Rice, corn, and soybeans are among the most widely cultivated crops, making them crucial for global food security and the economic well-being of many countries. Like many other crops, the global prices for these commodities are prone to fluctuations due to unfavorable weather conditions, natural disasters (like flooding), global demand, and economic crises. Consequently, their prices are subject to significant changes and volatility. Forecasting and modelling these prices offer valuable insights to policymakers and local growers within the agricultural sector. While there is a plethora of studies focusing on forecasting prices based on data obtained for a specific locality, country, or region, there is a paucity of publications that take on a more global outlook for rice, corn, and soybeans. The objective of this study is to use an Autoregressive Integrated Moving Average (ARIMA) process to model and forecast the international market prices of milled rice (5% broken), corn, and soybeans. We relied on World Bank data covering the period from 1988 to 2018 to construct several time series models. The average prices for milled rice, corn, and soybeans are $344.47, $144.48, and $334.72 (USD) per metric ton, respectively. The results of the model selection procedure indicate that the ARIMA (5,1,4), ARIMA (6,1,3), and ARIMA (6,1,1) models best fit the prices of milled rice, corn, and soybeans, respectively. Furthermore, these models offer the best in-sample and out-of-sample performances. The accuracy of the projected values, derived from the chosen models, was evaluated by calculating several metrics, including the mean absolute error (MAE), mean squared error (MSE), root mean square error (RMSE), and mean absolute percentage error (MAPE). This paper highlights the utility and applicability of the ARIMA model as a powerful tool for forecasting agricultural prices. Our modeling framework could enable governments and agribusinesses to (a) better anticipate global price fluctuations, (b) optimize trade decisions, (c) strengthen food security planning, and (d) engage in more sustainable agriculture.

| Published in | International Journal of Agricultural Economics (Volume 10, Issue 4) |

| DOI | 10.11648/j.ijae.20251004.13 |

| Page(s) | 170-182 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2025. Published by Science Publishing Group |

ARIMA Model, Price Volatility, Time Series Forecasting, Rice, Corn, Soybean, Economic Modeling, Agricultural Commodities

Descriptive | Rice | Corn | Soybeans |

|---|---|---|---|

Mean | 344.466 | 144.876 | 334.715 |

Median | 311.500 | 118.795 | 290.500 |

Std. Deviation | 126.858 | 59.588 | 117.607 |

Minimum | 163.750 | 75.270 | 183.000 |

Maximum | 907.000 | 333.053 | 684.020 |

Rice | Corn | Soybean | |||

|---|---|---|---|---|---|

Model | AIC | Model | AIC | Model | AIC |

ARIMA(6,1,3) | 3414.29 | ARIMA(4,1,4) | 2740.90 | ARIMA(6,1,6) | 3258.40 |

ARIMA(5,1,4) | 3414.76 | ARIMA(5,1,4) | 2741.06 | ARIMA(6,1,5) | 3259.26 |

ARIMA(3,1,2) | 3416.09 | ARIMA(6,1,5) | 2741.53 | ARIMA(3,1,3) | 3260.22 |

ARIMA(5,1,5) | 3416.12 | ARIMA(6,1,6) | 2741.92 | ARIMA(2,1,3) | 3268.49 |

ARIMA(2,1,4) | 3416.15 | ARIMA(3,1,5) | 2742.42 | ARIMA(1,1,1) | 3271.19 |

ARIMA(6,1,4) | 3416.37 | ARIMA(6,1,3) | 2751.96 | ARIMA(6,1,1) | 3271.93 |

Rice | Corn | Soybean | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

Model | MAPE | MAE | RMSE | Model | MAPE | MAE | RMSE | Model | MAPE | MAE | RMSE |

