | 22.9 | 20.51893 | 2.381073 | 11.604280 | 1.116043 |

15 | 27.5 | 27.30460 | 0.195398 | 0.715624 | 1.007156 |

16 | 24.9 | 23.81208 | 1.087923 | 4.568787 | 1.045688 |

17 | 28.5 | 29.29028 | -0.790280 | -2.698090 | 0.973019 |

18 | 27.5 | 27.74377 | -0.243770 | -0.878650 | 0.991214 |

19 | 25.1 | 24.34070 | 0.759296 | 3.119451 | 1.031195 |

20 | 25.1 | 23.64592 | 1.454081 | 6.149393 | 1.061494 |

21 | 25.1 | 26.43001 | -1.330010 | -5.032210 | 0.949678 |

22 | 28.5 | 29.37341 | -0.873410 | -2.973470 | 0.970265 |

NGO | Non-Governmental Organization |

IESF | International Educators and Scientists Foundation |

LaCI | Laboratory of Creative Ideas |

PO AAT ACD | Professional Organization of Auditors, Accountants Teachers of Accounting and Control Disciplines |

SPSS | Statistical Package for the Social Sciences |

| [1] | Verbivska, L.; Kriuchkova N.; Melnychenko R.; Bak N. 2023. Taxation strategy for small businesses in the context of digitalization. Financial and Credit Activity Problems of Theory and Practice, 4 (51): 66–79. [online cit.: 2025-02-10]. Available from: |

| [2] | Osaulenko, O.; Bondaruk, T.; Momotiuk, L. 2020. Ukraine’s State Regulation of the Economic Development of Territories in the Context of Budgetary Decentralisation. Statistics in Transition New Series, Vol. 21 Issue 3, New York: 129-148. [online cit.: 2025-02-10]. Available from: |

| [3] | Ievsieieva, O. 2018. Simulation of Taxation of Enterprises. International Journal of Engineering & Technology, 7 (4.3): 456–460. [online cit.: 2025-02-10]. Available from: |

| [4] | Kdyrova, I.; Sherman, M.; Ievsieieva, O., Pertsov, M.; Puhovskiy, E.; Yuryk, O. 2022. Digital Platforms in a Distance Learning Environment: An Educational Trend or the Need of the Hour? Journal of Curriculum and Teaching. Vol. 11, No. 8. Published by Sciedu Press: 273–280. [online cit.: 2025-02-10]. Available from: |

| [5] | Verbivska, L.; Zhuk, O.; Ievsieieva, O.; Kuchmiiova, T.; Saienko, V. 2023. The role of e-commerce in stimulating innovative business development in the conditions of integration. Financial and credit activity: problems of theory and practice, Volume 3 (50): 330–340. [online cit.: 2025-02-10]. Available from: |

| [6] | Gai, O.; Kononenko, L.; Chernovol, O. 2023. Tax audit in the conditions of digitalization: current state problems, perspectives. Economy & Society, No. 54: 1-8. [online cit.: 2025-02-10]. Available from: |

| [7] | Vinnytska O.; Chvertko L. 2024. Tax control as an element of interaction between tax payers and tax authorities. Economies’ Horizons: Scientific Jornal, No. 2-3 (28): 24-34. [online cit.: 2025-02-10]. Available from: |

| [8] | Voloshyna-Sidei, V.; Ievsieieva, O.; Maslyhan, O.; Syrtseva, S.; Nesterenko, O.; Harkusha, S. 2023. Strategic guidelines for the development of the economy in the conditions of global challenges and military aggression (Ukrainian case). Financial and credit activity: problems of theory and practice, Volume 1 (48): 219–228. [online cit.: 2025-02-10]. Available from: |

| [9] | SPSS Statistics: IBM [web-site / functional platform]: [online cit.: 2025-02-10]. Available from: |

| [10] | Opendatabot [electronic platform-service]: [online cit.: 2025-02-10]. Available from: |

| [11] | YouControl [web-platform]: [online cit.: 2025-02-10]. Available from: |

| [12] | Ievsieieva, O. 2019. Competitiveness Assessment for Transport Enterprises in the Context of Accelerated Development of the International Logistics Infrastructure. Fifteenth Scientific and Practical International Conference «International Transport Infrastructure, Industrial Centers and Corporate Logistics»: SHS Web of Conferences 67, 01004: 1–6. [online cit.: 2025-02-10]. Available from: |

| [13] | Ivanovska, A. 2023. Current issues of digitalizing the provision of administrative services in the field of taxation in Ukraine: regulatory and legal aspect. Economics. Finances. Law., No. 12: 15-19. [online cit.: 2025-02-10]. Available from: |

| [14] | Ievsieieva, O.; Dutchak, I.; Melyankova, L.; Smirnova, I.; Lepetan, I. 2024. Application of Innovative Technologies to Protect Financial Information in Accounting: Challenges of the Digital Economy Era // Pacific Business Review (International), Volume 17 issue 3: 62–79. [online cit.: 2025-02-10]. Available from: |

