2. Literature Review

2.1. Dimensions of Corporate Social Responsibility

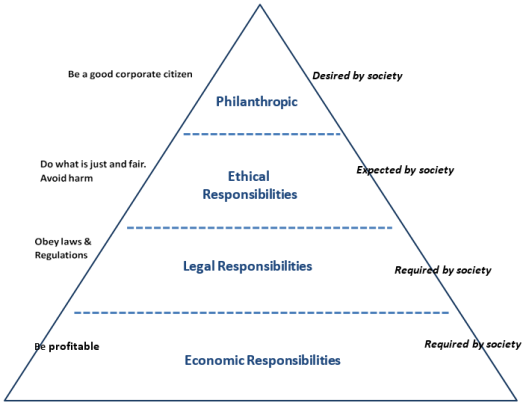

2.1.1. Economic Responsibility

Economic responsibility is the cornerstone of corporate social responsibility, emphasizing the need for businesses to be profitable while contributing positively to the economy. In the manufacturing sector, firms are expected to generate profits for their shareholders while also considering the broader economic impact of their operations. Companies that integrate social and environmental considerations into their economic strategies can achieve competitive advantages and foster innovation

| [14] | Khuong, M. N., An, N. K. T., Doanh, T. N., Tri, L. D. M., Phuong, N. N. D., Thanh, T. L. The Impact of Legal Environment on Business Success through the Practices of Corporate Social Responsibility. Management Science Letters. 2020, 10(13), 3033–3040. https://doi.org/10.5267/j.msl.2020.5.021 |

[14]

. This perspective is particularly relevant for manufacturing firms, which often face pressures to reduce costs while maintaining quality and sustainability. Furthermore, manufacturing companies that prioritize economic responsibility can enhance their long-term viability and stakeholder trust

| [11] | Islam, T., M., Jan, A. The Impact of Corporate Social Responsibility on Customer Loyalty: The Mediating Role of Corporate Reputation, Customer Satisfaction, and Trust. Sustainable Production and Consumption. 2021, 25, 123–135.

https://doi.org/10.1016/j.spc.2020.07.019 |

[11]

.

2.1.2. Legal Responsibility

Legal responsibility involves compliance with laws and regulations that govern business operations. In the manufacturing sector, this includes adherence to environmental regulations, labor laws, and safety standards. Legal responsibilities are mandatory and form the baseline for ethical business conduct

| [15] | M. N. Khuong, N. K. Truong an, and T. T. Thanh Hang, “Stakeholders and Corporate Social Responsibility (CSR) programme as key sustainable development strategies to promote corporate reputation—evidence from vietnam,” Cogent Bus. Manag., vol. 8, no. 1, 2021,

https://doi.org/10.1080/23311975.2021.1917333 |

[15]

. Proactive legal compliance can enhance a company's image and foster trust among stakeholders. Additionally, manufacturing firms that prioritize legal compliance not only avoid penalties but also gain a competitive edge by demonstrating their commitment to ethical practices.

2.1.3. Ethical Responsibility

Ethical responsibility extends beyond legal compliance, focusing on the moral obligations of businesses to act justly and fairly. In manufacturing, ethical considerations include fair labor practices, environmental stewardship, and transparency in operations. Ethical responsibilities are shaped by societal expectations and can significantly impact a company's reputation. Manufacturing firms are increasingly held accountable for their supply chain practices, as consumers demand ethical sourcing and production methods

| [16] | Kim, M. S., Thapa, B. Relationship of Ethical Leadership, Corporate Social Responsibility, and Organizational Performance. Sustainability. 2018, 10(2).

https://doi.org/10.3390/su10020447 |

[16]

.

2.1.4. Philanthropic Responsibility

Philanthropic responsibility refers to voluntary actions taken by companies to contribute to societal well-being. In the manufacturing sector, this can include community engagement, charitable donations, and support for local initiatives. Effective philanthropic strategies can enhance brand loyalty and customer engagement

| [17] | Lincoln, A. A. Challenges to Environmental Sustainability and Circular Economy Practices of Nigerian Small and Medium Enterprises. Journal of Sustainable Business. 2025,

https://doi.org/10.1186/s40991-025-00110-9 |

[17]

. Manufacturing firms that invest in community development not only fulfill their philanthropic duties but also create a positive corporate image that can lead to increased customer loyalty and employee satisfaction

| [18] | Machmuddah, Z., Sari, D. W., Utomo, S. D. Corporate Social Responsibility, Profitability, and Firm Value: Evidence from Indonesia. Journal of Asian Finance, Economics, and Business. 2020, 7(9), 631–638.

https://doi.org/10.13106/JAFEB.2020.VOL7.NO9.631 |

[18]

. Additionally, the role of corporate philanthropy in building sustainable communities and fostering long-term relationships with stakeholders.

Figure 1. Carroll’s Pyramid of CSR.