ARIMA(6,1,3) | 3.64 | 13.13 | 23.40 | ARIMA(4,1,4) | 4.00 | 6.09 | 9.46 | ARIMA(6,1,6) | 3.62 | 12.54 | 18.80 |

ARIMA(5,1,4) | 3.67 | 13.19 | 23.19 | ARIMA(5,1,4) | 3.88 | 5.94 | 9.37 | ARIMA(6,1,5) | 3.61 | 12.58 | 18.87 |

ARIMA(3,1,2) | 3.66 | 13.25 | 23.72 | ARIMA(6,1,5) | 3.84 | 5.88 | 9.32 | ARIMA(3,1,3) | 3.68 | 12.66 | 19.12 |

ARIMA(5,1,5) | 3.67 | 13.18 | 23.40 | ARIMA(6,1,6) | 3.85 | 5.89 | 9.29 | ARIMA(2,1,3) | 3.60 | 12.50 | 19.46 |

ARIMA(2,1,4) | 3.66 | 13.21 | 23.66 | ARIMA(3,1,5) | 3.88 | 5.99 | 9.46 | ARIMA(1,1,1) | 3.60 | 12.60 | 19.69 |

ARIMA(6,1,4) | 3.67 | 13.19 | 23.41 | ARIMA(6,1,3) | 3.95 | 6.01 | 9.54 | ARIMA(6,1,1) | 3.63 | 12.65 | 19.44 |

Rice | Corn | Soybean | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

Model | MAPE | MAE | RMSE | Model | MAPE | MAE | RMSE | Model | MAPE | MAE | RMSE |

ARIMA(6,1,3) | 3.099 | 13.100 | 15.596 | ARIMA(4,1,4) | 6.276 | 10.807 | 12.707 | ARIMA(6,1,6) | 6.163 | 22.307 | 25.421 |

ARIMA(5,1,4) | 1.958 | 8.284 | 10.303 | ARIMA(5,1,4) | 4.180 | 7.401 | 10.895 | ARIMA(6,1,5) | 6.145 | 22.239 | 25.389 |

ARIMA(3,1,2) | 2.204 | 9.357 | 11.889 | ARIMA(6,1,5) | 4.108 | 7.304 | 10.968 | ARIMA(3,1,3) | 5.138 | 18.435 | 23.659 |

ARIMA(5,1,5) | 2.020 | 8.518 | 10.299 | ARIMA(6,1,6) | 4.138 | 7.340 | 10.817 | ARIMA(2,1,3) | 4.020 | 14.402 | 18.834 |

ARIMA(2,1,4) | 2.273 | 9.649 | 12.289 | ARIMA(3,1,5) | 4.702 | 8.217 | 10.953 | ARIMA(1,1,1) | 3.782 | 13.501 | 18.190 |

ARIMA(4,1,2) | 2.256 | 9.580 | 12.225 | ARIMA(6,1,3) | 3.753 | 6.693 | 10.507 | ARIMA(6,1,1) | 3.643 | 13.019 | 17.586 |

Ljung-Box test | ||

|---|---|---|

Q* = 14.186, df = 14, p-value = 0.43591 | ARIMA(5,1,4) | lags=24 |

Q* = 39.369, df = 14, p-value =0.00031977 | ARIMA(6,1,3) | lags=24 |

Q* = 39.546, df = 16, p-value = 0.00090666 | ARIMA(6,1,1) | lags=24 |

ACF | Autocorrelation Function |

AIC | Akaike Information Criterion |

ARIMA | Autoregressive Integrated Moving Average |

ARIMAX | Autoregressive Integrated Moving Average with Exogenous Variables |

MAPE | Mean Absolute Percentage Error |

MAE | Mean Absolute Error |

PACF | Partial Autocorrelation Function |

RSME | Root Mean Squared Error |

SARIMAX | Seasonal Autoregressive Integrated Moving Average with Exogenous Variables |