APA Style

O. I. (2025). State Tax Regulation of Enterprises in the Conditions of Digitalization. International Journal of Accounting, Finance and Risk Management, 10(2), 86-93. https://doi.org/10.11648/j.ijafrm.20251002.11

ACS Style

O. I. State Tax Regulation of Enterprises in the Conditions of Digitalization. Int. J. Account. Finance Risk Manag. 2025, 10(2), 86-93. doi: 10.11648/j.ijafrm.20251002.11

@article{10.11648/j.ijafrm.20251002.11,

author = {Olga Ievsieieva},

title = {State Tax Regulation of Enterprises in the Conditions of Digitalization},

journal = {International Journal of Accounting, Finance and Risk Management},

volume = {10},

number = {2},

pages = {86-93},

doi = {10.11648/j.ijafrm.20251002.11},

url = {https://doi.org/10.11648/j.ijafrm.20251002.11},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ijafrm.20251002.11},

abstract = {The author have developed a methodological approach to analyzing the effectiveness of tax regulation of enterprises, which contributes to improving the efficiency of governmental tax regulation in the conditions of digitalization. It has been proved that scientifically substantiated strategic planning of tax revenues contributes to the optimization of limited resources of the territory, which are directed to effective spatial development. It can be actively applied both at the national level and at the level of regions and municipalities. The flexibility of the methodology is justified, which allows taking into account multiple factors affecting the amount of corporate profit tax and the expediency of its application in assessing the effectiveness of governmental tax regulation in the conditions of digitalization of enterprises of most types of economic activity in the region subject to the correct selection of factor characteristics. The relevance of the scientific development of the problem considered by the author increases due to the fact that scientifically based plans are necessary to justify medium- and long-term measures, to develop the strategy of the enterprise as a whole. The practical importance of specific tasks of modeling taxation at the state level, taking into account the financial indicators of enterprises, is emphasized. Rational taxation has been proven to generate revenues to finance public services that improve the investment climate and meet other public goals.},

year = {2025}

}

TY - JOUR T1 - State Tax Regulation of Enterprises in the Conditions of Digitalization AU - Olga Ievsieieva Y1 - 2025/03/18 PY - 2025 N1 - https://doi.org/10.11648/j.ijafrm.20251002.11 DO - 10.11648/j.ijafrm.20251002.11 T2 - International Journal of Accounting, Finance and Risk Management JF - International Journal of Accounting, Finance and Risk Management JO - International Journal of Accounting, Finance and Risk Management SP - 86 EP - 93 PB - Science Publishing Group SN - 2578-9376 UR - https://doi.org/10.11648/j.ijafrm.20251002.11 AB - The author have developed a methodological approach to analyzing the effectiveness of tax regulation of enterprises, which contributes to improving the efficiency of governmental tax regulation in the conditions of digitalization. It has been proved that scientifically substantiated strategic planning of tax revenues contributes to the optimization of limited resources of the territory, which are directed to effective spatial development. It can be actively applied both at the national level and at the level of regions and municipalities. The flexibility of the methodology is justified, which allows taking into account multiple factors affecting the amount of corporate profit tax and the expediency of its application in assessing the effectiveness of governmental tax regulation in the conditions of digitalization of enterprises of most types of economic activity in the region subject to the correct selection of factor characteristics. The relevance of the scientific development of the problem considered by the author increases due to the fact that scientifically based plans are necessary to justify medium- and long-term measures, to develop the strategy of the enterprise as a whole. The practical importance of specific tasks of modeling taxation at the state level, taking into account the financial indicators of enterprises, is emphasized. Rational taxation has been proven to generate revenues to finance public services that improve the investment climate and meet other public goals. VL - 10 IS - 2 ER -

NGO International Educators and Scientists Foundation (IESF), Kyiv, Ukraine; NGO Laboratory of Creative Ideas (LaCI), Kharkiv, Ukraine; NGO Professional Organization of Auditors, Accountants Teachers of Accounting and Control Disciplines (PO AAT ACD), Kyiv, Ukraine

Information