2.2. Current State of CSR Practices in Ethiopia

Corporate Social Responsibility practices in Ethiopia have been steadily gaining momentum in recent years, reflecting a growing recognition among businesses of the importance of integrating social and environmental considerations into their operations

| [19] | Matei, F. B., Boboc, C., Ghiță, S. The Relationship between Corporate Social Responsibility and Financial Performance in Romanian Companies. Economic Computation and Economic Cybernetics Studies and Research. 2021, 55(3), 297–314.

https://doi.org/10.24818/18423264/55.3.21.19 |

[19]

. The Ethiopian government has taken steps to promote responsible business conduct which aims to create an enabling environment for businesses to operate sustainably and contribute to social development. Despite these positive developments, challenges persist in effectively implementing and mainstreaming CSR initiatives in the Ethiopian business landscape

| [20] | Mihaljevic, M., Tokic, I. Ethics and Philanthropy in the Field of Corporate Social Responsibility Pyramid. Interdisciplinary Management Research. 2015, 11, 799–807. |

[20]

. One of the key challenges facing CSR implementation in Ethiopia is the limited awareness and understanding of CSR principles among businesses, particularly small and medium enterprises (SMEs). This lack of awareness is compounded by resource constraints, including financial limitations and a shortage of skilled personnel with expertise in CSR, which hinder the effective implementation of CSR programs. Additionally, the absence of clear regulatory frameworks and reporting mechanisms for CSR activities poses challenges in ensuring accountability and transparency in CSR practices, creating uncertainty around the expectations and standards for CSR implementation.

Nevertheless, Ethiopia presents significant opportunities for advancing CSR practices and driving sustainable business development. The country's rich cultural heritage and strong sense of community provide a solid foundation for fostering stakeholder engagement and social impact through CSR initiatives (Khuong et al., 2021). By leveraging these cultural values and community ties, businesses in Ethiopia can enhance their social license to operate and build trust with local communities. Furthermore, the emphasis on sustainable development and inclusive growth in Ethiopia's national development agenda creates a conducive environment for aligning CSR efforts with broader societal goals

| [21] | Muhammad, S. A. Influence of Corporate Social Responsibility Measure on Company's Financial Performance. Creative Business Research Journal. 2021, 1(2), 134-150. |

[21]

.

Collaborative partnerships between the government, private sector, and civil society can facilitate knowledge sharing, capacity building, and the co-creation of innovative CSR solutions to address pressing social and environmental challenges in the country. By building on existing cultural values, fostering stakeholder engagement, and aligning CSR initiatives with national development priorities, Ethiopian businesses can play a crucial role in driving sustainable development and creating shared value for society. Continued efforts from businesses, government, and civil society are essential to further mainstream CSR practices and unlock the full potential of responsible business conduct in Ethiopia.

2.3. The Role of Corporate Social Responsibility (CSR) on Business Performance

The role of corporate social responsibility in performance of manufacturing industries is an important consideration as businesses increasingly prioritize sustainable practices. By adopting CSR programs, companies can demonstrate their commitment to Sustainable environmental practice, worker safety, community engagement, and ethical behavior

. In turn, this improved public image and customer loyalty can translate into improved business performance.

The Triple Bottom Line theory, also known as 3P (Profit, People, Planet), expands the sole focus on financial profit to include the well-being of people and the long-term health of our planet. This framework calls for a balance between social, environmental, and financial performance, with each contributing to the overall success of the organization

| [23] | Sardana, D., Gupta, N., Kumar, V., Terziovski, M. CSR ‘Sustainability’ Practices and Firm Performance in an Emerging Economy. Journal of Cleaner Production. 2020, 258, 120766.

https://doi.org/10.1016/j.jclepro.2020.120766 |

[23]

. Implementing processes and practices in line with this philosophy can lead to cost savings, increased efficiency, reduced risk, and improved investor confidence in a manufacturing setting.

Stakeholder theory highlights the importance of considering the interests and well-being of all stakeholder groups, including employees, suppliers, customers, local communities, and investors. By addressing stakeholder concerns and integrating them into decision-making processes, organizations can make more informed choices, fostering support for their operations from stakeholders, which can lead to long-term success for both parties

| [24] | Shabbir, M. S., & Wisdom, O. The Relationship Between Corporate Social Responsibility, Environmental Investments, and Financial Performance: Evidence from Manufacturing Companies. Sustainability. 2020, 12(2), 123.

https://doi.org/10.3390/su12020467 |

[24]

. In the manufacturing sector, adopting and communicating CSR strategies and initiatives can help nurture positive relationships with these key stakeholders and create mutually beneficial partnerships for long-term success.

2.4. Corporate Social Responsibility and Profitability

The relationship between Corporate Social Responsibility (CSR) and profitability is a complex and widely debated topic in business literature. Research indicates that CSR can have both positive and negative impacts on a company's financial performance, with findings often varying based on context, industry, and the specific CSR initiatives undertaken.

Many studies support a positive correlation between CSR and profitability, suggesting that socially responsible practices can enhance a company's reputation, foster customer loyalty, and improve employee engagement. Companies that invest in CSR often experience better financial outcomes due to increased brand loyalty and customer satisfaction

| [25] | Singh, K., Misra, M. Linking Corporate Social Responsibility (CSR) and Organizational Performance: The Moderating Effect of Corporate Reputation. European Research on Management and Business Economics. 2021, 27(1), 100139.

https://doi.org/10.1016/j.iedeen.2020.100139 |

[25]

. The stakeholder theory further emphasizes that addressing the interests of various stakeholders can lead to long- term financial benefits.