WTO | World Trade Organization |

| [1] | Y. J. Mgale, Y. Yan, and S. Timothy, “A Comparative Study of ARIMA and Holt-Winters Exponential Smoothing Models for Rice Price Forecasting in Tanzania,” Open Access Libr. J., vol. 08, p. e7381, 2021, |

| [2] |

P. Sirisupluxana and I. Nitithanprapas Bunyasiri, “Risk assessment and risk management decisions: a case study of Thai rice farmers,” Bus. Manag. Rev., vol. 9, no. 3, pp. 200-207, 2018, [Online]. Available:

https://cberuk.com/cdn/conference_proceedings/2019-07-14-09-56-27-AM.pdf |

| [3] | R. Gök and E. Kara, “Impacts Of The Covid-19 Pandemic On The Agricultural Prices: New Insights From Cwt Granger Causality Test,” J. Res. Econ. Polit. Financ., vol. 5, pp. 76-96, 2020, |

| [4] | S. Frimpong, E. N. Gyamfi, Z. Ishaq, S. Kwaku Agyei, D. Agyapong, and A. M. Adam, “Can Global Economic Policy Uncertainty Drive the Interdependence of Agricultural Commodity Prices? Evidence from Partial Wavelet Coherence Analysis,” Complexity, vol. 2021, 2021, |

| [5] | G. Barrows, S. Sexton, and D. Zilberman, “The impact of agricultural biotechnology on supply and land-use,” Environ. Dev. Econ., vol. 755, pp. 676-703, 2014, |

| [6] | A. Adeosun, R. O. Olayeni, M. I. Tabash, and S. Anagreh, Revisiting the Oil and Food Prices Dynamics: A Time Varying Approach, vol. 19, no. 3. Springer International Publishing, 2023. |

| [7] | S. A. David, J. A. T. Machado, L. R. Trevisan, C. M. C. Inácio, and A. M. Lopes, “Dynamics of commodities prices: Integer and fractional models,” Fundam. Informaticae, vol. 151, no. 1-4, pp. 389-408, 2017, |

| [8] | Darekar and A. A. Reddy, “Forecasting of common paddy prices in India,” J. Rice Res., vol. 10, no. 1, pp. 71-75, 2017, Accessed: May 26, 2025. [Online]. Available: |

| [9] | P. V Cenas, “Forecast of Agricultural Crop Price using Time Series and Kalman Filter Method,” Asia Pacific J. Multidiscip. Res., vol. 5, no. 4, pp. 15-21, 2017. |

| [10] | Darekar and A. A. Reddy, “Forecasting wheat prices in India,” Wheat Barley Res., vol. 10, no. 1, pp. 33-39, 2018, [Online]. Available: |

| [11] | Bisht and A. Kumar, “Estimating Volatility in Prices of Pulses in India: An Application of Garch Model,” Econ. Aff. (New Delhi), vol. 64, no. 3, pp. 513-516, 2019, |

| [12] | R. W. Divisekara, G. J. M. S. R. Jayasinghe, and K. W. S. N. Kumari, “Forecasting the red lentils commodity market price using SARIMA models,” SN Bus. Econ., vol. 1, no. 1, pp. 1-13, 2021, |

| [13] | S. Luo, L. Y. Zhou, and Q. F. Wei, “Application of SARIMA model in cucumber price forecast,” Appl. Mech. Mater., vol. 373-375, pp. 1686-1690, 2013, |

| [14] | L. Mao, Y. Huang, X. Zhang, S. Li, and X. Huang, “ARIMA model forecasting analysis of the prices of multiple vegetables under the impact of the COVID-19,” PLoS One, vol. 17, no. 7, p. e0271594, 2022, |

| [15] | H. Adanacioglu and M. Yercan, “An analysis of tomato prices at wholesale level in Turkey: An application of SARIMA model,” Custos e Agronegocio, vol. 8, no. 4, pp. 52-75, 2012. |