Conversely, some studies highlight potential drawbacks, arguing that the costs associated with implementing CSR initiatives may outweigh the immediate financial benefits, particularly in the short term. CSR can enhance reputation, it may also impose significant costs that do not always translate into higher profits

| [1] | Almashhadani, M. Internal Control Mechanisms, Corporate Social Responsibility, and Profitability: A Discussion. International Journal of Business Management Invent. 2021, 10(12), 2319–801. https://doi.org/10.35629/8028-1012023842 |

[1]

.

The effectiveness of CSR in driving profitability is often influenced by factors such as industry context and the alignment of CSR strategies with core business objectives. Companies that integrate CSR into their business models and align it with their strategic goals are more likely to see positive financial returns. Additionally, industries with higher consumer engagement, such as consumer goods and services, may experience greater financial benefits from CSR initiatives compared to those in less engaged sectors.

2.5. Challenges to Environmental Sustainability and Circular Economy Practices of Paper Recycling Industries

There are various obstacles that the paper recycling industry must overcome in order to promote environmental sustainability and circular economy principles. The contamination of recyclable materials, which frequently arises from inappropriate disposal and a lack of public knowledge, is one significant problem

| [2] | Andrés, M., Agudelo, L., Jóhannsdóttir, L., & Davídsdóttir, B. A Literature Review of the History and Evolution of Corporate Social Responsibility. Journal of Cleaner Production. 2019, pp. 1–23. https://doi.org/10.1016/j.jclepro.2019.05.003 |

[2]

. Used Paper that is contaminated might result in lower- quality recycled products and higher processing expenses. Additionally, economic instability brought on by the varying demand for recycled paper can make it challenging for recycling operations to run effectively. Inefficiencies and increased waste levels result from the recycling process's added complexity caused by the absence of standardized collection and sorting mechanisms.

2.6. Theories of Corporate Social Responsibility

2.6.1. Carroll's Theory of Corporate Social Responsibility

Carroll's Pyramid of CSR, developed by Archie B. Carroll in 1991, presents a framework that categorizes the different responsibilities of businesses into economic responsibility, legal responsibility, ethical responsibility and Philanthropic Responsibilities. At the base of the pyramid, businesses are expected to be profitable and economically viable. This foundational responsibility emphasizes that companies must generate profit to survive and provide returns to shareholders. Above economic responsibilities, businesses must comply with laws and regulations. This includes adhering to labor laws, environmental regulations, and other legal requirements that govern business operations. Ethical responsibility level encompasses the expectations of society regarding ethical behavior. Companies are expected to operate fairly and justly, going beyond mere compliance with laws to consider the moral implications of their actions. At the top of the pyramid, philanthropic responsibilities involve voluntary actions that contribute to societal well-being, such as charitable donations, community engagement, and support for social causes. Carroll's Theory emphasizes that businesses should balance all four responsibilities to achieve a holistic approach to CSR. It suggests that while profit is essential, ethical and philanthropic actions can enhance a company's reputation and stakeholder relationships

| [5] | Aslaksen, H. M., Hildebrandt, C., Johnsen, H. C. G. The Long-Term Transformation of the Concept of CSR: Towards a More Comprehensive Emphasis on Sustainability. International Journal of Corporate Social Responsibility. 2021, 6(1).

https://doi.org/10.1186/s40991-021-00063-9 |

[5]

.

2.6.2. Triple Bottom Line Theory

The Triple Bottom Line Theory, developed by John Elkington in 1994, broadens the traditional definition of corporate success beyond financial performance to include social and environmental factors. TBL has three pillars: people (social), planet (environmental), and profit (economic). The People (Social) element focuses on the social impact of corporate activities, such as labor practices, community participation, and human rights. Companies are urged to think about the well-being of their employees and the communities in which they operate. The planet (environmental) dimension focuses on sustainability and the ecological impact of economic activity. Companies are encouraged to reduce their carbon footprint, waste, and use environmentally friendly techniques. Profit (Economic) demonstrates financial achievement, and while financial performance remains an important factor, TBL believes that economic success should not be at the expense of social and environmental obligations. The TBL framework encourages firms to use a broader approach to measuring success

| [12] | Gavrilova, T., Shakirova, B., Tsukrova, I., Sharifullina, R., & Lepik, K. Triple Bottom Line and Corporate Social Responsibility Performance Indicators for Russian Companies. Sustainability. 2020, 12(1), 313.

https://doi.org/10.3390/su120100313 |

[12]

. Companies that include social and environmental factors into their plans can improve long-term sustainability and provide value for all stakeholders.

2.6.3. Stakeholder Theory

Stakeholder Theory, particularly linked with R. Edward Freeman, asserts that corporations have a responsibility to a diverse range of stakeholders, not simply shareholders. Employees, consumers, suppliers, societies, and the environment are examples of stakeholders who have been affected by the company's actions

| [8] | Dmytriyev, S. D., Freeman, R. E., Hörisch, J. The Relationship between Stakeholder Theory and Corporate Social Responsibility: Differences, Similarities, and Implications for Social Issues in Management. 2021, pp. 1–30.

https://doi.org/10.1111/joms.12684 |

[8]

.

2.7. Corporate Social Responsibility Practices and Business Sustainability

The relation between Corporate Social Responsibility (CSR) practices and corporate sustainability is widely recognized as critical to long-term performance, particularly in emerging nations

| [25] | Singh, K., Misra, M. Linking Corporate Social Responsibility (CSR) and Organizational Performance: The Moderating Effect of Corporate Reputation. European Research on Management and Business Economics. 2021, 27(1), 100139.

https://doi.org/10.1016/j.iedeen.2020.100139 |

[25]

. CSR comprises the voluntary efforts made by corporations to address the social, environmental, and economic aspects of their operations, going beyond simple compliance with legal requirements to contribute constructively to society. Business sustainability, on the other hand, is functioning in a way that serves current needs without impacting future generations' ability to meet their own, while balancing economic viability, environmental stewardship, and social equality. According to research, there is a positive relationship between CSR activities, particularly environmental sustainability, and company performance, as organizations that actively engage in CSR are viewed as more credible and trustworthy, resulting in higher consumer loyalty and market share

| [24] | Shabbir, M. S., & Wisdom, O. The Relationship Between Corporate Social Responsibility, Environmental Investments, and Financial Performance: Evidence from Manufacturing Companies. Sustainability. 2020, 12(2), 123.

https://doi.org/10.3390/su12020467 |

[24]

. Furthermore, the effectiveness of these CSR initiatives can be significantly influenced by a company's internal capabilities, such as technological advancements and operational efficiencies; companies with strong plant capabilities are better positioned to implement sustainable practices effectively, thereby improving overall performance.

The motivations for CSR differ, with some organizations adopting these practices strategically to meet customer demand or comply with legislation, while others may engage in CSR willingly as part of their corporate ethos, which can influence how CSR is perceived and implemented. Furthermore, knowing the institutional context in which enterprises operate is critical, as CSR incentives in emerging economies such as India may differ from those in industrialized countries, influenced by local social norms, regulatory frameworks, and market dynamics. While CSR activities can lead to greater sustainability, issues such as resource allocation, market expectations, and varied levels of social awareness might hinder their implementation. Nonetheless, embracing CSR creates chances for innovation, stronger stakeholder relationships, and greater brand reputation, all of which contribute to long-term business sustainability.

2.8. Empirical Review and Research Hypothesis

2.8.1. The Effect of Economic Responsibility on Business Sustainability

Economic responsibility refers to an organization's ability to earn revenues, provide economic value, and ensure its financial survival. In contrast, organizational sustainability takes a broader approach, focusing on the organization's long-term prosperity while reducing negative consequences on the environment and society

| [26] | Suganthi, L. Investigating the Relationship Between Corporate Social Responsibility and Market, Cost, and Environmental Performance for Sustainable Business. South African Journal of Business Management. 2020, 51(1), 1–13.

https://doi.org/10.4102/sajbm.v51i1.1630 |

[26]

. Economic responsibility is critical for maintaining an organization's financial stability. This obligation provides the resources and capital required to support sustainability activities. The achievement of sustainability goals frequently requires optimizing resource utilization and lowering operational expenses. Organizations can benefit both economically and environmentally from embracing sustainable practices such as energy efficiency, waste reduction, and responsible sourcing

| [11] | Islam, T., M., Jan, A. The Impact of Corporate Social Responsibility on Customer Loyalty: The Mediating Role of Corporate Reputation, Customer Satisfaction, and Trust. Sustainable Production and Consumption. 2021, 25, 123–135.

https://doi.org/10.1016/j.spc.2020.07.019 |

[11]

. Resource-efficient operations not only reduce costs, but also improve overall economic performance.

Organizations that proactively manage and mitigate sustainability-related risks, such as those associated with climate change or supply chain disruptions, can avoid financial losses and reputational impact. The pursuit of sustainability objectives frequently spurs innovation and opens up new business opportunities. Organizations that implement sustainable practices can create innovative goods, services, and business models that react to the growing need for ecologically and socially responsible solutions, supporting economic growth and competitive advantage.

Hypothesis: A company's economic responsibility positively impacts its business sustainability.

2.8.2. The Effect of Legal Responsibility on Business Sustainability

Legal responsibility is critical, acting as a foundation for the long-term viability and good influence of companies. Legal responsibility includes an organization's obligation to follow the rules, regulations, and legal norms that govern its operations

| [27] | Waheed, A., Zhang, Q. Effect of CSR and Ethical Practices on Sustainable Competitive Performance: A Case of Emerging Markets from Stakeholder Theory Perspective. Journal of Business Ethics. 2020.

https://doi.org/10.1007/s10551-020-04679-y |

[27]

. Organizational sustainability, on the other hand, takes a comprehensive approach to achieving long-term success by combining social, economic, and environmental variables.

Adherence to legal standards is critical for minimizing the risks associated with legal violations, which can result in penalties, fines, and reputational damage. Organizations can lessen the likelihood of legal issues, as well as the financial and operational challenges that accompany them, by thoroughly comprehending and complying with relevant laws and regulations. This proactive strategy promotes long-term sustainability and stability

| [28] | Osadiya, T. T. Can the Differences in Senior Leadership Team & Society’s Orientations Impact on CSR Implementation in MNCs? A Case Study. Journal of Sustainable Business. 2025. https://doi.org/10.1186/s40991-025-00113-6 |

[28]

. Commitment to legal compliance is inextricably tied to an organization's reputation and stakeholder confidence. Organizations that stress legal responsibility are frequently perceived as trustworthy, accountable, and responsible, which boosts their reputation and promotes stakeholder relationships. This can lead to improved consumer loyalty, investor confidence, and employee happiness. Furthermore, legal obligation can act as a driver for sustainability developments across the sector. Organizations can set higher standards, influence industry practices, and promote genuine change by exceeding legal criteria rather than simply achieving them. As legal frameworks evolve to address rising sustainability concerns, organizations that lead in compliance can position themselves as innovators and leaders within their respective sectors

| [29] | Dunay, A., & Ayalew, A. Why Socially Responsible? Determinant Factors of Organizational Performance: Case of Dangote Cement Factory in Ethiopia. Cogent Business & Management. 2021, 8(1). https://doi.org/10.1080/23311975.2021.1899003 |

[29]

.