| [16] | R. M. Mutwiri, “Forecasting of Tomatoes Wholesale Prices of Nairobi in Kenya: Time Series Analysis Using Sarima Model,” Int. J. Stat. Distrib. Appl., vol. 5, no. 3, pp. 46-53, 2019, |

| [17] | R. C. T. de Souza, O. Guedes Filho, M. A. R. dos Santos, and L. D. S. Coelho, “Monthly Closing Price Forecasting of Soybean Grain in Paraná Using Sarima Modeling With Intervention,” J. Geospatial Model., vol. 2, no. 1, pp. 27-44, 2016, |

| [18] | “Commodity Markets.” Accessed: Jun. 02, 2025. [Online]. Available: |

| [19] | P. C. Padhan, “Application of ARIMA Model for Forecasting Agricultural Productivity in India,” J. Agric. Soc. Sci., vol. 8, no. 2, pp. 50-56, 2012. |

| [20] | S. U. Pepple and E. E. Harrison, “Comparative Performance of Garch and Sarima Techniques in the Modeling of Nigerian Broad Money,” CARD Int. J. Soc. Sci. Confl. Manag., vol. 2, no. 4, pp. 2536-7242, 2017, [Online]. Available: |

| [21] | S. N. Kumari and A. Tan, “Modeling and forecasting volatility series: With reference to gold price,” Thail. Stat., vol. 16, no. 1, pp. 77-93, 2018. |

| [22] | Kathayat and A.. Dixit, “Paddy price forecasting in India using ARIMA mode,” J. Crop Weed, vol. 17, no. 1, pp. 48-55, 2021, |

APA Style

Bernard, B., Francois, L., Renville, D. S. (2025). Forecasting the International Market Prices for Rice, Corn and Soybeans Using ARIMA Time Series Modelling. International Journal of Agricultural Economics, 10(4), 170-182. https://doi.org/10.11648/j.ijae.20251004.13

ACS Style

Bernard, B.; Francois, L.; Renville, D. S. Forecasting the International Market Prices for Rice, Corn and Soybeans Using ARIMA Time Series Modelling. Int. J. Agric. Econ. 2025, 10(4), 170-182. doi: 10.11648/j.ijae.20251004.13

@article{10.11648/j.ijae.20251004.13,

author = {Bunnel Bernard and Linda Francois and Dwayne Shorlon Renville},

title = {Forecasting the International Market Prices for Rice, Corn and Soybeans Using ARIMA Time Series Modelling

},

journal = {International Journal of Agricultural Economics},

volume = {10},

number = {4},

pages = {170-182},

doi = {10.11648/j.ijae.20251004.13},

url = {https://doi.org/10.11648/j.ijae.20251004.13},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ijae.20251004.13},

abstract = {Rice, corn, and soybeans are among the most widely cultivated crops, making them crucial for global food security and the economic well-being of many countries. Like many other crops, the global prices for these commodities are prone to fluctuations due to unfavorable weather conditions, natural disasters (like flooding), global demand, and economic crises. Consequently, their prices are subject to significant changes and volatility. Forecasting and modelling these prices offer valuable insights to policymakers and local growers within the agricultural sector. While there is a plethora of studies focusing on forecasting prices based on data obtained for a specific locality, country, or region, there is a paucity of publications that take on a more global outlook for rice, corn, and soybeans. The objective of this study is to use an Autoregressive Integrated Moving Average (ARIMA) process to model and forecast the international market prices of milled rice (5% broken), corn, and soybeans. We relied on World Bank data covering the period from 1988 to 2018 to construct several time series models. The average prices for milled rice, corn, and soybeans are $344.47, $144.48, and $334.72 (USD) per metric ton, respectively. The results of the model selection procedure indicate that the ARIMA (5,1,4), ARIMA (6,1,3), and ARIMA (6,1,1) models best fit the prices of milled rice, corn, and soybeans, respectively. Furthermore, these models offer the best in-sample and out-of-sample performances. The accuracy of the projected values, derived from the chosen models, was evaluated by calculating several metrics, including the mean absolute error (MAE), mean squared error (MSE), root mean square error (RMSE), and mean absolute percentage error (MAPE). This paper highlights the utility and applicability of the ARIMA model as a powerful tool for forecasting agricultural prices. Our modeling framework could enable governments and agribusinesses to (a) better anticipate global price fluctuations, (b) optimize trade decisions, (c) strengthen food security planning, and (d) engage in more sustainable agriculture.},