Hypothesis: A company's legal responsibility positively impacts its business sustainability.

2.8.3. The Effect of Ethical Responsibility on Business Sustainability

Ethical responsibility plays a crucial role in enhancing business sustainability by fostering stakeholder trust, improving financial performance, and driving innovation. Organizations that prioritize ethical practices tend to outperform their peers financially, as evidenced by research indicating that strong ethical conduct leads to enhanced brand reputation, customer loyalty, and the ability to attract and retain top talent

| [29] | Dunay, A., & Ayalew, A. Why Socially Responsible? Determinant Factors of Organizational Performance: Case of Dangote Cement Factory in Ethiopia. Cogent Business & Management. 2021, 8(1). https://doi.org/10.1080/23311975.2021.1899003 |

[29]

. Furthermore, ethical organizations create a positive workplace culture, resulting in higher employee engagement and satisfaction, which ultimately contributes to lower turnover rates and increased productivity. By proactively managing ethical risks, these organizations can mitigate potential legal disputes and reputational damage, ensuring stability and resilience essential for long-term sustainability.

Moreover, ethical responsibility drives innovation and adaptation to emerging challenges, positioning organizations to respond effectively to changing consumer preferences and societal expectations. As the global focus on ethical business practices intensifies, companies that embrace ethical responsibility are likely to thrive in an increasingly competitive and socially conscious marketplace, underscoring the importance of integrating ethical considerations into corporate strategies for long-term success

| [27] | Waheed, A., Zhang, Q. Effect of CSR and Ethical Practices on Sustainable Competitive Performance: A Case of Emerging Markets from Stakeholder Theory Perspective. Journal of Business Ethics. 2020.

https://doi.org/10.1007/s10551-020-04679-y |

[27]

.

Hypothesis: A company's ethical responsibility positively impacts its business sustainability.

2.8.4. The Effect of Philanthropic Responsibility and Business Sustainability

Philanthropic responsibility is closely interconnected with company sustainability, as both concepts are essential for fostering long-term profitability and positive societal impact. It entails an organization's commitment to give back to society through donations of resources, time, or expertise, which enhances stakeholder engagement and bolsters organizational reputation

| [20] | Mihaljevic, M., Tokic, I. Ethics and Philanthropy in the Field of Corporate Social Responsibility Pyramid. Interdisciplinary Management Research. 2015, 11, 799–807. |

[20]

. Businesses that focus on social well-being through philanthropy cultivate goodwill among stakeholders, which is crucial for sustained success. Philanthropic efforts address social challenges, including education, healthcare, poverty reduction, environmental conservation, and cultural preservation, thereby improving overall community well- being

| [30] | Becerra-Vicario, R., Ruiz-Palomo, D., León-Gómez, A., Santos-Jaén, J. M. The Relationship Between Innovation and the Performance of Small and Medium-Sized Businesses in the Industrial Sector: The Mediating Role of CSR. Economies. 2023, 11(3). https://doi.org/10.3390/economies11030092 |

[30]

. Furthermore, philanthropy facilitates networking and collaboration with other organizations, enabling shared resources and collective action in addressing sustainability issues. Initiatives that align with sustainability goals help differentiate businesses in the market and attract socially conscious consumers.

Hypothesis: A company's philanthropic responsibility positively impacts its business sustainability.

2.8.5. The Effect of Sustainable Environmental Practice on Business Sustainability

Sustainable environmental practices involve proactive measures taken by organizations to minimize their ecological footprint and implement strategies that protect the environment. This concept has gained traction as businesses acknowledge the importance of sustainability for regulatory compliance and enhancing long-term viability and competitive advantage. Organizations investing in sustainable practices frequently report reductions in operational costs and improved profitability over time, as these initiatives foster efficiencies that lead to financial gains

| [30] | Becerra-Vicario, R., Ruiz-Palomo, D., León-Gómez, A., Santos-Jaén, J. M. The Relationship Between Innovation and the Performance of Small and Medium-Sized Businesses in the Industrial Sector: The Mediating Role of CSR. Economies. 2023, 11(3). https://doi.org/10.3390/economies11030092 |

[30]

. Furthermore, organizations committed to sustainable environmental practices are better equipped to navigate complex regulatory landscapes and comply with increasingly strict environmental regulations

| [23] | Sardana, D., Gupta, N., Kumar, V., Terziovski, M. CSR ‘Sustainability’ Practices and Firm Performance in an Emerging Economy. Journal of Cleaner Production. 2020, 258, 120766.

https://doi.org/10.1016/j.jclepro.2020.120766 |

[23]

. By addressing regulatory challenges proactively, these companies can not only mitigate risks but also capitalize on differentiation opportunities within the marketplace. Ultimately, integrating sustainable environmental practices is a strategic necessity for businesses seeking long-term success, as the benefits extend beyond compliance to foster continuous improvement and adaptability in a rapidly changing business environment.

Hypothesis: A company's Sustainable environmental practice positively impacts its business sustainability.

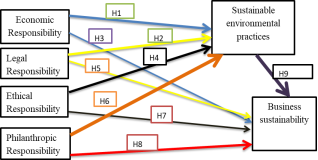

2.9. Conceptual Frame Work

This conceptual framework outlines the relationship between corporate social responsibility practices, sustainable environmental practices and business sustainability, with a focus on the Kuriftu paper mill

| [31] | Stojanovic, M., Milosevic, I., Arsic, S., Urosevic, S., Mihajlovic, I. Corporate Social Responsibility as a Determinant of Employee Loyalty and Business Performance. Journal of Competitiveness. 2020, 12(2), 149–166.

https://doi.org/10.7441/joc.2020.02.09 |

[31]

. The relationships between the key variables are presented in

Figure 2.

Figure 2. Conceptual Framework for the Study.

4. Results and Discussions

4.1. Reliability of the Research

Table 1 shows the Cronbach's Alpha reliability coefficients for major characteristics of corporate social responsibility (CSR) and business sustainability. Cronbach's Alpha is a useful tool for measuring measurement items' internal consistency

. Economic responsibility shows a Cronbach’s Alpha of 0.79, reflecting good reliability with its four items consistently measuring this aspect. Legal responsibility demonstrates even stronger reliability at 0.82, indicating that the four items effectively assess this construct. Ethical responsibility also maintains good reliability with a value of 0.79, suggesting that the ten items used are aligned in evaluating ethical practices within the organization. Philanthropic responsibility, while slightly lower at 0.70, still indicates acceptable reliability, though there may be opportunities for enhancement. In contrast, Sustainable environmental practice exhibits the highest reliability at 0.87, with its seven items providing a strong and consistent assessment. Finally, business sustainability achieves the highest Cronbach’s Alpha of 0.90, indicating that the eleven items used to measure this construct are very reliable.

Table 1. Reliability of the Research.

Variables | Cronbach’s Alpha | No. of items |

Economic Responsibility | 0.79 | 4 |

Legal Responsibility | 0.82 | 4 |

Ethical Responsibility | 0.79 | 10 |

Philanthropic Responsibility | 0.70 | 4 |

Sustainable environmental practice | 0.87 | 7 |

Business sustainability | 0.90 | 11 |

4.2. Correlation Analysis

The correlation illustrates the interrelationships among various dimensions of corporate social responsibility, sustainable environmental practices and business sustainability.

Table 2. Correlation Analysis.

Variable | EcoR | LR | EthR | PHR | SEP | BS |

EcoR | 1.00 | 0.76 | 0.73 | 0.71 | 0.74 | 0.82 |

LR | 0.76 | 1.00 | 0.75 | 0.58 | 0.71 | 0.81 |

EthR | 0.73 | 0.75 | 1.00 | 0.58 | 0.72 | 0.81 |

PHR | 0.71 | 0.58 | 0.58 | 1.00 | 0.61 | 0.58 |

SEP | 0.74 | 0.71 | 0.72 | 0.61 | 1.00 | 0.77 |

BS | 0.82 | 0.81 | 0.81 | 0.58 | 0.77 | 1.00 |

Where | EcoR=economic | responsibility | LR=Legal | responsibility | EthR=Ethical | responsibility |

PHR=Philanthropic responsibility, SEP=Sustainable environmental practice and BS=Business sustainability

Correlation coefficients, value closer to 1 indicate a strong positive relationship, while a value closer to -1 indicates a strong negative relationship. The correlation analysis presented in

Table 2 shows the relationships among CSR responsibilities and business sustainability. Economic responsibility, legal responsibility, ethical responsibility, philanthropic responsibility, and Sustainable environmental practice are all interconnected, with economic responsibility demonstrating a strong positive correlation with business sustainability.

Legal responsibility has a significant positive relationship with business sustainability, indicating that compliance with laws contributes to sustainable business practices

| [33] | Tiffany, T., Sufiyati, S. The Analysis of Factors Affecting Profitability. International Journal of Applied Economics and Business. 2023, 1(1), 603–612.

https://doi.org/10.24912/v1i1.603-612 |

[33]

. Ethical responsibility and philanthropic responsibility are also positively correlated with business sustainability, however to a lesser extent. Sustainable environmental practice also has a positive link with company sustainability, implying that focusing on environmental issues helps to promote sustainable business operations.

Among all the responsibilities analyzed, economic responsibility has the most positive link with business sustainability. This research give emphasis to the importance of economic responsibility in promoting sustainable company practices. As businesses increase their economic responsibility by making sure financial stability, profit growth, and responsible resource management, this contributes to their overall sustainability. If the correlation coefficient value between predictor variables is larger than 0.850, multicollinearity issue between such predictor variables is suspected

| [27] | Waheed, A., Zhang, Q. Effect of CSR and Ethical Practices on Sustainable Competitive Performance: A Case of Emerging Markets from Stakeholder Theory Perspective. Journal of Business Ethics. 2020.

https://doi.org/10.1007/s10551-020-04679-y |

[27]

. Therefore, correlation coefficient between independent variables is not suspected in this study.