year = {2025}

}

TY - JOUR T1 - Forecasting the International Market Prices for Rice, Corn and Soybeans Using ARIMA Time Series Modelling AU - Bunnel Bernard AU - Linda Francois AU - Dwayne Shorlon Renville Y1 - 2025/07/07 PY - 2025 N1 - https://doi.org/10.11648/j.ijae.20251004.13 DO - 10.11648/j.ijae.20251004.13 T2 - International Journal of Agricultural Economics JF - International Journal of Agricultural Economics JO - International Journal of Agricultural Economics SP - 170 EP - 182 PB - Science Publishing Group SN - 2575-3843 UR - https://doi.org/10.11648/j.ijae.20251004.13 AB - Rice, corn, and soybeans are among the most widely cultivated crops, making them crucial for global food security and the economic well-being of many countries. Like many other crops, the global prices for these commodities are prone to fluctuations due to unfavorable weather conditions, natural disasters (like flooding), global demand, and economic crises. Consequently, their prices are subject to significant changes and volatility. Forecasting and modelling these prices offer valuable insights to policymakers and local growers within the agricultural sector. While there is a plethora of studies focusing on forecasting prices based on data obtained for a specific locality, country, or region, there is a paucity of publications that take on a more global outlook for rice, corn, and soybeans. The objective of this study is to use an Autoregressive Integrated Moving Average (ARIMA) process to model and forecast the international market prices of milled rice (5% broken), corn, and soybeans. We relied on World Bank data covering the period from 1988 to 2018 to construct several time series models. The average prices for milled rice, corn, and soybeans are $344.47, $144.48, and $334.72 (USD) per metric ton, respectively. The results of the model selection procedure indicate that the ARIMA (5,1,4), ARIMA (6,1,3), and ARIMA (6,1,1) models best fit the prices of milled rice, corn, and soybeans, respectively. Furthermore, these models offer the best in-sample and out-of-sample performances. The accuracy of the projected values, derived from the chosen models, was evaluated by calculating several metrics, including the mean absolute error (MAE), mean squared error (MSE), root mean square error (RMSE), and mean absolute percentage error (MAPE). This paper highlights the utility and applicability of the ARIMA model as a powerful tool for forecasting agricultural prices. Our modeling framework could enable governments and agribusinesses to (a) better anticipate global price fluctuations, (b) optimize trade decisions, (c) strengthen food security planning, and (d) engage in more sustainable agriculture. VL - 10 IS - 4 ER -

Department of Mathematics, Physics and Statistics, University of Guyana, Georgetown, Guyana

Biography: Bunnel Bernard is a lecturer at the University of Guyana. He holds a BSc in Mathematics from the University of Guyana (2015) and an MSc in Applied Modelling and Quantitative Methods from Trent University (2024). His master’s research focused on developing a mathematical model and modelling structure for agricultural planning. Currently, his research interests lie in weather simulation and modelling, evapotranspiration estimation and modelling, multi-objective optimization, AquaCrop yield estimation, and the development of agricultural planning models. He is passionate about using applied mathematics and quantitative methods to address real-world challenges in agriculture and environmental systems. Through his work, he aims to contribute to more informed decision-making in climate-resilient agriculture and resource management by integrating modelling, data, and optimization strategies.

Research Fields: weather simulation and modelling, Reference Evapotranspiration estimation and modelling, Multi-objective optimization, AquaCrop yield estimation, and Agricultural planning models.