4.3. Multi-collinearity Test Between Independent Variables

In regression analysis, Tolerance and Variance Inflation Factor (VIF) are used to assess multicollinearity among independent variables. Multicollinearity occurs when two or more independent variables are highly correlated, which can distort the model’s estimates. To find out if there is the exact issue of multi-collinearity, the value of Tolerance should be below 0.1 and Variance Inflation Factor (VIF) value should be larger than 10

. In our analysis, none of the independent variables exhibited a tolerance level below 0.10, and their corresponding VIF values were below 10. This indicates that there is no multicollinearity problems among the variables included in the model

.

Table 3. Tolerance and Variance Inflation Factor (VIF).

Independent Variables | Tolerance | VIF |

Philanthropic responsibility | .475 | 2.105 |

Legal responsibility | .327 | 3.057 |

Ethical responsibility | .342 | 2.926 |

Economic responsibility | .269 | 3.713 |

4.4. Model Summary for Predicting Business Sustainability

Table 4. Model Summary.

Model | R | R Square | Adjusted Square | R | Std. Error of the Estimate | Sig. F Change |

Without intermediate | 0.827 | 0.684 | .682 | | 3.409 | .000 |

With the Presence of intermediate | 0.861 | 0.741 | .739 | | 3.409 | .000 |

Source: SPSS version 27 computation, 2025

The model summary indicates a strong correlation between independent variables and business sustainability, showcasing effective regression analysis both without and with an intermediate variable. Without the intermediate variable, the model has an R value of 0.827 and an R² of 0.684, explaining 68.4% of the variance in business sustainability. The introduction of the intermediate variable enhances the model, raising the R value to 0.861 and the R² to 0.741, indicating that 74.1% of the variance is explained. The Adjusted R² slightly decreases to 0.739, showing minimal efficiency reduction due to new predictors. The standard error remains consistent at 3.409, and the F change significance remains at 0.000, confirming the model's statistical significance.

4.5. The Effects of Corporate Social Responsibility Practices on Business Sustainability

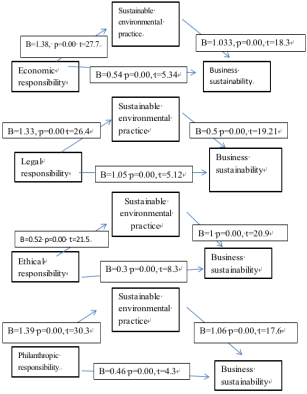

Figure 3. Relationships Between Corporate Social Responsibility Dimensions and Business Sustainability Mediated by Sustainable Environmental Practices.

This study explores the mediating role of sustainable environmental practices in the relationship between various forms of Corporate Social Responsibility (CSR) and business sustainability, particularly within kuriftu paper mill. The independent variables examined include economic, legal, ethical, and philanthropic responsibilities, with sustainable environmental practices serving as the mediator and business sustainability as the dependent variable. The analysis reveals significant findings: economic responsibility has a robust positive relationship with sustainable environmental practices, indicated by a coefficient of B = 1.38 (p < 0.00, t = 27.7), and it also demonstrates a substantial direct effect on business sustainability, with a coefficient of B = 1.033 (p < 0.00, t = 18.3). Similarly, legal responsibility significantly impacts sustainable environmental practices (B = 1.33, p < 0.00, t = 26.4) and exhibits a noteworthy direct effect on business sustainability (B = 1.05, p < 0.00, t = 5.12). Ethical responsibility contributes positively to sustainable environmental practices (B = 0.52, p < 0.00, t = 21.5) and significantly affects business sustainability (B = 1.06, p < 0.00, t = 17.6). Lastly, philanthropic responsibility shows a positive association with sustainable practices (B = 0.46, p < 0.00, t = 4.3) and has a notable impact on business sustainability (B = 0.23, p < 0.00, t = 20.9). The finding indicates the critical role of sustainable environmental practices as a mediator in the CSR-business sustainability relationship. This analysis highlights the importance of integrating sustainable practices into CSR strategies to enhance long-term business viability in the Ethiopian kuriftu paper millindustry, advocating for a strategic focus on sustainability to foster both environmental responsibility and robust business outcomes.

Table 5. The Effect of Sustainable Environmental Practice on Business Sustainability.

Variable | Effect of independent variables on business sustainability without mediator | Mediator variable | Effect of independent variables on business sustainability with mediator | BootSE | BootLLCI | BootULCI |

Effect of Economic responsibility on business sustainability | 0.541 | Sustainable environmental practices | 1.426 | .126 | 1.167 | 1.659 |

Effect of Legal responsibility on business sustainability | 0.5 | Sustainable environmental practices | 1.4 | .13 | 1.12 | 1.64 |

Effect of Ethical responsibility on business sustainability | 0.3 | Sustainable environmental practices | 0.51 | .06 | .39 | .63 |

Effect of Philanthropic responsibility on business sustainability | 0.46 | Sustainable environmental practices | 1.46 | .13 | 1.18 | 1.71 |

The assessment of how various dimensions of corporate responsibility influence business sustainability, both directly and indirectly, provides profound insights into the significance of sustainable environmental practice according to mentioned in

Table 5.

The direct effect of economic responsibility on business sustainability is quantified at 0.541, signifying a positive relationship independent of any mediating factors. This suggests that firms demonstrating strong economic responsibility significantly contribute to their sustainability outcomes

| [35] | Bux, H., Ahmad, N. Promoting Sustainability through Corporate Social Responsibility Implementation in the Manufacturing Industry: An Empirical Analysis of Barriers using the ISM-MICMAC Approach. 2020.

https://doi.org/10.1002/csr.1920 |

[35]

. However, when the influence of economic responsibility is assessed in conjunction with the sustainable environmental practices the effect notably amplifies to 1.426. This enhancement illustrates that adopting practices oriented towards sustainable environmental outcomes significantly boosts the impact of economic responsibility on overall business sustainability. The effectiveness of this mediating relationship is corroborated by the bootstrapped confidence intervals, which show BootLLCI at 1.167 and BootULCI at 1.659. Since both the lower and upper confidence intervals are positive, it confirms that significant mediation exists, thereby reinforcing the vital role of sustainable environmental practices as a mediator

.

Considering legal responsibility, its direct effect on business sustainability stands at 0.500. This relationship mirrors that of economic responsibility, indicating that adherence to legal standards positively influences sustainability outcomes. When factoring in the presence of sustainable environmental practices as a mediator, the indirect effect rises to 1.400, with BootLLCI documented at 1.120 and BootULCI at 1.640. The positive nature of both confidence intervals again reinforces the existence of significant mediation, emphasizing that sustainable environmental practices magnify the impact of legal responsibility on sustainability achievements.

The influences of ethical and philanthropic responsibilities, though comparatively lower than those of economic and legal responsibilities, remain relevant. The direct effect of ethical responsibility is documented at 0.300, leading to an indirect effect of 0.510 when sustainable environmental practices are considered as mediators. This is supported by BootLLCI at 0.390 and BootULCI at 0.630, which again indicates significant mediation as both confidence intervals are positive. Furthermore, philanthropic responsibility carries a direct effect of 0.460 coupled with a substantial indirect effect of 1.460, further validated by confidence intervals showing BootLLCI at 1.180 and BootULCI at 1.710. The positivity of these intervals further solidifies the evidence of significant mediation in this context.

4.6. Hypothesis Testing Results

The analysis of corporate social responsibility (CSR) practices reveals a series of significant and positive relationships with business sustainability, emphasizing the integral role of sustainable environmental practices as a mediating factor. Specifically, it was found that a company's economic responsibility, legal responsibility, ethical responsibility, and philanthropic responsibility all have statistically significant impacts on business sustainability, with p-values less than 0.05, indicating their critical role in enhancing sustainable practices. This suggests that organizations prioritizing these CSR dimensions are likely to achieve better sustainability outcomes

| [31] | Stojanovic, M., Milosevic, I., Arsic, S., Urosevic, S., Mihajlovic, I. Corporate Social Responsibility as a Determinant of Employee Loyalty and Business Performance. Journal of Competitiveness. 2020, 12(2), 149–166.

https://doi.org/10.7441/joc.2020.02.09 |

[31]

.

Furthermore, the findings illuminate the important mediating role of sustainable environmental practices in these relationships

| [14] | Khuong, M. N., An, N. K. T., Doanh, T. N., Tri, L. D. M., Phuong, N. N. D., Thanh, T. L. The Impact of Legal Environment on Business Success through the Practices of Corporate Social Responsibility. Management Science Letters. 2020, 10(13), 3033–3040. https://doi.org/10.5267/j.msl.2020.5.021 |

[14]

. Economic responsibility, legal responsibility, ethical responsibility, and philanthropic responsibility each significantly bolster sustainable environmental practices, thereby enhancing their positive effects on overall business sustainability. The p-values for these mediation effects are also below 0.05, affirming their statistical significance.

In addition, the direct relationship between sustainable environmental practices and business sustainability was confirmed to be substantial, with a p-value of 0.000, further underscoring the necessity of integrating sustainable environmental initiatives into business strategies.

Table 6. Hypothesis Table.

Hypothesis | Relationship | B | P Value | Result |

H1 | Economic responsibility positively influences sustainable environmental practices within businesses. | 1.38 | 0.000 | Supported |

H2 | Legal responsibility positively influences sustainable environmental practices within businesses. | 1.33 | 0.000 | Supported |

H3 | Ethical responsibility positively influences sustainable environmental practices within businesses. | 1.05 | 0.000 | Supported |

H4 | Philanthropic responsibility positively influences sustainable environmental practices within businesses. | 1.06 | 0.000 | Supported |

H5 | Sustainable environmental practices significantly mediate the relationship between economic responsibility and overall business sustainability. | 0.54 | 0.000 | Supported |

H6 | Sustainable environmental practices significantly mediate the relationship between legal responsibility and overall business sustainability. | 0.30 | 0.000 | Supported |

H7 | Sustainable environmental practices significantly mediate the relationship between ethical responsibility and overall business sustainability. | 0.23 | 0.000 | Supported |

H8 | Sustainable environmental practices significantly mediate the relationship between philanthropic responsibility and overall business sustainability. | 0.46 | 0.000 | Supported |

H9 | A direct positive relationship exists between sustainable environmental practices and overall business sustainability. | 1.06 | 0.000 | Supported |

Supported Hypotheses: All hypotheses are supported.