Department of Mathematics, Physics and Statistics, University of Guyana, Georgetown, Guyana

Biography: Linda Francois is a Lecturer at the University of Guyana, Department of Mathematics, Physics, and Statistics. She holds an MSc in Ac-tuarial Science with a minor in Finance from the University of Nebraska-Lincoln and a BSc in Statistics from the University of Guyana. Her work integrates statistical and mathematical analysis with applied research in public health, urban flood resilience, and time series modelling. She has contributed to studies on inclusive urban flood resilience and public health challenges in the Demerara-Mahaica region. Linda is committed to academic excellence, student development, and interdisciplinary collaboration supporting data-driven policy and sustainable development in Guyana.

Research Fields: Applied Statistical Modelling, Public Health Statistics, Urban resilience and Environmental Statistics, Development Studies, Biostatistics.

Department of Mathematics, Physics and Statistics, University of Guyana, Georgetown, Guyana

Biography: Dwayne Shorlon Renville is a lecturer in the Department of Mathematics, Physics, and Statistics at the University of Guyana. He obtained his Bachelor’s and Master’s degrees in Mathematics from the University of Guyana, Guyana, and the University of the West Indies, Mona Campus, Jamaica, respectively. He recently completed his doctoral degree in Innovation in Global Development at Arizona State University, USA, where his research focus has since been on inclusive development, urban flood resilience, and their fusion, inclusive urban flood resilience. As a freshly minted scholar of innovation in global development, Dr. Renville is spearheading a number of research papers in these fields. Relying on his mathematics background, Dr. Renville is engaged in other research projects and collaborations in other fields such as public health and biostatistics.

Research Fields: Development Studies, Inclusive Development, Flood Resilience, Biostatistics, Urban Studies.

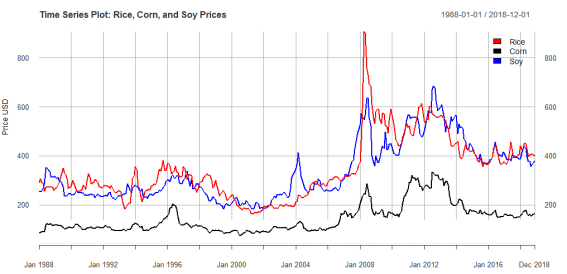

Figure 1. Time series plot of prices in USD for rice, corn, and soybeans (soy) from 1988-2018.

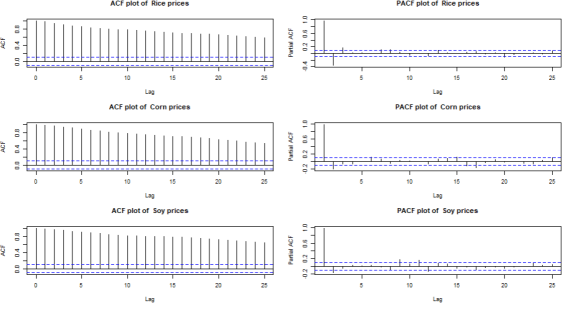

Figure 2. ACF and PACF plots of the prices of rice, corn, and soybeans (soy) from 1988-2018.

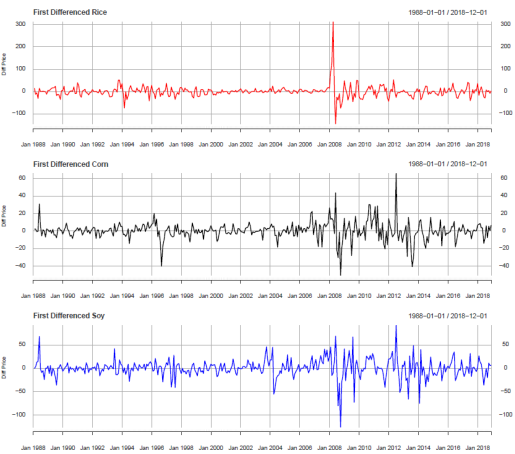

Figure 3. Time series plot of the first difference for rice, corn, and soybeans prices.

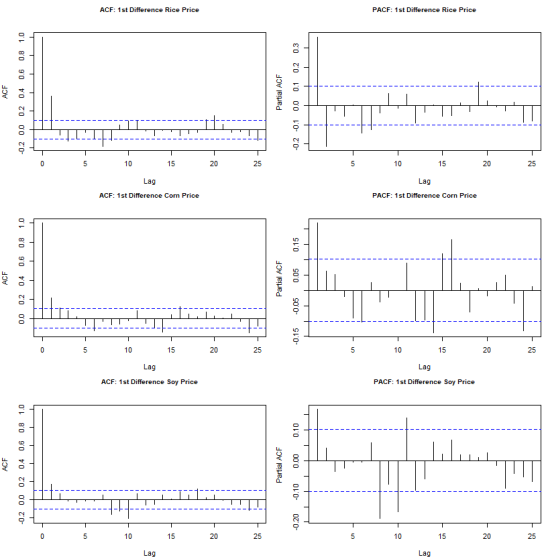

Figure 4. ACF and PACF plots of differenced prices of Rice, Corn, and Soybeans from 1988-2018.

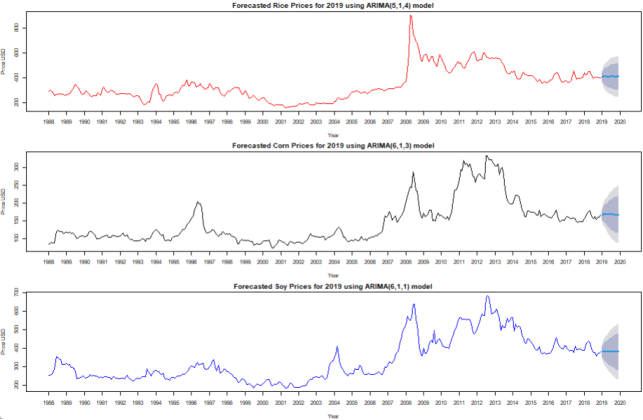

Figure 5. Forecast for year 2019 and original observations of rice prices using ARIMA(5,1,4), corn prices using ARIMA(6,1,3) and soybeans prices using ARIMA(6,1,1). Dark, grey-colored bands indicate 80% forecast confidence, while lighter grey-colored bands indicate 95% confidence.

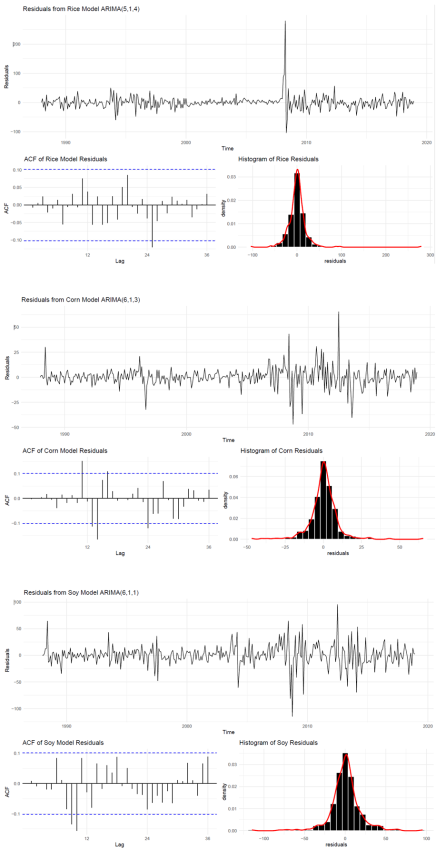

Figure 6. Residual plots of ARIMA(5,1,4), ARIMA(6,1,3) and ARIMA(6,1,1).

Information